Written Commentary

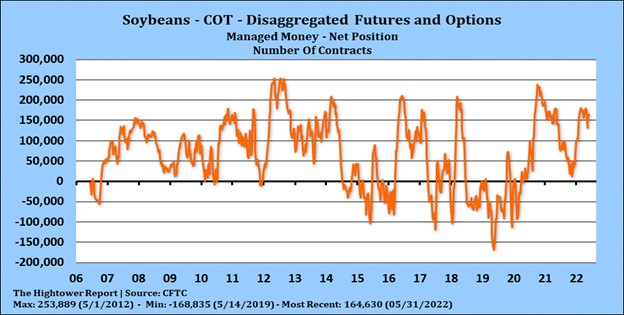

SOYBEANS

Weekly US soybean exports were 12.8 mil bu vs 14.8 last week and 8.8 last year. Season to date exports are 1,831 vs 2,090 last year. USDA goal is 2,140 vs 2,261 ly. Soybean futures have found resistance on talk that China is not asking for US prices. There is talk that China will lessen covid restrictions. This could increase China commodity imports. There is also talk that the Biden administration may drop China tariffs later this week. Trade estimates that US soybean plantings are near 80 pct vs 66 last week. Some estimate that this week USDA may not make many changes to US/World supply and demand. Still some feel South America soybean crop could be lower and final US soybean exports could be higher. Some feel US 2021/22 carryout could be closer to 190 mil bu vs USDA 310 and 2022/23 closer to 200 vs USDA 310. That could suggest nearby soybean futures could test 18.00 before US harvest.

CORN

Trade will be watching US central Bank action in raising interest rates. There remains estimates that US Fed will increase rates 50 basis points in June, July and September. There are also estimates that Crude could test 147. US gas a diesel prices are at all time highs. Weekly US corn exports were 56.4 mil bu vs 55.5 last week and 56.1 last year. Season to date exports are 1,721 vs 2,071 last year. USDA goal is 2,500 vs 2,753 ly. US census corn exports are running 260 mil bu above inspections. Corn futures have found support on talk that Ukraine will not accept any Russia and Turkey plan to open Ukraine grain exports. There is talk that the Biden administration may drop China tariffs later this week. Weekend 2nd week US Midwest weather maps suggested a dirty south central ridge day 11-12. Morning maps were not as dry. Trade estimates that 93 pct of US corn crop is planted vs 86 last week. USDA first weekly corn crop rating could be 68 pct G/E. Some estimate that this week USDA may not make many changes to US/World supply and demand. Still some feel South America corn crop could be lower and final US corn exports could be higher. Some feel US 2021/22 carryout could be closer to 1,350 mil bu vs USDA 1,440 and 2022/23 closer to 1,200 vs USDA 1,360. That could suggest nearby corn futures could test 8.00 before US harvest.

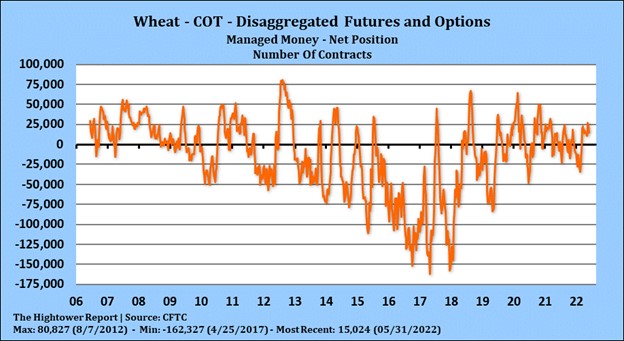

WHEAT

Weekly US wheat exports were 12.9 mil bu vs 12.6 last week and 19.5 last year. June starts a new marketing year. Season to date exports are 8 vs 7 last year. USDA goal is 775 vs 805 ly. Wheat futures have found support on talk that Ukraine will not accept any Russia and Turkey plan to open Ukraine grain exports. Russia also bombed key Ukraine ports over the weekend and shelled grain elevators. Dry weather across parts of EU, Ukraine, south Russia, north China plains and Argentina offers support. Wet weather continues in ND and east Canada HRS area. Matif was up over €21 at the highs as severe weekend wind and hail storms added to the Ukraine events, taking over from the drought across much of France and potentially adding yet another problem to the World wheat S&D. It is too early to get any real assessment of the damage from the storms, but the French Farmers’ Union FNSEA said it was ‘significant’ and talked of 100% losses for some farms. Trade estimates US winter wheat crop 30 pct G/E vs 29 last week with harvest near 6 pct. OK/TX yields are well below average. US HRS plantings are estimated near 86 vs 73 last week.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.