Written Commentary

EU Soft-Wheat Exports Rise 7.8% Y/y; Corn Imports Increase 66%

The European Union’s soft-wheat exports for the season that began July 1 reached 22.1m tons by March 19, compared with 20.5m tons a year earlier, the European Commission said on its website.

Wheat prices overnight are down 9 1/2 in SRW, down 7 3/4 in HRW, down 6 in HRS; Corn is down 1 1/2; Soybeans down 4 3/4; Soymeal down $0.36; Soyoil down 0.13.

For the week so far wheat prices are down 35 3/4 in SRW, down 22 1/2 in HRW, down 20 in HRS; Corn is down 5 3/4; Soybeans down 13 1/2; Soymeal down $0.83; Soyoil down 1.27.

For the month to date wheat prices are down 31 3/4 in SRW, down 1/4 in HRW, down 27 in HRS; Corn is down 1 3/4; Soybeans down 16 3/4; Soymeal down $10.10; Soyoil down 3.93.

Year-To-Date nearby futures are down 14.8% in SRW, down 8.4% in HRW, down 10.4% in HRS; Corn is down 7.4%; Soybeans down 3.7%; Soymeal down 4.3%; Soyoil down 11.9%.

Chinese Ag futures (MAY 23) Soybeans unchanged; Soymeal down 16; Soyoil down 162; Palm oil down 196; Corn down 37 — Malaysian palm oil prices overnight were down 117 ringgit (-3.09%) at 3667.

There were changes in registrations (-11 Soybeans). Registration total: 2,537 SRW Wheat contracts; 23 Oats; 73 Corn; 188 Soybeans; 613 Soyoil; 1 Soymeal; 88 HRW Wheat.

Preliminary changes in futures Open Interest as of March 21 were: SRW Wheat up 4,604 contracts, HRW Wheat up 719, Corn up 4,593, Soybeans up 3,386, Soymeal down 501, Soyoil up 3,065.

Brazil Grains & Oilseeds Forecast: Scattered showers are continuing over the interior of Brazil this week but will be spottier across southern and eastern areas. That will help increase the remaining safrinha corn planting. Soil moisture is good for the corn in the ground. Showers will decrease later this week over central areas as the wet season is showing signs of slowing down early — not a good outlook if that continues over the next few weeks as well.

Argentina Grains & Oilseeds Forecast: A front continues to bring scattered showers, sometimes heavy, to central Argentina early this week and then to northern areas later in the week. Rain is likely too late for much of the damaged corn and soybean crops. However, stabilization will likely occur if the showers are as heavy as forecast. Temperatures will remain above normal until a cold front moves through next week.

Northern Plains Forecast: Temperatures remain below normal for the next couple of weeks in the Northern Plains and Canadian Prairies, requiring higher inputs than normal for livestock and limiting snow melt. A system moves through Tuesday with scattered precipitation and some areas of moderate snow in the northeast, but the rest of the week is likely dry as systems pass by to the south.

Central/Southern Plains Forecast: Temperatures are higher for the next couple of days but will be squashed later this week as a cold front is slowly pushed southward through the region by a few storm systems. These systems will produce scattered precipitation across the region with the strongest storm in the series occurring Thursday into Friday, which has the best chance at bringing precipitation to the southwestern drought areas. There may be another over the weekend that could do so as well, but chances are low for meaningful precipitation outside of Kansas and Colorado’s winter wheat areas.

Midwest Forecast: A string of systems will push a cold front through the Midwest this week, bringing widespread precipitation through the region yet again. Another may come through this weekend into early next week. A wet end to March is likely to lead to some delays for early fieldwork heading into April. Temperatures will be waffling to end the month as well.

Black Sea Forecast: Dry and warm conditions will continue in the Black Sea region for most of this week before a front brings more showers through the region this weekend and into next week. Soil moisture is mostly good in the region and the warmth will help winter wheat to develop this week. The wheat crop is in good shape overall where not affected by war.

