Written Commentary

While the summer holiday season has gotten underway, the new week brings a deluge of major data from the USA, China and UK, though precious little elsewhere, while the usual roster of banking and financial behemoths gets the US Q2 earnings season underway. The events schedule has Fed’s Warsh making his first semi-annual testimony (formerly known as Humphrey Hawkins) to Congress, an expected rate hold from Canada’s BoC, and, by contrast, an initial rate hike from the Bank of Korea.

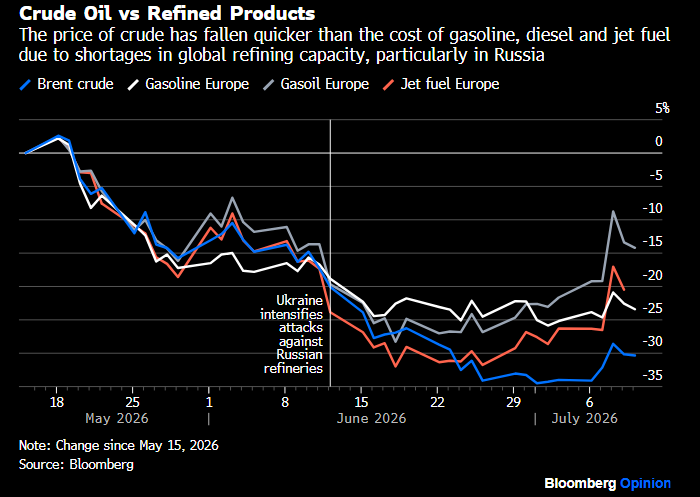

Tensions in the Persian Gulf continue to run high, though, for the time being, a full-blown resumption of hostilities does appear to be high on the list for either side, though the risk cannot be ignored. Perhaps more material is that increased attacks imply the modest recovery in traffic through the Strait of Hormuz remains ‘Stop/Go’, with crude inventories continue to decline, with stocks of key refined products even more precarious, while Europe’s summer restocking of gas storage is way behind its typical seasonal cycle. The threat of increasing disruptions to energy and agricultural output from Russia and Ukraine cannot be overlooked, with both sides seemingly focused on inflicting damage on key infrastructure – be that power, refineries, storage or ports. There remains a glaring disconnect between the relative calm of energy futures and physical pricing, be that for crude or products, and paper markets seem to be focused much more on the prospects of a glut of supply on the hopeful, rather than well-reasoned assumption that energy supplies will gradually return to normal. That narrative appears to dismiss the challenge of rebuilding depleted inventories across the globe and the unsurprising drive in many countries to increase storage capacity, which will also need to be filled.

A third major heatwave in Western Europe, the devastating impact of Typhoon Bavi in China and Taiwan, while many in Asia Pacific’s agricultural areas, and western forecasters fret about a Super El Nino lasting into early 2027, with climate historians noting that an El Nino was a major contributor to the great famine of the 1870s, which claimed the lives of 50 million people, when the global population was about 1.3 Bln people, as against the current 8.3 Bln. Many may decry this as peddling gloom and doom when the global economy is displaying considerable resilience in the face of a run of crises, but the point is simple: the array of risks is large and as much as technological advances have and are mitigating the multi-faceted threats that the world faces, a tipping point may be reached.

USA: CPI tops a busy run of statistics, with a sharp drop in gasoline prices expected to edge headline lower by -0.1% m/m, and the y/y rate down to a still lofty 3.8% from 4.2%, though core is seen up a very average 0.2% m/m to keep the y/y rate unchanged at 2.9%, due to upward pressure from hotels, leisure and airfares due to the World Cup, and consumer electronics from very lofty memory chip prices. PPI is forecast to slow sharply in m/m terms to unchanged headline in the main due to energy prices (gasoline and jet fuel most notably), and 0.3% core, which would see headline y/y ease to 6.2%, but core climb to 5.2%. While signalling an all clear on inflation, as or lower than expected outcomes would probably prompt a further reduction in the probability of an end July Fed rate hike.

