Written Commentary

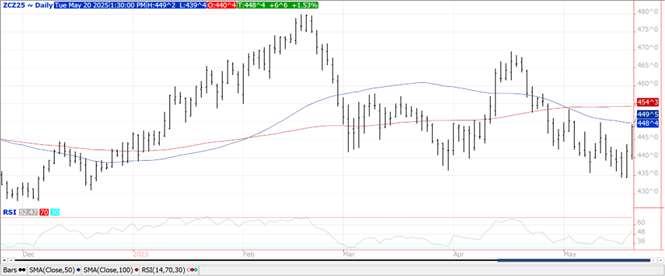

Prices were up $.06-$.07 higher closing near session highs. Spreads were little changed. Both July-25 and Dec-25 traded to a 1 week high. Near term resistance for Dec-25 is at the 50 day MA at $4.49 ½. Healthy rains moved across the central Midwest the past 24 hours with many areas picking up over an inch of moisture. Much of the nation’s midsection will remain in an active weather pattern over the next week. Rain is expected to favor the S. Midwest and northern Delta region where isolated flooding may occur. Plantings advanced 16% to 78% complete, above the 67% pace from YA while also staying ahead of the 5-year Ave. of 73%. Plantings were in line with expectations. Minor delays are noted in IL and TN with more significant delays in KY with 63% planted vs. 74% Ave. and OH 34% vs. 48%. Brazil is investigating 6 potential outbreaks of the highly pathogenic bird flu, with 2 of the suspected cases on commercial farms. EU corn imports as of May 18th at 17.7 mmt are up 8% from YA. Tomorrow’s EIA report is expected to show ethanol production ranged from 289-307 mil. gallons LW vs. 292 mil. the previous week. The continued expansion of corn based ethanol in Brazil has drawn down their corn stocks while limiting their supply for export. This should continue to benefit the US exports well into the 25/26 MY.

Prices were modestly higher across the complex with beans up $.02-$.04, meal was up $1-$2 while oil was slightly higher. Spreads were mixed and little changed. July-25 beans continue to consolidate near its 100 day MA at $10.47 ¾. Inside trade for July-25 oil as prices consolidate between $.48-$.50 lbs. July-25 meal once again established a fresh 6 week low while holding support above its contract low at $289.70. Spot board crush margins rebounded another $.02 to $1.35 ½ bu. with bean oil PV slipping to 45.8%. Although Argentine flooding hasn’t impacted major producing areas, the BAGE warns they may need to lower their production forecasts due to the heavy rains in northern Buenos Aires. Plantings advanced 18% to 66% complete, above the 50% pace from YA and 5-year Ave. of 53%. Emergence has reached 34% vs. the 5-year Ave. of 23%. The only states running behind their historical average are MS at 76% vs. 78% and KY 43% vs. 46%. Of the 6.1 mmt of soybeans imported by China in April-25, 4.6 mmt were from Brazil with 1.38 mmt from the US. Their imports from Brazil are down 22% YOY, while the imports from US were off 44%. EU soybean imports as of May 18th at 12.5 mmt are up 6.8% YOY. Their meal imports at 16.8 mmt are up 24.4%. Japan’s chief trade negotiator is expected to visit the US for a 3rd meeting with the Trump Administration this Friday. India is reportedly seeking a multi-phase trade agreement with the US, aiming to finalized before the reciprocal tariffs take effect in July.

Prices were higher across all 3 classes today ranging from $.12 higher in MGEX to $.17 better in CGO. July-25 CGO stalled out just shy of the May high at $5.48. Near-term resistance for July-25 KC is at $5.46 ¾. Wheat was the upside leader as lower winter crop ratings combined with another round of heavy rain across the S. Midwest provided the fuel for today’s rally. Cool temperatures with potential for damaging frost in key growing areas of E. Europe also lent support. WW conditions slipped 2% to 52% G/E as there was a 2% shift from good to fair. Expectations were for ratings to hold steady. Overall composite ratings remain their highest since 2020. 64% of the crop is headed vs. 67% from YA and the 5-year Ave. of 58%. Current ratings suggest an average yield of 52.6 bpa and production of 1.353 bil. using the USDA’s harvested acres forecast, below the USDA est. of 1.382 bil. Spring wheat plantings advanced 16% to 82% complete vs. 76% from YA and well above the 5-year Ave. of 65%. EU soft wheat exports as of May 18th have reached 18.5 mmt, down 33.7% YOY.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.