The week ends with the Middle East conflict still front and centre, but markets becoming more concerned, or rather less confident that a resolution will be found that reduces the array of medium-term risks to the global economy from the conflict. Some might say ‘not before time’. The fact is that unblocking energy and raw and processed materials supply chains will be a very protracted process, and supply chains will again see substantial re-routing, while establishing alternative scalable and secure sources. Above all, anything that involves processing and refining will take anywhere between 18 months to 5 years, and a great deal of scarce capital and labour resources.

On the regular macro schedule, there are Japan’s National CPI, UK Retail Sales, French Consumer Confidence and Germany’s Ifo Business climate, and only Canada’s less than timely Retail Sales, and US final Michigan Sentiment ahead. With the ECB and the Fed in ‘purdah’ ahead of next week’s policy meetings, there is little in the way of central bank speakers, while Hasbro, HCA Healthcare, Norfolk & Southern, Procter & Gamble and oilfield services giant SLB aka Schlumberger, are likely to be among the highlights of the run of corporate earnings.

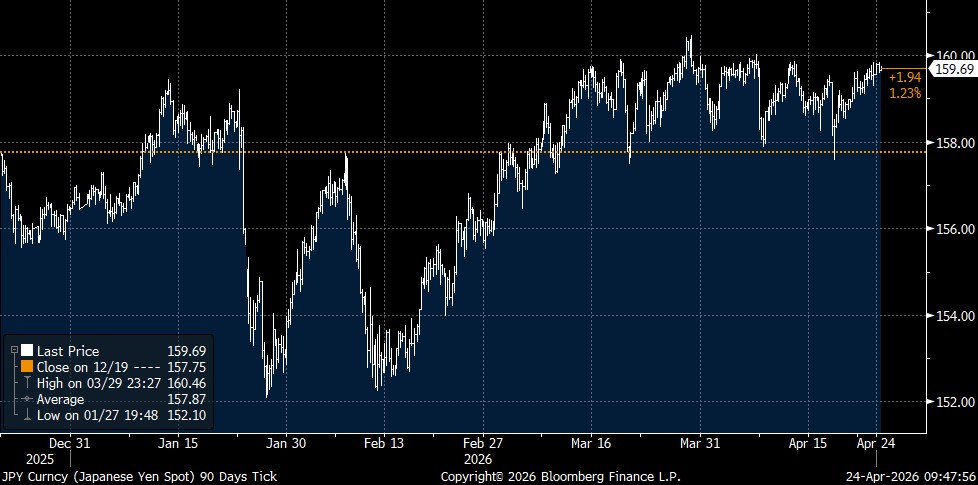

* Japan: While markets are expecting the BoJ to hold rates at next week’s April 27/28 meeting, today’s Japan National CPI was another reminder that it remains behind the curve (as tacitly acknowledge by governor Ueda in his comment that real rates remain low), with the ex-Food & Energy measure slipping marginally to 2.4% y/y, but remaining above the BoJ’s target in every month but one since September 2022. The JPY has been in a very tight 158-160 sideways range since 10 March (see chart), and typically a protracted period of narrow range trading tends to end with a bout of sharp volatility.

* UK: The run of data over the past 2 days has been rather mixed. Today’s Retail Sales at 0.7% m/m was stronger than the expected flat m/m, but this was largely a function of consumers stocking up on petrol/road fuel, with the core ex-Auto Fuel measure at best tepid at 0.2% m/m, particularly given small downward revisions to February. GfK Consumer Confidence at a 3-yr low of -25 vs. prior -21 was in line with forecasts, paced by drops in current and expected views on the Economy. While both PMIs were better than expected, this looks to be a case of companies pre-emptively building up inventories due to supply chain disruption risks, rather than improving demand, as was above all highlighted in the collapse in the CBI Industrial Trends’ quarterly Business Optimism to -65 (below its GFC low, and only just above the low during the pandemic. Overall, it serves as a reminder that the BoE MPC will remain very split about risks to the growth and inflation outlooks.

* Eurozone/Germany: Today’s weaker than expected German Ifo Business Climate (84.4 vs. 86.3) and sharp drop in French Consumer Confidence (84 vs. prior 89) largely echo yesterday’s divergent ‘flash PMIs’, which similarly to the UK saw a boost to Manufacturing from precautionary inventory building, but a sharp drop in Services as consumers reined in spending due to the jump in energy prices. Thus the Ifo fall would have been considerably worse if the marginal drop in the Manufacturing sub-index (-15.5 vs. -14.4) had not offset 6 to 9 point falls in Services, Trade & Construction. While the ECB is focussed on inflation risks, above all second-round effects, it will be wary that already substantial long-term demand destruction from structurally high energy prices may have a more profound impact on the growth outlook.