Written Commentary

SOYBEANS

July soybeans closed sharply lower on the session and experienced the lowest close since April 11th. The surge higher in the dollar index plus weakness in the energy market and a selloff in the corn market were all seen as bearish forces. Severe lockdowns in China has traders nervous about their economy, and the soybean oil market is showing aggressive selling following Friday’s key reversal from an all-time high. The meal market is also trading sharply lower and the selling pushed the market down to the lowest level since February 1. For the weekly export inspections report, traders were looking for soybean inspections near 500,000–1.0 million tons. Inspections came in at 601,282 metric tonnes. Cumulative inspections year-to-date are 47,206,500 metric tonnes which is 15.2% below last year. This is 82.0% of the USDA’s forecast for the 2021-22 marketing year versus the five year average of 78.3%. For the weekly crop progress report, traders see soybean planting at 8% complete, 5–10% range, as compared with 3% last week.

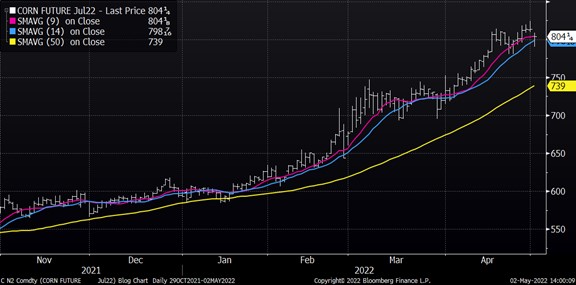

CORN

The gap lower opening for December corn after a key reversal on Friday is a bearish technical development. The market closed lower on the session but close to the highs. Talk of some dryness in the Dakotas and Minnesota, and some warmth in the 6-10 day forecast helped to pressure the market. In addition, the sharp selloff in the crude oil market and a continued strong advance for the US dollar were seen as bearish forces. For the weekly export inspections report, traders expected 1.0-1.775 million tonnes. Corn export inspections for the week ending April 28 came in at 1,683,994 metric tonnes. Cumulative inspections year-to-date are 36,577,009 metric tonnes which is 16.1% below last year. This is 57.6% of the USDA’s forecast for the 2021-22 marketing year versus the five year average of 60.4%. For the weekly crop progress report, traders see corn planted area near 16% complete, 12 – 24% range, as compared with 7% planted last week. Lower their second corn crop estimate from Brazil with one estimate out today at 88.1 million tons as compared with 91.9 million as their previous estimate. Dry weather seems to be impacting the filling stage and helping to reduce yield.

WHEAT

July wheat closed slightly lower on the day and up more than 20 cents from the lows. Some dryness in the short-term forecast for the Dakotas plus hefty rain amounts for Kansas and hard red winter wheat growing areas are factors which helped pressure the market. The early weakness in corn and soybeans was also seen as a negative force, and a surge higher in the US dollar also helped to pressure. Talk that India’s crop might be down about 6% from the early estimates due to a heat wave at the tail end of harvest helped to support. India experienced the hottest March in 122 years, and the heat continued for much of April. At this point, when India expected a record crop, traders were believing that they could export near 12 million tonnes. Traders expected 225,000–500,000 tonnes for export inspections, but they came in at 384,460 metric tonnes. Cumulative inspections year-to-date are 18,755,678 metric tonnes which is 19.1% below last year. This is 87.8% of the USDA’s forecast for the 2021-22 marketing year versus the five year average of 86.7%. For the weekly crop progress update, traders expect to see winter wheat crop rated 28% good/excellent with a range of 25% to 30%. Spring wheat planting progress is expected to have reached 20% complete, 15–23 range, as compared with 13% last week.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.