Written Commentary

The soybean complex finished mixed in choppy 2 sided trade. Beans were down $.08-$.09, meal was $1 higher while oil plunged $.01 ½ lb. Nearby bean spreads firmed up with Jan-25/Mch-25 closing at $.08 ¾, a 4 month high. Oil spreads weakened while meal spreads were mixed. Jan-25 beans briefly dipped below LW’s low, however held above this month’s low at $9.82. Resistance is at the 50 day MA, currently $10.21 ¼. Dec-24 meal continues to hover just above its contract low of $285.30 with long term support at the Aug-2020 low near $280 ton. Bean oil broke down to a new low for the month as speculators lighten up on their long positions. Next support for Dec-24 is the 100 day MA at 42.86. Talk of China offering BO for export into SE Asian countries also contributed to the price weakness. Spot board crush margins fell another $.07 to $1.22 ½ bu. a 5 month low. Bean oil PV fell to 42.8%, a 4 week low. Dry areas in central Argentina are expected to see a healthy dose of rain the first half of next week. Recent dryness in southern growing areas of Brazil have started to receive beneficial rain. A good mix of rain and sunshine is expected for most areas of Brazil into early December. An area of possible concern is in Sao Paulo and N. Parana where moisture is expected to be lite. The USDA announced the sale of 226.2k mt (8.3 mil. bu.) to an unknown buyer and 202k mt (7.4 mil. bu.) to China. Chinese customs data showed they imported 541.4k mt of soybeans from the US in Oct-24. While double what they imported from the US in Oct-23, they were still a tenth of the 5.53 mmt they imported from Brazil, and less than half of the 1.36 mmt brought in from Argentina. In the first 10 months of 2024 imports for the US have reached 15.1 mmt, down 13% from YA, while imports from Brazil at 67.8 mmt are up 13.6%. At midday Brazil’s Ag. Ministry announced they have struck a deal with China to open markets to sorghum, fishmeal, sesame and other Ag. products. Export sales tomorrow are expect to range from 35-55 mil. bu. of beans, 5-25k tons of oil, and 200-450k tons of meal.

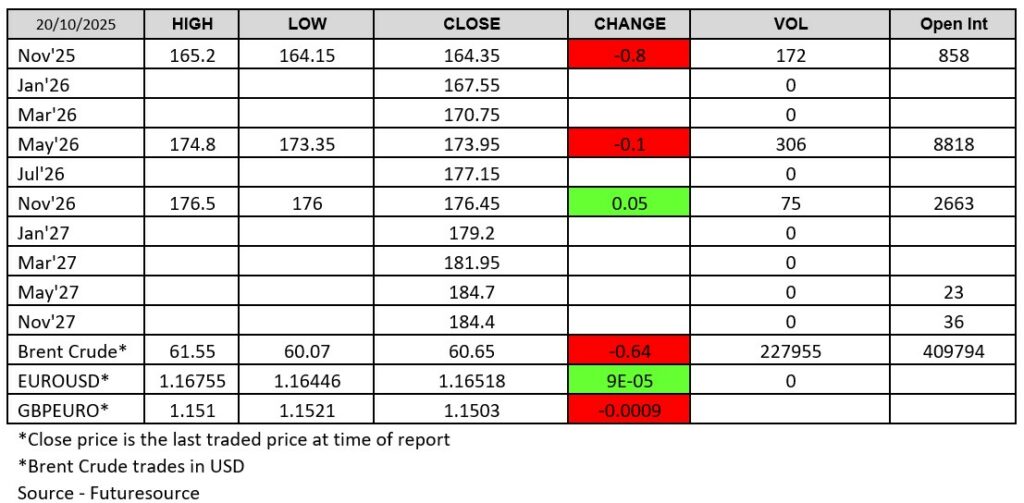

Prices finished $.02-$.05 higher across all 3 classes today. KC and MGEX traded above yesterday’s high with next resistance at the 100 day MA’s of $5.76 and $6.12 ¾ respectively. After passing on yesterday’s tender, Jordan is seeking 120k mt of wheat in a new tender that expires Nov. 26th. Algeria has reportedly bought 160k-180k mt of durum wheat between $348-$360/mt CF, depending on the vessel size. The wheat is for Jan/Feb shipment with Canada, the US or Australia likely the country of origin. Wire services are reporting Russian farmers will likely start planting less wheat following this year’s heavy losses. Despite tight stocks among global wheat exporters production from southern hemisphere exporters, where harvest is ongoing, is expected to be up 18% from YA which seems to be keeping a lid on rally attempts. Export sales tomorrow are expected to range between 10-22 mil. bu.

All charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.