Written Commentary

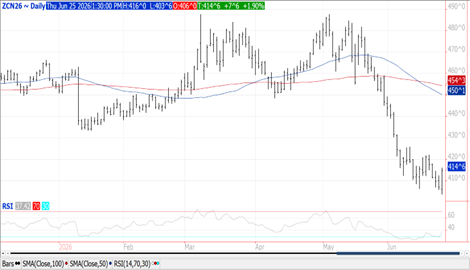

Prices jumped $.07 ½ – $.08 ½ today after establishing new contract lows overnight. Key reversals were carved out for all future contracts out to July-27. Despite the strength nearby spreads eased ahead of FND for the July-26 contract which is less than 1 week away. Prior to the turnaround July-26 also filled the gap from last September on the weekly chart. Yesterday’s EIA report showed ethanol production slipped to 320 mil. gallons last week, below expectations and the pace needed to reach the USDA corn usage estimate for a 10th consecutive week. Also, late yesterday the Trump Admin. urged the Senate to pass legislation allowing the year-round sale of E-15. For next week’s USDA update I see corn acres dipping to 94.75 mil. while my June 1st stocks est. is 5.425 bil. bu. The Ave. estimate in the Bloomberg survey shows acres at 95.1 mil. down from 95.3 in March with stocks at 5.414 bil. vs. 4.643 bil. YA. Export sales at 58 mil. bu. were in line with expectations. Old crop commitments at 3.333 bil. bu. are up 25% YOY vs. the USDA forecast of 16%. Noted buyers were Japan – 16 mil., and Mexico – 24 mil. New crop commitments have reached 212 mil. bu. a 4-year high while up 50% YOY. The spread between Spot Dalian futures in China and US Gulf corn has widened out to just over $150/mt, the widest in nearly 2 years. Perhaps an interest in US corn soon ?

Prices were sharply higher across the complex in 2-sided trade. A strong recovery in the agricultural space today was driven by a turnaround in the US $$$, a more threatening US forecast along with indications China is seeking offers for US beans for Sept/Oct delivery. Beans were up $.19-$.22, meal was $4-$5 higher while oil was up nearly $.01 ½ lb. Despite the strength nearly bean spreads traded to new low ahead of FND. Product spreads were mixed. Both July and Nov. beans made new lows for the week, however held support above their respective June lows. Near-term resistance for July-26 is at LW’s high just above $11.40. July-26 oil held support above its 100-day MA before rebounding. S&P Global calculates the B/E price for bean oil for a California RD manufacturer has fallen to $.87 lbs. following a drop in diesel prices. D4 RIN values have held up well at just under $2.40. Bean prices will continue to be sensitive news surrounding Chinese demand. US FOB offers at the Gulf are back to a slight premium over Brazilian offers for July/Aug-26, while slightly below Sept-26 forward. Spot crush margins jumped $.06 today to $3.29 ½ bu. while bean oil PV rebounded to 53.5%.

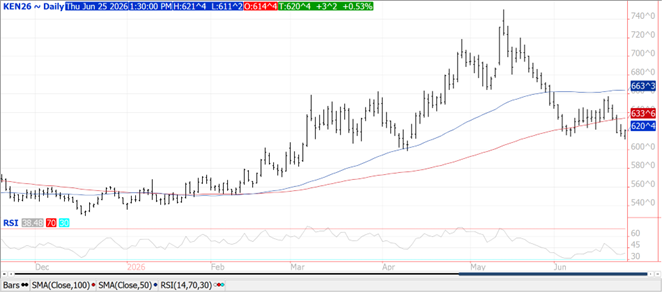

Prices ranged from $.02 lower for deferred MIAX futures to $.05 higher in CGO futures. CGO July-26 was up $.05 ¼ at $5.91, KC July-26 was up $.03 ¼ at $6.20 ½ , while MIAX July-26 was $.03 higher at $5.87 ¼. July-26 KC traded to a 2 ½ month lower before recovering. Inside trade for MIAX July-26 after establishing a new contract low yesterday. Export sales of 18.5 mil. bu. were in line with expectations as US prices have become more competitive. YTD commitments at 202 mil. bu. are down 17% from YA vs. the USDA forecast of down 15%. By class sales were HRW – 5 mil, HRS and white 4.3 mil. each, SRW – 4 mil., and 1 mil. bu. of durum. Heavy rains across the S. Midwest will continue to slow SRW development and harvest.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.