Written Commentary

The Week Ahead – Preview:

The new week brings month end and a busy run of economic data, above all in the US, where labour market reports and PCE deflators top the schedule, along with Consumer Confidence and revised Q2 GDP. There are also China’s NBS PMIs, Manufacturing PMIs worldwide, Eurozone and national CPI readings, while the UK eyes Credit and Mortgage Aggregates, BRC Shop Price Index and Nationwide House Prices. Japan looks to Industrial Production, Retail Sales and Q2 Capital Spending, the latter also features in Australia, while Canada has Q2 & June GDP, and South Korea Trade. There are a good number of Fed and ECB speakers in the wake of Powell and Lagarde’s speeches at Jackson Hole. The former stuck to the familiar high or a little higher for longer, though also emphasizing the lagged effects of policy tightening, while the latter underlined the long-term battle to bring down inflation over weak incoming activity data, but skirted offering any guidance on the September meeting outcome, clearly mindful that building a consensus at that ECB council meeting will be challenging, with the minutes of the August ECB meeting also on tap. Commodity markets have an array of corporate earnings from major China oil, iron and steel, battery metals and solar panel producers to digest, while StatCan issues its monthly crops report. Politically all eyes will be on US Commerce Secretary Raimondo’s four-day visit to China, though the suspicion is that it will be mostly a case of fence-mending rhetoric, while post hoc unilateral action on both sides will likely underline ongoing and heightened tensions. US bank regulators are also due to publish proposals for banks with low levels of balance sheet assets to issue long-term debt to provision for capital losses. The UK bank holiday will thin trading, and next weekend will mark the end of the holiday season with the Labour Day holiday in the US.

While the week-ending US monthly labour data will be a key focal point, it is the overall array of the Consumer Confidence’s Labour Differential (Jobs Plentiful minus Hard to Get), JOLTS Job Openings (seen at 9.45 Mln vs. 9.58 Mln) and Challenger Job Cuts along with Payrolls, Unemployment Rate and Average Hourly Earnings which will inform how much the labour market is or is not loosening. Payrolls are forecast at a slightly lower 168K (vs. 187K) and Private Payrolls seen at 150K (vs. 172K), and follow the provisional downward annual of revision 306K, but on balance, all this really says that is that labour demand is solid, though not as strong as previously thought; it does not to point to any ‘show stoppers’ for the Fed’s fight to bring inflation down. Thursday’s headline and core PCE deflators are seen up 0.25 m/m, thus ticking up slightly to 3.3% and 4.2% y/y from 3.0% and 4.1% and echoing the CPI data. House prices are again expected to post solid m/m gains (CS 0.8% m/m, FHFA 0.6% m/m), while remaining negative in y/y terms due to base effects. Consumer Confidence is seen slipping to 116.2 from 117.0, though rising mortgage rates may weigh along with still elevated gasoline prices. Q2 GDP is expected to be unrevised at 2.4%, though the focus has already turned to Q3, which is seen ticking up towards 3.0% SAAR, even if this is seen as a temporary bump higher, both due to the so-called ‘Barbenheimer’ effect and a pick-up in inventories (which may well be involuntary). Auto Sales end the week, and are forecast to slip to 15.5 Mln SAAR from 15.74 Mln, well below pre-pandemic levels, but still supported by pent-up demand due to low pandemic-era output.

China’s NBS PMIs will be very closely watched, but forecasts assume only modest slips to 49.1 from 49.3 for Manufacturing, and 51.0 from 51.5 for Services, despite the run of downbeat anecdotal evidence, which imparts some downside risk. The fact remains that the array of policy tweak announcements continue to underwhelm financial markets hoping, perhaps forlornly, for some ‘shock and awe’ measures, which the authorities are not minded to provide given a clear desire to restore some order to overleveraged parts of the economy. A brief discussion on the latest round of measures can be found here. Elsewhere, the question will be how other Manufacturing (and the week after Services) PMIs fare relative to the broad weakness seen last week in the Eurozone, UK and US readings.

