Written Commentary

SOYBEANS

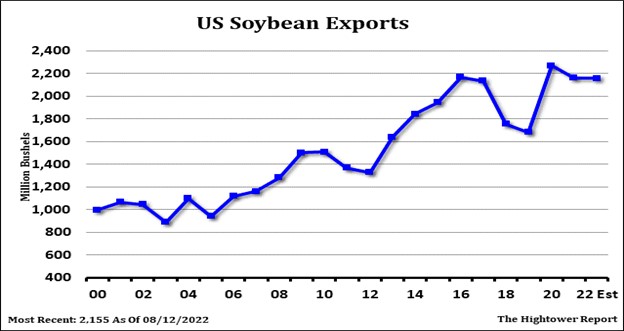

Soybean futures ended lower on talk that US 2022 soybean crop could be record high. Traders are also concerned that Brazil 2023 soybean crop could also be record high. Finally, there is some concern that increase tension between US and China, increase China covid lockdowns and slower China economy could reduce their raw material imports including soybeans from US. Some are about to lower US 2022/23 soybean exports to below 2,000 mil bu which would add 150 mil bu to the carryout. US Q4 and Q123 exports could be huge but could drop off once SA harvest begins. Soyoil gained on soymeal. SA soymeal prices are a discount to US.

CORN

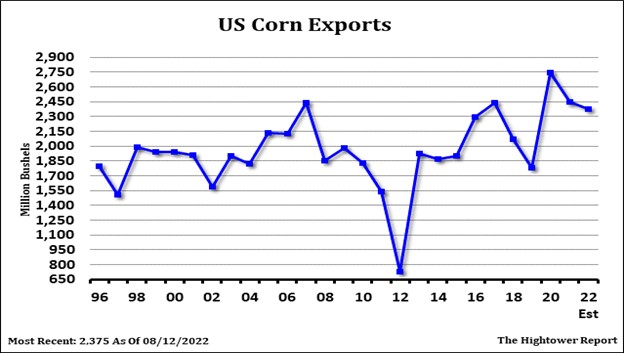

Corn futures ended lower on some long liquidation at month end and talk futures, spreads and cash basis could drop when harvest starts. Ukraine is offering October corn for export near $253 vs US $323. Corn trying to deal with uncertain Ukraine corn exports, actual US 2022 final corn crop, SA 2023 crops and weather, strong cash basis and lower EU corn supply. Could have been some liquidation of short wheat and long corn spreads. There were no Sep corn deliveries. Weekly US ethanol production was down almost 2 pct from last week but still up 7 pct versus last year. Stocks were down 1 pct from last week and 11 pct from last year. Most feel there may not be a weekly USDA FAS export sales report on Thursday. Still trade estimates that old crop sales may have been -100/300 mt and new crop 500-800 mt. Margins are still estimated to be positive. USDA estimates World 2022/23 corn trade near 185.6 mmt vs 200.4 last year. US 60.3 vs 62.2, Brazil 47.0 versus 44.5. Argentina 41.0 vs 39.0 and Ukraine 12.5 vs 24.5. EU exports are est near 2.7 vs 5.8 ly and imports near 19.0 mmt vs 16.0 ly.

WHEAT

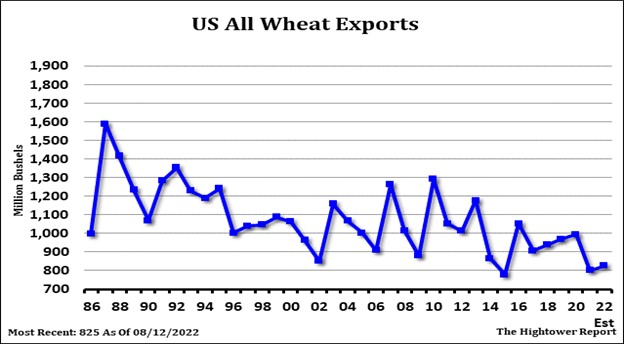

Wheat futures ended higher on unwinding long corn and short wheat spreads. Weak commodity prices on fears of a slowdown of Global raw material demand and stagflation offers resistance. US HRW export prices are $50/60 dollars per tonne over Germany wheat. US SRW export price is $20/25 dollars per tonne over France. Russia wheat export prices are near $310 vs US SRW $346. HRW basis is weaker with more railcars being shown to market ahead of corn and soybean harvest and a few millers sitting idle on sideline ahead of long holiday weekend. NSW harvest progressing nicely and yields continue to impress. Early Canada NWS yields are also better than expected. Wheat futures continue choppy trading with uncertainty on Black Sea exports and fact US exports are still uncompetitive. Rumors that Russia may not extend the Ukraine corridor export deal when it expires in October offered support. US bakers are 99 pct covered Q3, 60-65 pct Q4 covered and 10 pct covered Q1,23.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.