Written Commentary

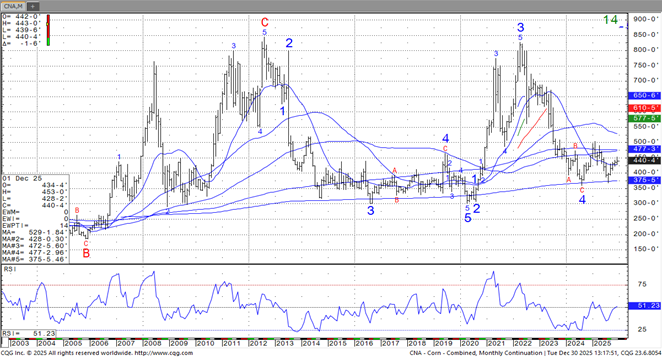

A late rally enabled prices to close fractionally higher. Spreads were little changed. Inside trade for Mch-25 after rejecting trade above $4.60 yesterday for the first time in 6 months. Next resistance is $4.68. Near term forecasts for hot/dry conditions from Central Argentina into S. Brazil provide underlying support while prospects for record soybean yields in Central growing regions of Brazil limit upside opportunities. Last week MM’s bought nearly 68k contracts of corn extending their long position to a 2 year high at 229k contracts. Nov-24 exports at 185 mil. bu. were nearly 30 mil. bu. above the weekly inspections data. Exports in Q1 of the 24/25 MY have reached 513 mil. bu., up 36.5% from YA, vs. the USDA forecast of up 8%. Today’s census data makes me rethink my expectation of no change to the current USDA export forecast of 2.475 bil. bu. in Friday’s WASDE report. The USDA also announced the sale of 110k mt (4.3 mil. bu.) of corn to Colombia. Ethanol exports in Nov-24 at 188 mil. gallons was a 7 month high and up 31% from Oct-24 while up 63% from Nov-23. Tomorrow’s EIA report is expected to show ethanol production last week ranged between 323 – 328 mil. gallons, vs. 327 mil. the previous week. EU imports for the 24/25 as of Jan.5th had reached 10.2 mmt, up 5% from YA.

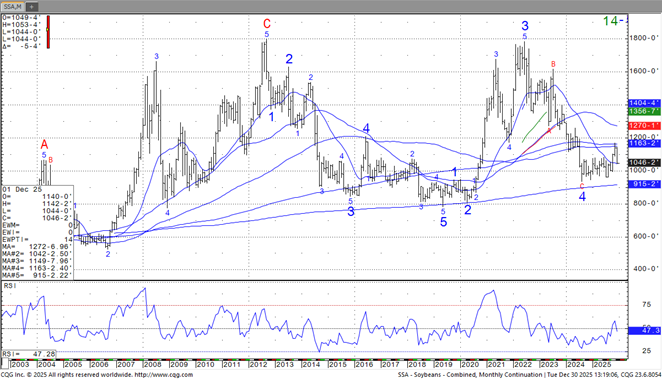

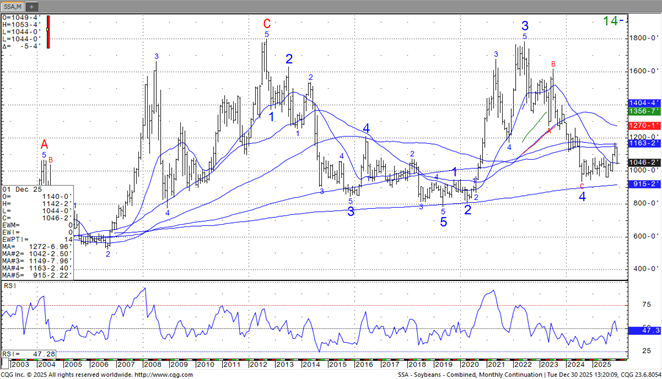

Prices were mixed today with beans steady to $.02 lower, meal was down $3-$4 while oil broke out to the upside finishing 90-100 higher. Mch-25 beans rejected trade below LW’s low rebounding back to near unchanged. Weakening basis levels in Brazil continue to limit upside potential. Beans in Brazil for Mch/April shipment are offered roughly $.10 under CME futures, compared to $.50-$.60 under YA. Extended forecasts offer better prospects for beneficial rains towards the end of week 2 of the outlook, however confidence that far out is sketchy. Mch-25 oil broke out to a fresh 3 week high. Next major resistance not until the 100 day MA at 42.37. After raising their bean oil export 500 mil. lbs. in Dec-24 to 1.10 bil. lbs. look for the USDA to raise this forecast another 300-400 mil. lbs. on Friday. Domestic usage, including usage for biofuels, will likely need to be lowered 200-300 mil. lbs. in order to keep ending stocks above 1.40 bil. lbs. Mch-25 meal held support just above the $300 level and its 50 day MA. Today’s price plunge filled a gap on the chart from the Christmas short covering rally. Last week MM’s bought just over 25k soybeans, 31k meal while selling just over 9k bean oil. Speculative traders remain net short all 3 sectors of the soy complex. Bean exports in Nov-24 at 363 mil. bu. were just over 30 mil. above the weekly inspections data. Cumulative exports in Q1 of the 24/25 MY at 819 mil. bu. are up 15% from YA, vs. the USDA forecast of up 8%. EU soybean imports as of Jan. 5th have reached 6.96 mmt, up 12% from YA. Meal imports at 10.22 mmt, are up 34%.

Prices were $.02-$.03 higher across all 3 classes today. Next major resistance for the Mch-25 contracts are their respective 50 day MA’s. For Chicago it’s at $5.60, $5.61 ¼ for KC and $6.02 ¾ for MGEX. A number states reported updated winter wheat conditions after yesterday’s close with the most notable states showing a decline in ratings. Kansas showed only 47% of the crop was rated G/E, down 8% from late Nov-24, however still above the 43% from YA. Ratings in OK fell 3% to 45% G/E vs. 67% from YA. Conditions also fell in IL, NE, ND, SD, and OH while rising in CO, MT and NC. Look for drought readings to expand across key growing areas of W. KS and the panhandles of OK and TX as these areas have missed out on recent precipitation systems. EU exports for the 24/25 as of Jan.5th have reached 11.16 mmt, down 34% from YA. Wire services are reported that Jordan purchased 60k mt of optional origin milling wheat at $268.90/mt FC for March shipment.

Charts provided by The Hightower Report.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.