Written Commentary

SOYBEANS

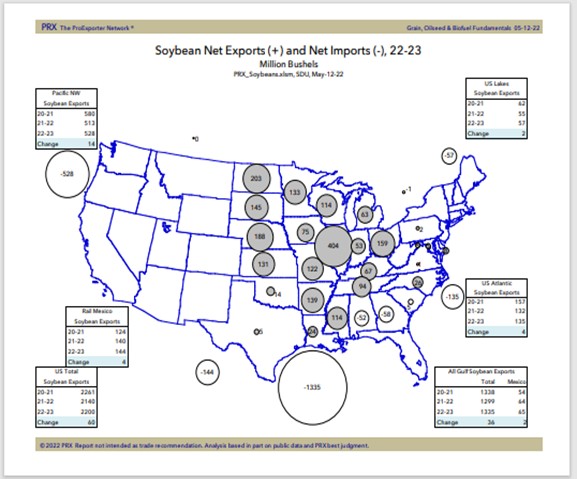

Nearby soybeans ended higher. SN gained on SX. Soyoil gained on soymeal. Talk of higher US crush and export demand. There is talk that due to higher crush margins, some soybeans are moving from export to crush. This could add to meal supplies. US soybean planting pace is now near 30 % vs 12 last week. IL is 38% planted, up 27% on the week, IA 34%, up 27%, IN 28%, up 21%, MN 11%, up 9%, NE 44%, up 16%, SD 15% up 10%, ND 2% up 2%, OH 18%, up 14%. SN is above Mondays high and over the 20 and 50 DMA. 17.00 SN is key resistance. Higher US soybean demand should push SN over 17.00. China remains the biggest soybean short in the market. At the halfway point, China total soy imports from all destinations are down 6 pct YoY at 51 mmt. Most estimate total China soybean imports closer to 94 mmt vs USDA at 92.

CORN

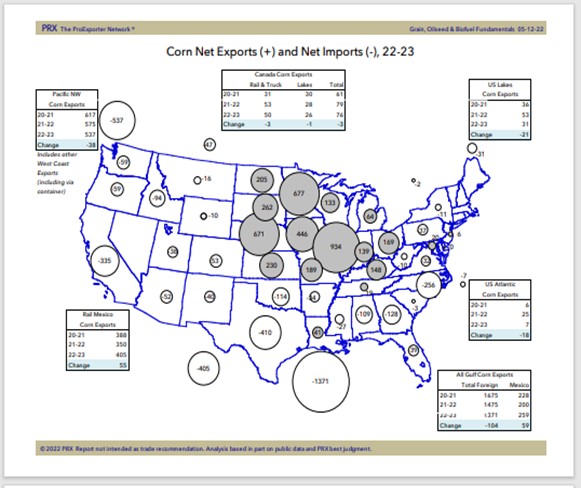

Corn futures traded lower. CZ gained on CN. Some feel US corn crop will get planted. Slow US weekly corn exports may be offering resistance. Some feel that corn export demand will increase in the fall. October corn elevations are +60 cents. Some thought US corn export demand would increase Jan 1. Higher October elevations suggest exports could increase in October. Some feel total US weekly US exports could test previous high of 160 mil bu including 80 corn and 40 soybeans. Global end users are not covered Q3 and Q4. US corn is 49% planted versus 78% ly and 66% 5-year average. IL is 55% done, up 40% on the week, IA 57%, up 43%, IN 40%, up 29%, MN 35%, up 26%, NE 62%, up 23%, SD 31%, up 20%, ND 4%, up 3%, OH 31%, up 26%, and MI 31% up 27%.

WHEAT

Wheat futures have had a wild trading day. India banning exports, dry US south plains, south EU and wet weather in ND and east Canada weather offers support. US spring wheat crop is 39 pct planted vs 27 last week. US winter wheat crop is rated 27 pct G/E vs 29 last week. IL is 52%, up 7%, IN is 65%, up 4%, OH is 60%, up 4%. TX is 5% G/E down2%, Oklahoma 13%, down 7%, and Kansas is 24%, down 4%. US winter wheat is rated 39% poor to very poor. WN is near 12.77 with a range of 12.00-12.84. KWN is near 13.69 with a range of 12.98-13.79. MWN is near 13.93 with a range of 13.40-14.12. The EU has cut its forecast for 2022 economic growth to 2.7% for 2022 and 2.3% for 2023. This is down from their February forecast of 4.0% and 2.7% respectively. Inflation is expected to be 6.1% for 2022 and 2.7% for 2023. This is compared to a previous forecast of 3.5% and 1.7%. Most of the hit to GDP and rise in inflation is tied to the war in Ukraine and subsequent rise in energy prices.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.