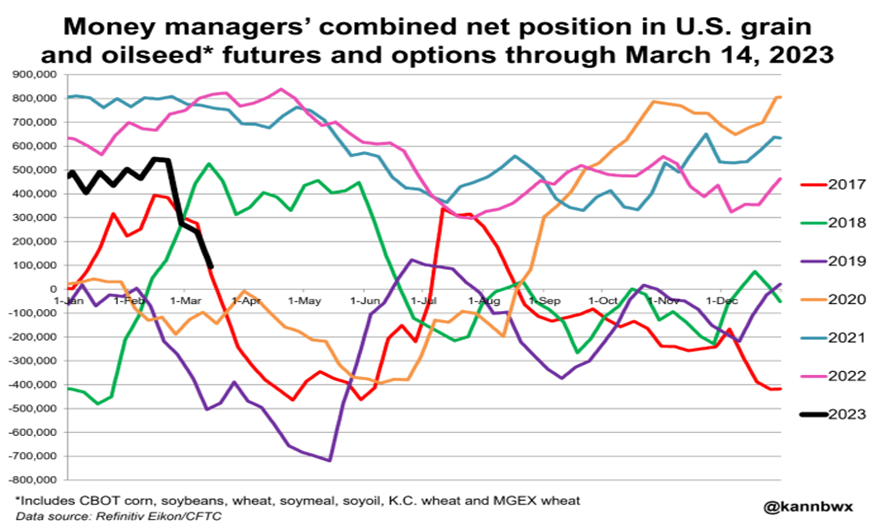

The player sheet for 3/21 had funds: net sellers of 5,000 contracts of SRW wheat, sellers of 2,500 corn, sellers of 8,500 soybeans, sellers of 1,000 soymeal, and sellers of 5,500 soyoil.

TENDERS

PENDING TENDERS

ETHANOL: US Weekly Production Survey Before EIA Report

Output and stockpile projections for the week ending March 17 are based on five analyst estimates compiled by Bloomberg.

Brazil’s Agroconsult sees soy exports at 96 mln T, a record

Brazil is expected to export 96 million tonnes of soybeans this year, a record, according to a forecast on Tuesday by agribusiness consultancy Agroconsult.

Brazil will also export above 50 million tonnes of corn this season, Agroconsult said, citing a favorable outlook for total corn production in the country in spite of an expected fall in plantings in some states.

Brazil 2022/2023 soybean crop forecast raised to 155 mln t – Agroconsult

Brazilian farmers will reap a record soybean crop of 155 million tonnes in the present cycle, even as drought conditions slashed yields in large producing states like Rio Grande do Sul.

After three months surveying soybean areas nationwide, agribusiness consultancy Agroconsult increased its current estimate from 153 million tonnes in a forecast released last month.

China Soybean Imports Seen Rising to 97.5M Tons in 2023/24: USDA

China’s soybean imports are forecast to rise to 97.5m metric tons in 2023-24, lifted by “modest” demand growth in the country’s animal feed industry, the US Department of Agriculture’s Foreign Agriculture Service says in a report.

EU 2022/23 soybean imports reach 8.45 mln T, rapeseed 5.87 mln T

European Union soybean imports in the 2022/23 season that started in July had reached 8.45 million tonnes by March 19, down 14.6% from 9.89 million by the same week last season, data published by the European Commission showed on Tuesday.

EU rapeseed imports so far in 2022/23 had reached 5.87 million tonnes, up 54% compared with 3.81 million tonnes a year earlier.

The bloc’s soymeal imports over the same period totalled 11.24 million tonnes, down 4.6% from 11.78 million the prior season, while palm oil imports stood at 2.65 million tonnes, 29% below a year-earlier 3.73 million.

However, the Commission said that it was still experiencing problems compiling grain trade figures from Germany and Italy.

Export data submitted by Germany from November may be inaccurate following the country’s switch to a new declaration system, while for Italy import data only went up to Jan. 13, it said in a note.

Russia Winter Crops Endure Winter Well

Russia’s winter crops endured the winter well, Interfax reported, citing Roman Vilfand, research director at the government’s weather center.

Paraguay Group Sees Russia Also Buying Soy Amid Argentina Demand

Russia will probably join Brazil in buying some of Paraguay’s soy beans this year even as Argentine crushing mills pay a premium for the oilseed after a drought devastated that country’s crop, said Hugo Pastore, executive director of grain and oilseed export group Capeco.

Interested in more futures markets? Explore our Market Dashboards here.