Written Commentary

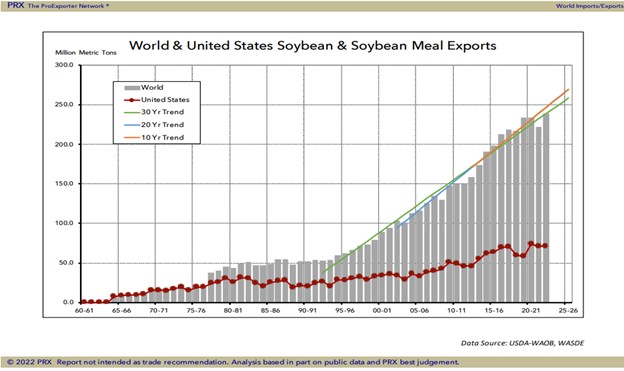

SOYBEANS

Soybean traded sharply lower. Improved US Midwest weather and concern about China demand erased all of last weeks gains. Negative July China economic data weighed on commodity prices especially Crude oil and soybeans. Lower July data forced China Central Bank to lower 2 key interest rates to try to shore up their economy. NOPA

crushed 170.2 mil bu of soybeans in July, up 3 pct from the 164.6 mil bu in June and up 9 pct from July 2021 crush of 155.1 mil bu. The crush had been expected to rise to 171.5 mil bu. Weekly US soybean exports were 27 mil bu vs 10 ly. Season to date exports are 2,031 vs 2,159 ly. Trade est US soybean crop rating at 58 pct G/E vs 59 last week.

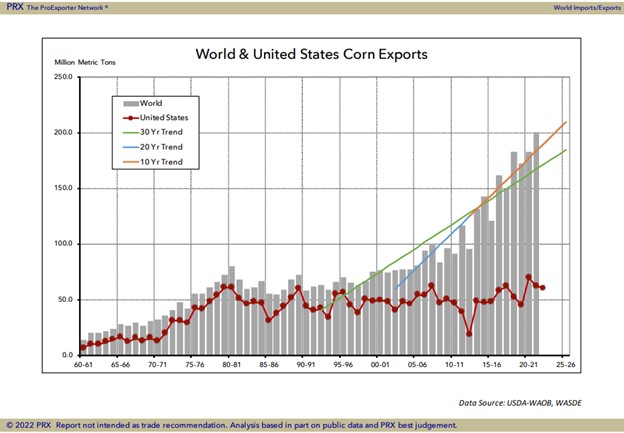

CORN

Corn futures ended lower. CZ ended near 6.27 with a range of 6.18-3.38. Improved US Midwest weather and concern about China demand offered resistance. CZ had An inside day but was unable to push above resistance near 6.40. Some feel CZ could be in a range between 6.00-6.50. Bulls are hoping market could find support near session lows of USDA drops weekly US corn crop ratings again today. Trade estimates US corn 56 pct G/E vs 58 last week. Rains are moving out of E NE into SW IA and NW MO. These areas could see .50-1.50 inches of needed rain. International Research Institute for climate issued a long range forecast suggesting above US Midwest temps through November. South 1/3 US will remain hot and dry. There forecast also includes dry weather for Argentina and S Brazil for the 3rd straight year. USDA drop in World corn production, increase in exports and drop in end stocks offers support to corn futures before South America 2023 harvest. Negative July China economic data weighed on commodity prices especially Crude oil and corn. Lower July data forced China Central Bank to lower 2 key interest rates to try to shore up their economy. Weekly US corn exports were 21 mil bu vs 31 ly. Season to date exports are 2,089 vs 2,547 ly.

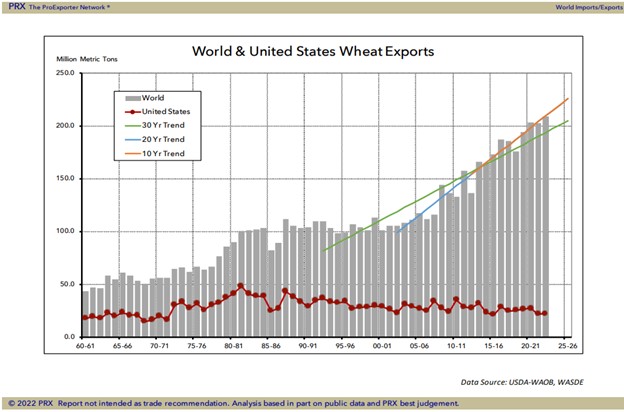

WHEAT

Wheat futures ended lower but off session lows. WU ended near 8.00 with a range of 7.78 to 8.04. WU could be in a 7.50-8.50 range. Talk of higher Russia crop and higher exports offers resistance while hungry World offers support. KWU ended near 8.80 with range 8.58-8.86. MWU ended near 9.10 with range 8.88-9.13. Trade looks for spring wheat rated 63 pct G/E vs 64 last week. 22 pct of the crop is harvested vs 9 last week. Trade estimated US winter wheat harvest at 92 pct vs 86 last week. Most feel grain markets will slowly shift from focusing on supply to demand. USDA raised World wheat exports to 208 mmt vs 205 in July and 202 last year. Still they raised production 8 mmt all in Russia which kept World stocks near 267 mmt vs 276 last year. June to July Russia wheat exports are below last year. USDA estimates Russia wheat exports at 42 mmt vs 33 ly. They also estimate EU at 33.5 vs 31.7 ly. India 6.5 vs 8.0 last year. Weekly US wheat exports were 13 mil bu vs 21 ly. Season to date exports are 142 vs 185 ly.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.