Written Commentary

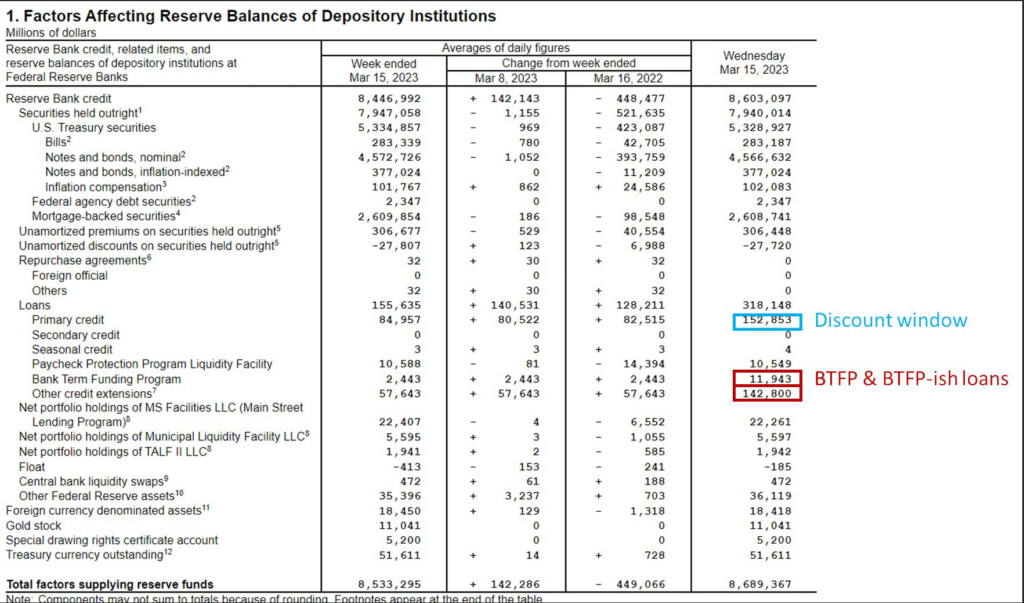

Yet another tumultuous week comes to an end, with a relatively modest schedule of data likely to be subordinated to ongoing banking sector concerns, and the likelihood of some divided ECB speak after yesterday’s council meeting. The statistical run has Singapore Trade data to digest, with Eurozone final CPI, Q4 Labour Costs and US Industrial Production and provisional Michigan Sentiment ahead, along with the OECD Interim Economic Outlook forecast update. Next week brings the Fed, BoE and SNB meetings, with surveys (flash PMIs and national business and confidence surveys) dominating the data schedule, accompanied by US New & Existing Home Sales and Durable Goods, while the UK looks to CPI, Retail Sales and PSNB. But with yet another bank rescue, this time a capital injection into First Republic by a group of GSIB’s led by JP Morgan and orchestrated with the Fed and Treasury, banking concerns remain to the fore despite some easing, and leave markets wondering where the next set of skeletons are going to be found. This was more than amply demonstrated by the £300 Bln increase in the size of the Fed’s balance sheet as reported last night, breaking down into Discount window: $153 Bln, New bank support measures (BFTB plus) $11.6 Bln and Credit extension $143 Bln (see table).

Fed weekly balance sheet report 16 March

** U.S.A. – Feb Industrial Production, Mar prov. Michigan Sentiment **

The US Industrial Production is expected to be bifurcated, with a modest 0.2% m/m rise in headline boosted by utilities output on the back of a reversion to more seasonable patterns, after a warm January. By contrast Manufacturing Output is forecast to fall 0.3% m/m, with the rise in the headline Manufacturing ISM obscuring the fact that both output and orders remained in contractionary territory, and thus predicting the consensus. Michigan Sentiment is seen unchanged at a lowly 67.0, with robust labour demand expected to be offset by signs that households are struggling with the rise in cost of living, as evidenced by a rise in credit card use and delinquencies on loans creeping higher. Whether the SVB collapse was captured in the survey period is an open question, and does pose a downside risk.