Retail Sales are seen slowing to 0.3% m/m, paced above all by a price related fall in gasoline sales (ex-Autos median -0.1% m/m), but the core ‘Control Group’ measure is expected to ease only marginally to 0.5% m/m vs. May 0.7% – as ever, beware of the often quite sharp revisions. Industrial Production is forecast to edge up to 0.2% m/m with Manufacturing Output eking out a 0.1% m/m gain, while both the NY and Philly Fed Manufacturing surveys are anticipated to signal the manufacturing sector is in good health, and NFIB Small Business Optimism to edge up, but remain quite subdued. The Fed’s Beige Book will likely continue to describe growth as ‘slight to moderate’, with some relief from the short-lived MoU between the US and Iran likely to have boosted outlook optimism (and the report unlikely to capture reaction to the renewed set of tensions). As for Warsh’s testimony, this may prove to be a ‘nothing burger’, both due to his rejection of forward guidance on the policy outlook, the fact that he did not even sign the written monetary policy report, and his previously well documented aversion to answering any politically motivated questions.

China: Tuesday brings the latest set of Trade data, with Exports expected to post a marginally lower though still very robust pace of growth at 18.2%, though anecdotal port data implies some upside risks, while Imports are also seen easing relative to May, but remaining very high at 24.7%, and primarily paced by falling commodity prices, overall confirming that external demand remains very robust. But that is not likely to be enough to avoid a significant setback in Q2 GDP to 4.5% y/y from Q1’s 5.0%, or 0.9% q/q from 1.3%, with accompanying monthly forecast to show Retail Sales remaining slightly in negative territory at -0.1%, Fixed Asset Investment woeful at -5.0% y/y, underlining the weakness in domestic demand, with Industrial Production holding up at 4.5% y/y. But well off the pace of the early part of 2026.

U.K.: Monthly GDP is seen returning to meagre growth at 0.1% m/m, after dropping -0.1% m/m in April, with Retail Sales strength a key contributor, even if the Index of Services is also seen at 0.1% m/m, but Manufacturing Output is expected drop -0.2% after an auto sector boost of 0.4% in April, while Construction Output is forecast to dip -0.3%. BRC Retail Sales are published ahead of that on Tuesday. With the BoE seemingly on hold for at least the next meeting, the coronation of Andy Burnham as Labour Party leader on Saturday, and installation as PM on Monday, and England still contending for the World Cup, this week’s run of data may prove to be little more than statistical roadkill, even if it underlines the challenges that the new PM will face.

US S&P 500 Q2 earnings are expected to show earnings growth at a whopping 23.6% (vs. 18.8% at the start of Q2), even if one would have to stress that Mag7 tech companies’ manipulation of depreciation timelines as distorting the picture (above all given the outsized ‘hyperscaling’ of AI related investments), while revenue growth is seen up a robust 11.7%. There are 13 S&P 500 companies reporting this week, with worldwide corporate earnings highlights as compiled by Bloomberg News likely to include: ABB, Abbott Laboratories, ASML, Assa Abloy, Atlas Copco, Avenue Supermarts, Bank of America, Bank of New York Mellon, BayCurrent, Blackrock, Cintas, Citigroup, Citizens Financial, Cosmos Pharmaceutical, Danske Bank, DNB Bank, Epiroc, EQT, Fastenal, Fifth Third, General Electric, Goldman Sachs, HCL Technologies, Intuitive Surgical, Investor, JB Hunt Transport Services, Johnson & Johnson, JPMorgan Chase, JSW Steel, Kongsberg Gruppen, LM Ericsson, Lufax, M&T Bank, Money Forward, Morgan Stanley, Netflix, Nordea Bank, Peric Special Gases, PNC Financial Services, Progressive, Prologis, Publicis, Regions Financial, Saab, Sandvik, Sansan, Shift, Skandinaviska Enskilda Banken, State Street, Svenska Handelsbanken, Swedbank, TSMC aka Taiwan Semiconductor Manufacturing, Travelers, Truist Financial, United Airlines, UnitedHealth, US Bancorp, Volvo, Wells Fargo.