Written Commentary

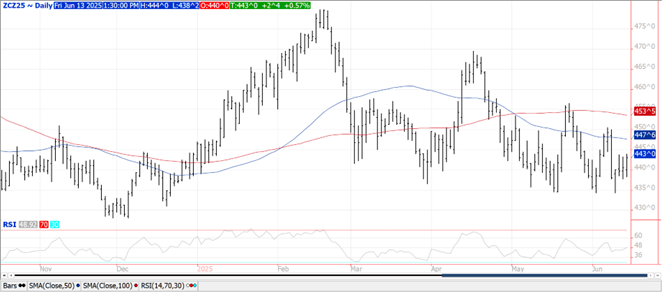

Price were $.02-$.06 higher today with July-25 the upside leader. With US old crop inventories tight and the Goldman roll now over, look for July-25 to gain on new crop Dec-25. US weather remains mostly favorable as much of the nation’s midsection will see a good mix of rain and sunshine over the next 2 weeks. The past 24 hours showed healthy rains across E TX, the Gulf coast and S. Midwest. Pockets of heavy rain also noted across the N. Midwest and W. NE, an area still impacted by severe drought. The market has been treating the strong US demand as old news as future demand shifts to SA. Dec-25 has been grinding sideway in a $4.35-$4.50 range looking forward to the month end stocks/acreage data. Next resistance for July-25 is this month’s high at $4.51. The BAGE places Argentina corn harvest at 47% while holding their production forecast unchanged at 49 mmt, vs. the USDA est. of 50 mmt.

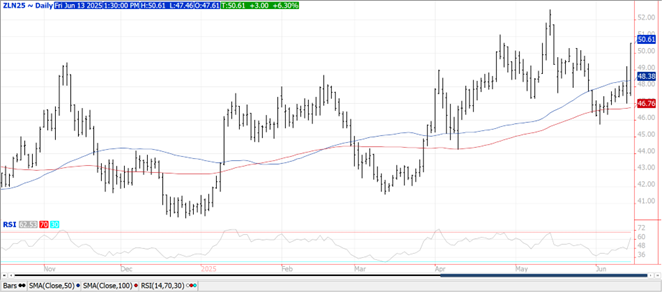

Prices were sharply mixed across the complex. Beans were up $.25-$.28, oil was locked limit up $.03 lb. all the way out to Sept-26, while meal was down $3 per ton. Next resistance for July-25 beans is last month’s high at $10.82 and $10.65 ½ for Nov-25. Expanded limits on Sunday night of $1.15 bu. for soybeans, $.04 ½ lb. for oil and $60 per ton for meal. Today the US EPA proposed target for biomass-based diesel rise to 5.61 bil. gallons in 2026 while growing to 5.86 bil. in 2027. Current mandates cover only 3.35 bil. gallons. US biodiesel and RD capacity has been over 6.5 bil. gallons annually for the past year. The EPA went on to state they expect to announce small refinery waiver policy before finalizing proposed blending requirements. The BAGE placed soybean harvest in Argentina at 93%, up 4% for the week while increasing production .3 mmt to 50.3. The USDA is stuck at 49 mmt. NOPA crush on Monday is expected to show NOPA members processed nearly 194 mil. bu. in May, which if realized would be a record high for the month. Estimates range from 188.5-196 mil. bu. Bean oil stocks are expected to fall 5% from April to 1.450 bil. lbs. and if realized would be off nearly 16% from the 1.724 bil. lbs in May-25. Although the USDA lowered their old crop bean oil usage for biofuels 200 mil. lbs. yesterday to 12.90 bil. lbs. they kept 25/26 usage unchanged at a record 13.90 bil. lbs.

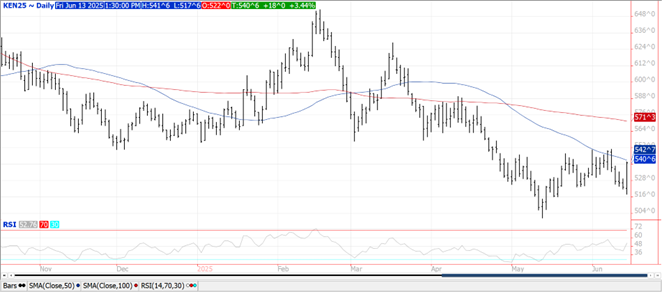

Prices surged $.16-$.18 across the 3 classes drawing support from the surging bean and oil prices along with heavy rains slowing winter wheat harvest. July-25 Chicago closed back above its 50 day MA with next resistance at the 100 day at $5.61. The rally in July-25 KC stopped just short of its 50 day MA at $5.42 ¾. The BAGE places Argentine plantings at 38.5% advancing 15% for the week. Drought conditions across EC China will see relief with several opportunities for rain in coming weeks. Tunisia reportedly bought 100k mt of soft wheat at an average cost of $244.50/mt CF for July/Aug shipment. Stocks/use ratio among global exporters slipped to 15.6% in June down from 16.4% in May, comparable with YA.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.