Written Commentary

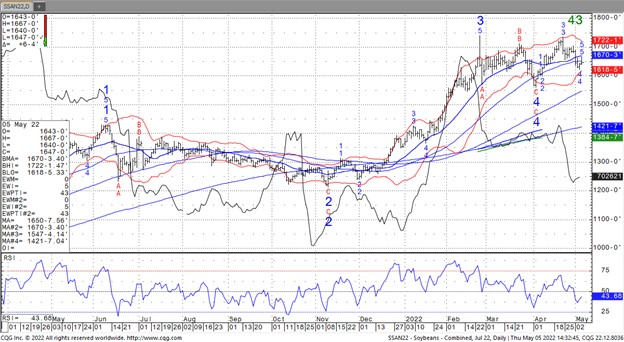

SOYBEANS

Soybeans were higher led by the May. US domestic soybean basis is firmer. May open interest is down to only 1,866 contracts. Total soybean open interest is down to 702,900 from a high in Feb of 863,000. There were no new daily US soybean sales announced. Soymeal gained on soyoil. Lower palmoil prices due to demand concerns is offering resistance to soyoil Weekly US soybean export sales were near 734 mt. Total commit is near 58.3 mmt vs 61.2 ly. USDA goal is 57.5 mmt vs 61.5 ly. New crop sales rose 407 mt with unshipped open sales near 11.1 mmt. Trade unable to push over 17.00 SN. This limits new buying. Key will be US spring and summer weather.

CORN

Corn futures edged higher. CN continues to trade in a broad range between 7.80 and 8.20. 7.80 tends to trigger new unpriced demand and is too low if US corn export demand increases from USDA latest guess. Near 8.20 prices tend to slow demand. Total open interest has dropped from a high in mid Feb near 1,624,000 contracts to 1,511,000. Slowdown in new farmer selling and end users rolling needs forward hoping for lower prices has reduced open interest. May option open interest expiration also dropped OI. Weak energy and financial markets today and higher US Dollar may be limiting new buying in corn futures. Still, US corn demand should be higher which could drop US 2021/22 carryout. US Midwest 2 week forecast calls for warmer and drier weather. This week is wet. US farmers should be able to plant the crop starting next week. Some feel yields begin to drop for corn planted after May 10. But from where? One key could be USDA crop and yield est on May 12. USDA has no reason yet to drop the yield below 180.

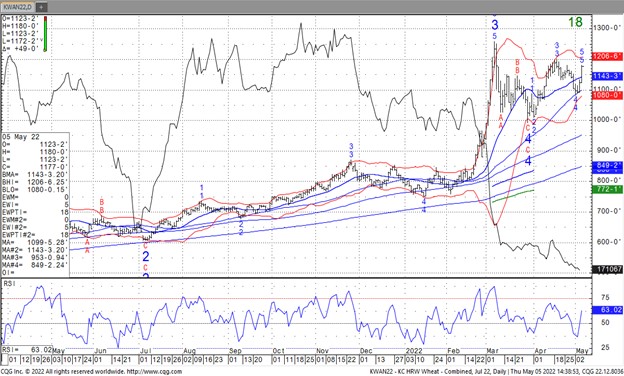

WHEAT

Wheat futures continued to trade higher. It is still not clear if India will ban wheat exports. Still most feel their crop is below domestic demand which could limit new exports. It is dry in Pakistan, EU and Bangladesh. Pakistan and Bangladesh could be net importers of wheat. Matif new crop futures are making new highs on feelings that their exports may need to increase to help offset lower Black Sea exports. US north plains forecast is still wet. US south plains is expected to turn warmer and drier soon. Weekly US wheat export sales were 118 mt. Total commit is near 19.4 mmt vs 25.5 last year. USDA export goal is 21.3 mmt vs 27.0 ly. USDA est total World exports at 200.1 mmt vs 202.6 ly. Russia 33.0 vs 39.1 ly, Ukraine 19.0 vs 16.8?, EU 34.0 vs 29.7, Canada 15.5 vs 26.4, Australia 27.5 vs 23.8 and India 8.5 vs 2.5 ly

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.