Written Commentary

A cessation of military strikes between Israel and Iran allows markets once more to live in hope of a more durable ceasefire, though bridging the gaps between the various sides still looks to be a major challenge, with ceasefire violations likely to continue. A much busier day in terms of statistics has China Trade, German Trade and Industrial Production, South Korea’s upwardly revised Q1 GDP and UK BRC Retail Sales and Barclaycard Consumer Spending to digest along with a surprise off-cycle rate hike in Indonesia, desperately trying to shore up its beleaguered currency. Ahead lie South Africa’s Q1 GDP, US NFIB Small Business Optimism, Existing Home Sales and Trade Balance and Mexican CPI, and a speech by new Bank of France governor Moulin, though the ECB is in purdah ahead of Thursday’s policy meeting, so he is unlikely to touch on the policy outlook.

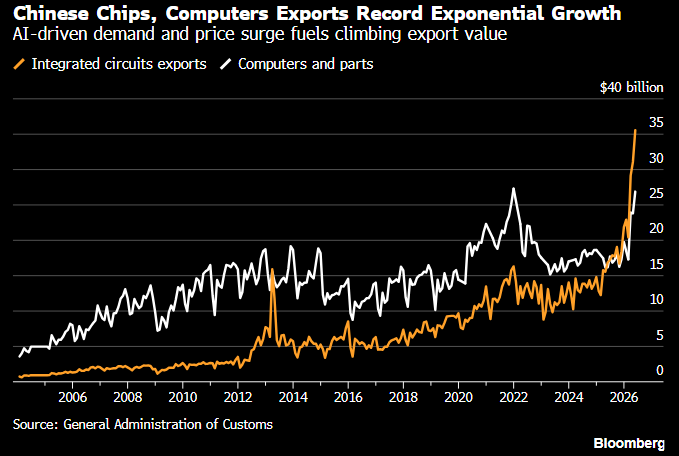

** China – May Trade Balance **

– Another set of stronger than expected trade data attests to the continued strength of export demand, above all for semiconductors and a broad array of tech equipment, as the attached chart attests, along with autos, again underlining the lopsided profile of growth across much of the world, while refined oil products continued to decline. On the import side the slide in crude oil imports continues (-29% to 7.9 Mln bpd, some 2.0 Mln plus below pre-Iran conflict, wholly unsurprising given high prices and China’s long-established pattern of purchases of raw materials of any description. For a discussion on China’s crude inventories management, please watch today’s Gulf Intelligence ‘Daily Energy Podcast’ on YouTube: But otherwise, the trade data again underlines the weakness in domestic demand.

** U.S.A. – May NFIB Small Business Optimism **

– NFIB Small Business Optimism is expected to be little changed at a modest 96.0. But with the already published Employment components showing Hiring Plans sliding to their lowest level (+9) since the pandemic, the risks look to be to the downside, unless the recent slide in the Economic Outlook (last 4 vs. prior 11) is halted, which seems unlikely given persistently high energy prices and uncertainty related to the Persian Gulf conflict. A close eye also needs to be kept on Selling Prices (last 30 vs. 25) and Sales (last 3 vs. 7). As an aside yesterday’s headline NY Fed 1-yr Inflation expectations may have eased to 3.46% y/y from 3.64%, but the details highlighted that over the next year consumers see gasoline prices up 5%; food prices up 5.8%; medical costs up 8.9%; college education to rise 8% and rent prices to rise 7.4% – that expected pressure on non-discretionary prices will continue to keep White House approval ratings depressed.