Written Commentary

SOYBEANS

Soybeans ended higher. US June CPI data was higher than expected. For some this suggested US Central Bank will increase rates in July and maybe Sep. There is some hope that that could be the highest data for the year. Some feel recent drop in energy and grain prices could suggest US inflation may be peaking. USDA dropped US 2022 soybean crop 135 mil bu due to lower acres. US 2-3 week Midwest forecast is warm and dry. 65-70 pct Midwest has adequate topsoil moisture. US dropped US crush and exports to offset the lower crop. USDA est World 2022/23 soybean crop at 391 mmt vs 352 ly. Is this too high? USDA also est World soybean exports at 169 mmt vs 154 ly. Is this too low? USDA est South America 2023 soybean production at 210 mmt vs 174 this past year. China 2022/23 soybean imports are est at 98 mmt vs 90 this year and 100 last year. Trade est US weekly new crop soybean sales near 100-300 mt vs 240 last week.

CORN

Corn futures ended higher. US cash domestic corn basis remains firm on a slowdown in farmer selling and fact end users are trying to add coverage. US June CPI data was higher than expected. For some this suggested US Central Bank will increase rates in July and maybe Sep. There is some hope that that could be the highest data for the year. Some feel recent drop in energy and grain prices could suggest US inflation may be peaking. USDA increased US 2022 corn crop due to higher acres. US 2-3 week Midwest forecast is warm and dry. 65-70 pct Midwest has adequate topsoil moisture. US dropped US feed use but most feeders report same or higher feed us than last year. The first unanswered question is will UN, Russia and Ukraine agree to a deal that would open a corridor for Ukraine exports. Wire services report some kind of agreement may be signed next week. Still, most doubt Russia will agree without dropping sanctions and Ukraine will not agree unless Russia stops the war. The other unknown is what final US 2022/23 corn supply will look like versus USDA July guess. USDA est World corn imports at 177 mmt vs 179 ly. Is this too low? USDA also est World corn exports at 182 mmt vs 199 ly. Is this too high? US is 61 mmt vs 62 this year. Brazil is 47 vs 44 this year. Argentina 41 vs 39 this year. Ukraine is 9 vs 24 ly. USDA est World corn end stocks at 313.0 mmt of which China is 204. Is USDA est of US corn yield at 177 too high? Trade est US weekly new crop corn sales near 100-400 mt vs 111 last week. Last week there were rumors China may have bought US PNW corn for Jan-Feb.

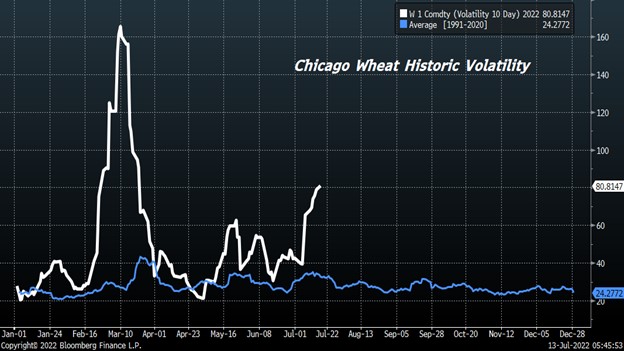

WHEAT

Wheat futures ended lower. US June CPI inflation date was higher than expected. Given recent drop in energy and grain futures some hope this may be the top for inflation. USDA est World 2022/23 wheat imports at 202 mmt vs 196 ly. Is this too low? USDA also est World wheat exports at 205 mmt vs 200 ly. Is this too high? US is 22 mmt vs 22 last year. Russia is 40 vs 33 last year. EU is 35 vs 29 last year. Ukraine is 10 vs 18 ly. Is USDA est of EU wheat crop at 134 mmt too high? The first unanswered question is will UN, Russia and Ukraine agree to a deal that would open a corridor for Ukraine exports. US HRW harvest is wrapping up in KS,OK and TX. Fears of global economic recession continue to offer resistance to wheat prices. Recent decline in US prices makes US exports more competitive. Tight US corn stocks until new crop harvest this fall could see more wheat feeding. Baker remains active component pricing futuresin lower futures trend. Active new crop HRW selling has pressured nearby basis. Logistical challenges still forecasted for balance of Q4 which likely limits downside basis pressure Baker est to be 30-35% covered Q4 and 5-10% covered Q1 2023 and continues to look to add coverage on dips.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.