Written Commentary

CORN

Prices were $.01½-$.03 lower today as spreads continue to firm. Dec-24/Mch-25 traded into $.11 ½ the highest in 4 ½ months. Strong demand and limited farmer selling is forcing spreads to tighten to keep the pipeline full. US rains this week will favor the ECB with another system impacting the Southern plains late this weekend into early next week. While I’d expect US drought readings to ease further in the Midwest and winter wheat growing areas, the northern plains will likely see drought conditions expand. Export inspections at 31 mil. bu. were in line with expectations. YTD inspections at 324 mil. are up 31% from YA vs. the USDA forecast of up 1.4%. Mexico was the only noted buyer with nearly 16 mil. bu. Still surprised the USDA made no change to their export forecast of 2.325 bil. bu. last Friday. I look for this forecast to work higher over time. The USDA also announced the sale of 110k mt (4.4 mil. bu.) to Mexico. Algeria is seeking up to 240k mt of SA feed corn for late Dec-24 shipment. I look for US corn harvest to have reached 95% as of Sunday. EU 24/25 corn imports as of Nov. 10th have reached 7.1 mmt, up 8.2% from YA.

The soybean complex was lower across the board today with beans down $.12-$.14, meal was $1-$2 lower while bean oil was down 180-190. Bean spreads were firmer while spreads for both products weakened. Jan-25 beans rejected trade above its 100 day MA both Friday and Monday. Prices were able to hold above the $10.00 level. Dec-24 meal established a new contract low today, trading to the lowest level since Aug-2020. Concern that Indonesia may slow its move to a diesel blend containing 40% biodiesel contributed to the selloff in vegetable oil prices. Sources indicate they are considering phasing in the higher blend over the first 6 months of 2025 in order to allow palm oil production a chance to expand, rather than beginning in January. Spot board crush margins plunged $.17 today to $1.50 bu., matching a 2 month low, while bean oil PV slipped to 44.1%. NOPA crush from October is due out at 11 AM CST on Friday. Rains will favor central and northern growing regions of Brazil for the next week to 10 days. A dryer weather pattern is expected across southern Brazil and Argentina this week with better prospects for rain in week 2. Export inspections at 84 mil. bu. were in line with expectations. Last week’s inspections were revised up 5.5 mil. bu. bringing YTD inspections to 560 mil. up 6% from YA vs. the USDA forecast of up 7%. China took 58 mil. bu. As expected the USDA lowered their export forecast 25 mil. bu. to 1.825 bil. Late yesterday the Rosario Grain Exchange suggested that following recent rains, Argentine farmers would work quickly to seed this year’s soybean crop. Plantings were at 8% as of late last week. EU soybean imports as of Nov 10th had reached 4.43 mmt, up 6.7% from YA. Meal imports at 6.53 mmt are up 18%.

After mixed, quiet trade overnight wheat prices plunged $.12-$.14 with all 3 classes trading to their lowest levels in 2 ½ months. Expected improvement for the US winter crop along with a seemingly friendlier relations between US/Russian under the incoming Trump administration seem to have fueled to bearish sentiment. No significant drought relief is expected for Western Russia, Ukraine and western Kazakhstan over the next week to 10 days. Dec-24 Chicago premium over Dec-24 corn settled below $1.25, its lowest close in 8 months. Export inspections at 13 mil. bu. were also in line with expectations however just below the 15 mil. needed per week to reach the USDA forecast of 825 mil. bu. YTD inspections at 371 mil. are up 35% from YA, vs. the USDA forecast of up 17%. Jordan reportedly bought 60k mt of optional origin wheat for $269/mt CF for Feb-25 shipment. EU soft wheat exports for 24/25 at 8.34 mmt are down 30% from YA. I look for US winter wheat ratings to improve 4% to 45% G/E.

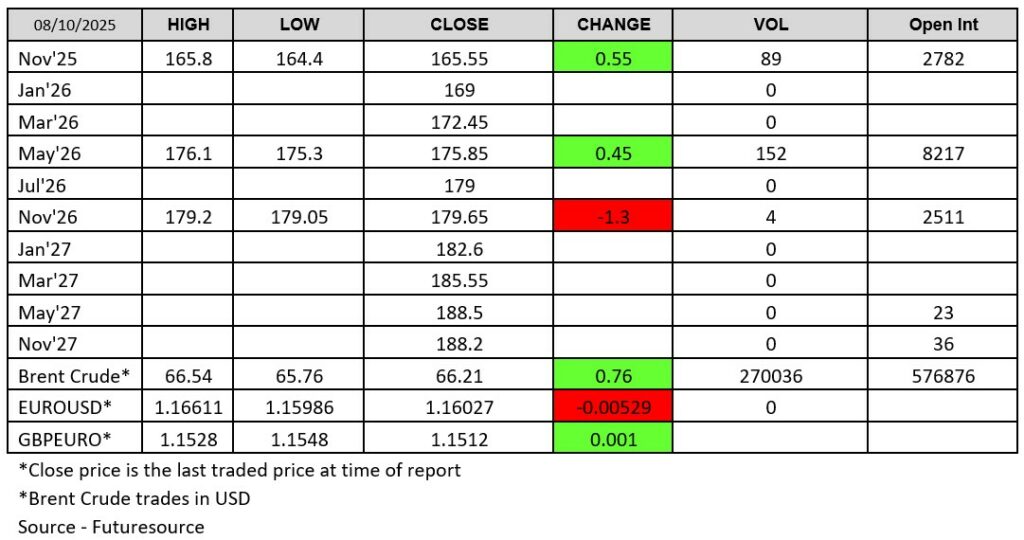

All charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.