Written Commentary

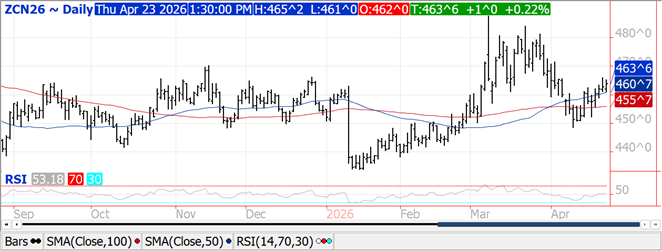

Prices were $.01-$.02 higher in choppy 2-sided trade. Spreads were mixed and little changed. July-26 held support at its 50-day MA while holding near the midpoint of its $4.50-$4.80 range. The BAGE held their production forecast unchanged at 61 mmt, well above the UDSA forecast of 52 mmt. Harvest was reported as only 26.5% complete. US lawmakers continue to make a push for the year-round sale of E-15. While the pace of US planting will be slower than normal in the last week of April, they will likely remain above their historical average. Export sales at 69 mil. bu. was in line with expectations and brought old crop commitments to 2.917 bil. bu. up 28% from YA, vs. the USDA forecast of up 15.5%. Commitments represent 88% of the USDA forecast, above the historical average of 84%. Noted buyers were Korea – 14 mil., Japan – 13 mil. while Mexico bought 17 mil. bu. of new crop. US corn acres in drought rose 1% to 27%.

Prices were mixed with beans steady to $.05 lower while both meal and oil were little changed. Oil spreads weakened; meal spreads firmed while bean spreads were mixed. After rejecting trade above $12 yesterday, July-26 beans slipped back near the midpoint of its $11.55-$12 range. July-26 oil held support just above $.70 lbs. setting up the late day recovery. Support for July-26 meal is at its 100-day MA at $315. Spot board crush margins rebounded $.04 to $3.33 ½ bu. while bean oil PV held near all-time highs at 52.8%. Energy prices firmed late after Pres. Trump ordered the US Navy to “shoot and kill any boat” laying mines in the Strait of Hormuz, threatening the fragile ceasefire agreement. As the Strait remains mostly closed, peace talks apparently are on hold. Speculative traders turned moderate sellers across the soybean complex yesterday. Look for the CFTC to print another record large long position held by MM’s in soybean oil, and a combined record long position across the complex. The markets attention will start shifting to Pres. Trump’s meeting in Beijing with Chinese leader Xi next month. Without additional Chinese purchases the USDA export forecast will likely be lowered again, which will likely again be offset by higher crush. Bean exports at 13 mil. were in line with expectations. YTD commitments are down 18% from YA in line with the USDA forecast. Sales to China for the 25/26 MY are below US/China Trade War I levels from the first Trump Admin. Shipments to China are up to 10 mmt. Meal sales at 162k tons were below expectations and bring YTD commitments to 14 mmt up 17% YOY vs. the USDA forecast of up 6%. Bean oil sales at 3.3 mil. lbs. bring YTD commitments to 803 mil. lbs. down 62% YOY vs. USDA forecast of down 52%.

Prices surged $.08-$.30 with KC futures leading the way. CGO July-26 jumped out to a 3-week high. KC July-26 reached a 22-month high while MIAX July-26 hit a 9-month high. While much of the nation’s midsection will see moderate to heavy rainfall over the next week, some areas in the SW plains will likely remain arid. Early ideas on US winter wheat production is just below 1.20 bil. bu., a 4-year low and compares to 1.329 bil. YA. For HRW futures (KC) to test the $7.00 level would likely take production falling below 600 mil. bu. vs. 804 mil. The BAGE forecasts Argentine wheat planting will drop 3% in 2026 to 6.5 mil. HA citing higher fertilizer costs weighing on profit margins. With US wheat largely pricing itself out of the global marketplace, exports were only 5 mil. Old crop commitments at 900 mil. bu. are still up 15% from YA, vs. the USDA forecast of up 9%. Not even wire service reports that east coast flour mills bought upwards of 120k mt of milling wheat from Poland, shunning more expensive supplies from the US, could hold wheat prices back due to large scale speculative buying. US winter wheat acres in drought jumped another 2% to 70%.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.