Written Commentary

Source: FutureSource

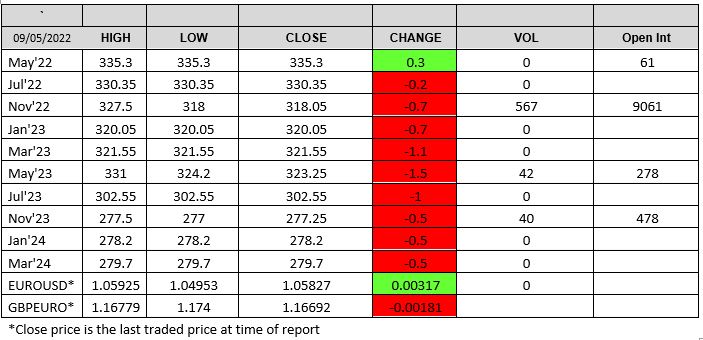

Supply concerns lifted wheat markets to start the day off, both in the US and Europe. Wheat found substantial support due to the trade continuing to put significant focus onto the drier than desired weather pattern in the last couple of months in the EU before pulling back. EU soft wheat maturity is well into a phase where dry conditions will impact overall totals. Forecast going forward is also not very promising. US crop ratings, released later on, are expected to be steady to better with the SRW being the best by far. Canada’s eastern prairies are seeing a similar pattern. Canada’s western prairies continue to be drier than desired. While supplies of wheat have a tendency to end up adequate, it’s tough to count on that right now. Market structure and overbought conditions appear to be the primary negative inputs in wheat futures. Matif Sep-22 hit a trading high of €405/t before pulling back and settling at €394.50/t, down €3.00 on Friday.

US weekly wheat inspections fell by 40% to 236,874tt in the week ending May 5th according to the USDA. No major sales reported. Ukraine exported 1.090Mmt of grain in April according to Agriculture Minister Mykola Solskyi. Vivergo is firing up with first shipments reported to have left the plant last week. Production is set to gradually ramp up towards the end of June according to Vivergo.

Corn and soybeans continued to cool with better planting prospects offering resistance. Demand has been in line with expectations. Potential for heavy spec liquidation may be the biggest potential negative factor near current levels. China’s April bean imports are 8.08 MMT for a year total of 28.36 MMT, which is down .8% from the prior year. China’s y/y edible oil imports are estimated down 65.6% to 1.30 MMT. Safras estimated Brazilian bean production at 122.3 MMT vs. prior 125.08 MMT. They have total corn production at 118.41 MMT with second crop corn at 83.25 MMT or down about 1 MMT from prior estimate.

Malaysian palm oil remains supported. Brent crude was trading down 4.62% at time of writing at $107.27/ba. Matif rapeseed found support with Aug-22 settling €4.50 up on Friday at €846.50/t.

Hanne Bell, Ryan Easterbrook, Dominic Enston and Aaron Stockley-Isted

Phone: +44 (0)20 7716 8477 or +44 (0)20 7716 8140 Email: intl.grains@admisi.com

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice. ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG. A subsidiary of Archer Daniels Midland Company.

© 2022 ADM Investor Services International Limited

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.