Written Commentary

SOYBEANS

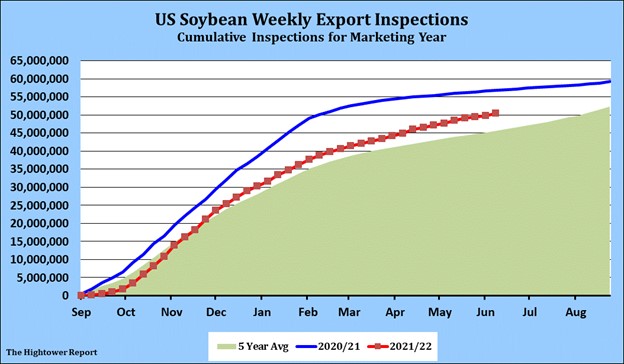

Black Monday for commodities. Talk of US inflation getting worse, US Fed raising interest rates this week, in June and in September plus new concerns about food and fuel demand, Ukraine war and new covid cases in China weighed on prices. The rally in the US dollar brought in crude oil selling, pulling soyoil and the soy complex lower. US Midwest weather will be hot and dry this week. More normal weather is forecast for Midwest next week. US weekly soybean exports were near 605 mt. Total soybean exports to date are 50.4 mmt vs 57.0 ly. USDA goal is 59.0 vs 61.5 ly. First soybean crop rating is estimated near 70 pct G/E. Soybean plantings should be 90 pct done. SN tested first support near 17.05. Next support is 16.71. Resistance is near 17.50.

CORN

Corn closed mixed. String of 8 straight up days ended with most commodities trading lower. Managed funds continued to liquidate longs on less concern about US Midwest weather, declining market profits and before first notice day. With the FOMC meeting in focus as we move past the CPI numbers on Friday the US dollar is at 20 year highs. The odds for a 50 basis point rate hike are high, but do not rule out a 75 basis point hike. With chatter of US inflation not peaking until at least 9% we may see a 75 bp rate hike come July 26/27, the next FOMC meeting dates. Black Monday for commodities and equites. Concerns about food and fuel demand, Ukraine war and new covid cases in China is weighing on prices. US Midwest weather will be hot and dry this week. More normal weather is forecast for Midwest next week. US weekly corn exports were near 1,199 mt. Total exports to date are 44.9 mmt vs 54.2 ly. USDA goal is 62.2 vs 69.9 ly. Some could see exports closer to 68.7. Trade est US corn rating at 73 pct G/E. Corn plantings should be 98 pct done. CN ended today with and outside day closing below Fridays low. CN range was 7.58-7.82. CN ended below both the 20DMA and 50 DMA. Next support is 7.50.

WHEAT

Despite the losses in US futures, Matif wheat managed to stay in the green to start the week although it closed well off the early highs. Heat and dryness across Spain, France and Germany this week provided the main focus. There was more talk of Morocco

still trying to buy nearby old crop wheat. The EU put the Ukraine crop at 27.0 mmt vs the Ukraine Ag Min’s 17-20 mmt and the USDA’s 21.5 mmt. The only thing that counts is exports and USDA’s 10 mmt est may be too optimistic. Focus will increasingly turn to

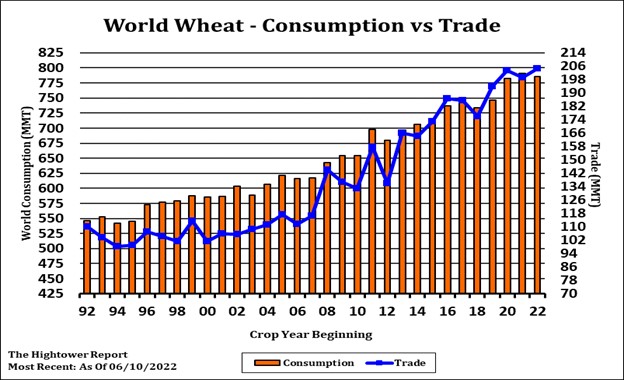

vessel nominations and line-ups in order to gauge Russian exports. India continues to get requests for wheat from various countries but with no reports of any additional sales. USDA’s Jul-June est of 6 mmt as way too high. US weekly wheat exports were near 388 mt. Total exports to date are 615 mt vs 694 ly. USDA goal is 21.1 mmt vs 21.9 ly. Spring crop should be 63 pct G/E. Spring wheat plantings should be 91 pct done. US winter wheat harvest is estimated at 14 pct.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.