Written Commentary

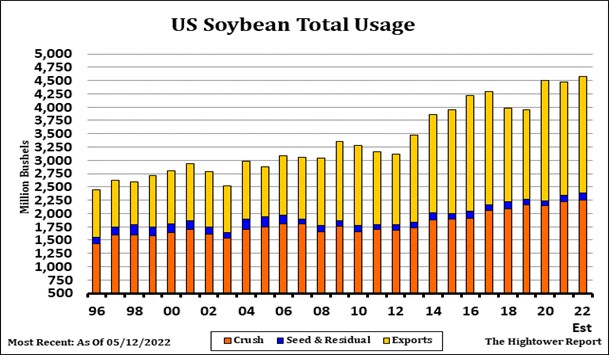

SOYBEANS

Potential change to a drier US Midwest weather pattern helped beans. China buying US soybeans also helped beans. July soybeans bounced back over 17.00. Talk that China increased buying nearby Argentina soybeans, fall US soybeans and 2023 Brazil soybeans helped the basis and July gaining on back months. USDA estimated that 78 pct of the US soybean crop is planted. Some feel some of the 2022 intended soybean acres may not get planted. There are some that estimate now that US 21/22 soybean exports could increase to 2,200 mil bu vs USDA estimate of 2,140. This could tighten US old crop supplies. This is helping the US domestic basis. US farmers are focusing on spring fieldwork and not marketing grain. This is helping SN gain on back months.

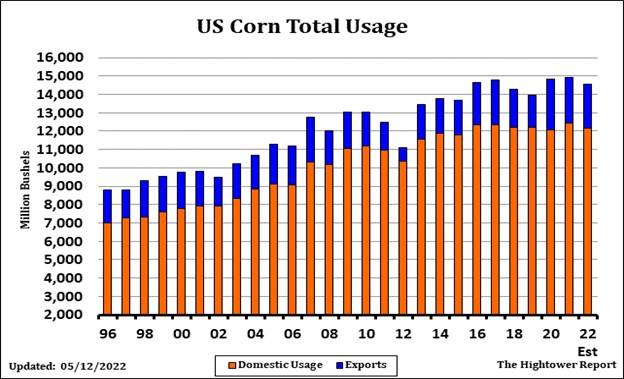

CORN

Corn has found support on talk of a ridge developing over the east Midwest. Overnight EU model was pretty impressive. American models are not as impressive. Key is the jet stream. Some feel rains will move over the top of the ridge that will keep US south plains dry but north plains and east Midwest could remain wet. Some feel there is now a 50-50 pct chance a permanent ridge could develop in the west in July. US cash domestic corn basis remains firm in expectations of increase US export demand. Some feel final US corn exports could be closer to 2,700 mil bu vs USDA 2,500. This also includes fact to date US census exports are 290 mil bu above inspections. EU barley prices are $60 above US corn. USDA estimated that 94 pct of US Corn crop has been planted. Still, there are 684,000 corn acres yet to be planted in ND, 546,000 in MN and 434,000 in SD. Long range US west Midwest Weather maps hint of some ridging. Rains could move across the ridge including ND, MN, WI, IL, IN and OH. SD, W IA, NE, KS, CO, OK and TX could turn warmer and drier. Some feel Brazil final corn crop could be closer to 107 mmt vs USDA 116 and Argentina 49 mmt vs USDA 52. Where will World, buyers find 12 mmt of lower South America supply especially if Ukraine ends up with restricted grain exports. .

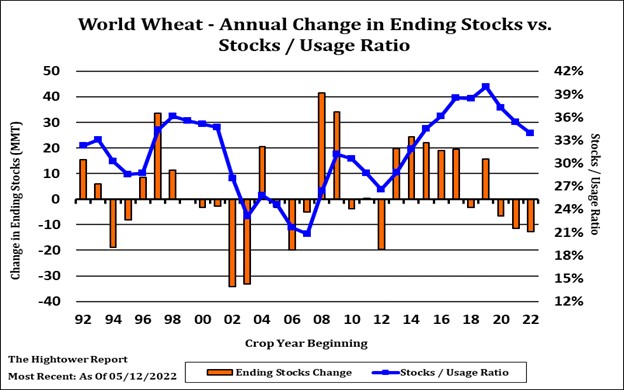

WHEAT

Wheat is again wheat. Down, up then down again. Wheat ended down on concern about demand and approaching US winter wheat harvest. Some selling today was attributed to more rumors of a corridor for Ukraine exports to be given to ship Ukraine grain. Most doubt anything solid can come from tomorrow meeting between Turkey and Russia, Ukraine will need assurance that US or UK defense boats would escort grain shipments. Most doubt Russia or Turkey would agree to that. Trade estimates US 2022 wheat crop near 1,713 mil bu vs USDA 1,729. Combines are stopped due to rains but OK/TX yields are below average and some are concerned that rains could begin to lower quality. There remains 2.0 million US spring wheat acres unplanted

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.