Written Commentary

SOYBEANS

Soybeans ended higher. Soyoil rally is helping soybeans. US diesel stocks are low. Soyoil based B100 can be used as an additive to diesel. Diesel is near $5.40 per gallon. This potential increase in soyoil demand pushed BOZ to new contract high. Brazil soybean planting is done forecast of rain next week could be ideal for the crop. USDA is already forecast a record Brazil 2023 crop. Argentina will soon begin to plant soybeans. Weather is dry but scattered rains are forecast for late next week. Some feel soybean futures are overpriced if 2023 SA crops are record high and global economies slow which good drop feed protein demand esp China. China Oct PMI data dropped.

CORN

Corn futures managed a small gain. Lower US Dollar and higher energy prices offered support. Finally there may be 2 chances for some NC US Midwest rains. The forecast was enough to drop barge freight sharply. USDA will be out next week. Most look for slight drop in US corn crop. Still, slow US export pace could force USDA to drop exports which could raise the US 2022/23 corn carryout. This week, China approved corn exports from Brazil. Brazil has record Oct 1 corn supply. There was talk that China may have bought Brazil corn. For Dec through April. USTR and Ag Sec are making Mexico ban on GMO corn a top priority. Key is If it includes over feed corn or just food. US barge feright collapsed on talk of 2 upper central Midwest rains that could help Miss river water levels USDA est Brazil 2023 corn crop record high. Rains could be finally dropping late next week over Brazil corn area. Argentina corn is 23 pct planted and in need of a rain. Crop rated at a level well below normal. 6 pct of the crop is rated G/E vs 82 ly. Will be interesting if USDA drops the crop. Pollination is normally around Christmas time. Ukraine is cheapest export corn followed by Brazil. Still no confirmation that Russia will extend the Ukraine export deal that expires Nov 19. Ukraine war continues to escalate. Some feel corn futures are overpriced given slow export demand.

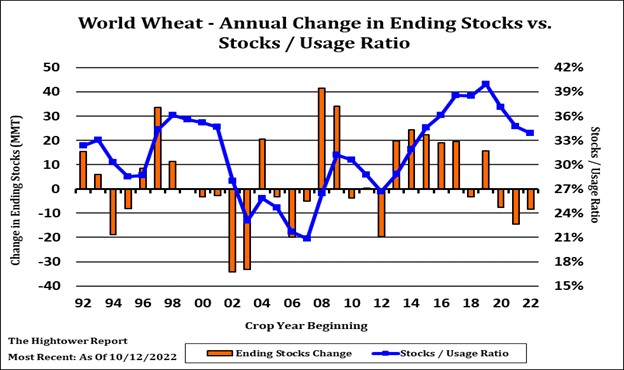

WHEAT

Wheat futures ended mostly higher. Weekly US wheat export sales were low but lower US Dollar and higher commodity trade may be offering support. Trade is not looking for big USDA changes in US 2022/23 US wheat carryout or World end stocks. Argentina is still dry. Argentina dropped their wheat crop to 14 mmt vs USDA 17.5. Argentina will allow exporters to roll forward 8.4 mmt export licenses. They own only 3.1 mmt. That could suggest a 5 mmt World trade shortfall. E Australia is getting a break for too much rain. Harvest has been delayed. Rains though return next week. Rare to see a fall rally in wheat futures due to drop in South Hemisphere wheat crops. US south plains is also dry. This week US winter wheat crop rating was record low for last week. Still no official word that Russia will extend Ukraine export corridor deal. Russia is asking that one of its large state Bank be exempted from sanctions to help increase Russia grain and fertilizer exports. UN would like the increase to lower World food and fertilizer prices. This could also help chances that the Ukraine export corridor deal could be extended.

See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.