Written Commentary

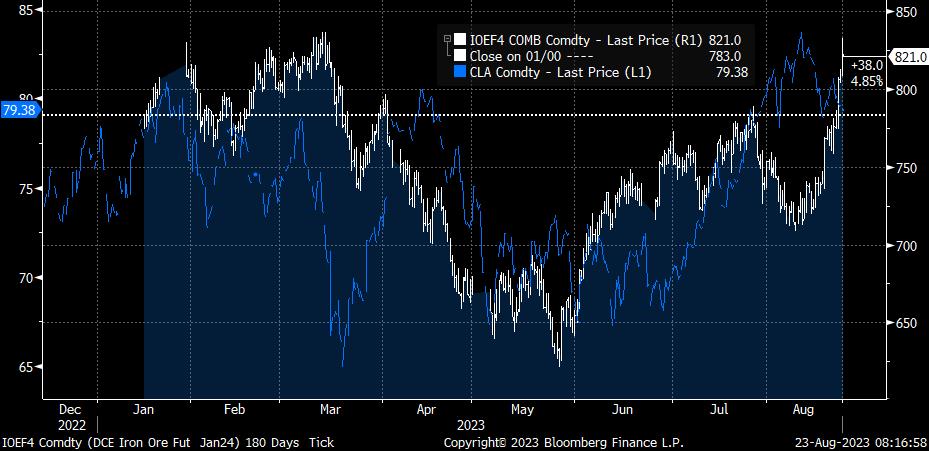

G7 flash PMIs dominate the data calendar, with South African CPI, Canadian Retail Sales and US New Home Sales, but otherwise the schedule is again rather thin, with weekly EIA oil inventories, and corporate earnings from AI investors’ ‘hot stock’ Nvidia the other highlights. Govt bond supply takes form of German 7-yr, US 20-yr and FRN 2-yr. China’s economic and property woes and concerns about higher for longer rates and the implications for the world’s mountain of debt remain the overarching themes, but there are anomalies appearing in this. Take, for example, the very surprising recent rise in Iron Ore futures, supposedly on China optimism, and contrast that with oil’s retreat from its recent highs on concern about China demand – see chart.

It’s also worth giving some thought as to whether the recent rise in US yields and accompanying steepening of the UST curve has prompted banks (perhaps at the behest of the Fed and other regulators) to address the issue of unrealized losses on bond holdings (with credit ratings downgrades adding to the pressure), and forcing some liquidation, with the mountain of recent T-Bill issuance largely going to money market funds, and bank holdings actually falling modestly in net terms. The renewed contraction in the Fed’s balance sheet due to QT, and the May through July drop in the volume of usage of the Fed’s Reverse Repo facility certainly highlight the draining of excess market liquidity (also exacerbated by the Treasury rebuilding its Cash Balance at the Fed), and with bad loan and arrears provisions rising, the need for some balance sheet reconciliation, and more active risk management is pretty clear.

G7 flash PMIs are expected to be little changed, with Manufacturing PMIs expected to continue to contract across the board, above all in Germany (exp. 38.5 from 38.8), and Services readings were mostly seen expanding modestly, with the exception of France (exp. 47.5 from 47.1), but the actual outturns for Germany (47.3 vs. prior 52.3) and France (46.7) suggest that higher rates are starting to bite hard, despite the fall in energy prices. The steep fall in yesterday’s CBI Industrial Trends survey Volume of Output over past 3 months to -19 .vs -3, with Orders weaker than expected at -15 from -9 implies downside risks for the UK Manufacturing PMI, forecast at an already weak 45.0, and it will be interesting to note how the UK Services sector fares by comparison to the Eurozone.