In the Eurozone, national CPI readings will again be rather disparate, with energy price base effects keeping Spanish HICP at a very low level relative to other countries, but ticking higher on the month to 2.6% y/y from 2.1%, and core likely little changed at 4.5% y/y. By contrast, German HICP is seen up 0.3% m/m, but dipping to 6.4% y/y from 6.5%, with the boost from higher travel/tourism costs (set to fade in September), offset by base effects in housing and food. French HICP has the potential to be the major outlier, with the expected rise to 5.4% y/y from 5.1% looking under-clubbed after the sharp 10% increase in electricity prices and a rise in petrol prices during the month, even if food prices should offer an offset. Italian HICP is seen declining quite sharply to 5.6% y/y from 6.3%, with very noisy base effects in airfares and hotel accommodation and lower household energy prices accounting for much of the drop. The end result of all of this is that Eurozone HICP is forecast to post a rise of 0.4% m/m, but fall in y/y terms to 5.1% from 5.3%, with core CPI also expected to dip to 5.3% from 5.5% y/y, but still looking rather ‘sticky’. German Unemployment is seen edging back up by 10K, to push the Unemployment Rate up to 5.7% from 5.6%, while GfK Consumer Confidence is seen little changed at -24.5, with the slide in other surveys imparting some downside risks.

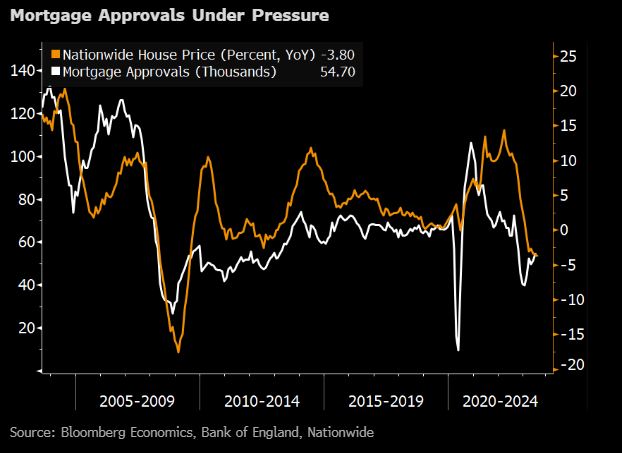

There is some irony that UK data has suddenly taken a fairly sharp turn for the worse after the resilience seen in H1 2023. Given the fall in Kantars’ Grocery price index, there should be a further marked fall in the BRC’s Shop Price Index from July’s 7.6% y/y, paced by food prices. By contrast, housing indicators are expected to remain very weak, with Mortgage Approvals forecast to drop to 51K from 54.7K, Mortgage Lending to remain very weak at £300 Mln and Nationwide’s House Price index to fall -0.4% m/m, to push the y/y rate down to -4.9% from -3.8% (see chart).

Japan’ Industrial Production has been rather choppy in m/m terms, with a drop of -1.3% m/m forecast after a 2.4% m/m jump in June that followed May’s -2.2%, while a boost from tourism is likely to have helped Retail Sales rebound 0.9% m/m after a drop of -0.6%. The Q2 Capital Spending report will as usual dictate the extent of any revisions to the much better than expected Q2 GDP data, with headline CapEx seen slowing to 7.8% from 11.0%, in part due to base effects, with Company Profits expected to edge into negative territory at -0.1% vs. Q1 4.3%, despite an anticipated 4.3% y/y rise in Sales, as higher labour costs start to take their toll. In Australia Q2 Private CapEx is also expected to slow to 1.0% q/q vs. 2.4% in Q1, with Q2 Construction Output also seen slowing to 0.8% q/q from 1.8%, while Canada’s Q2 GDP is expected to slow to just 1.2% SAAR from 3.1% in Q1, and monthly GDP to suggest a significant loss of momentum going into Q3, with a drop of -0.2% m/m after rising 0.3% in May.

Govt bond supply is quite light (as is seasonally typical) outside of the US, which sees $118 Bln total of 2, 5 & 7 -yr, while the Eurozone has EUR 3.0 bln total of 3 & 18-yr from the EU, EUR 5.5 Bln of 4 & 5-yr in Germany, and EUR 5.75 Bln of 2, 3 & 18-yr in Italy.

The Q2 corporate earnings season has largely run its course in North America and Europe, but it will be another busy week for Chinese companies reporting, along with Bank of Nova Scotia, CIBC, HP, Salesforce and UBS. Highlights for the week according to Bloomberg News are likely to include: : Agricultural Bank of China, Bank of China, Bank of Montreal, Bank of Nova Scotia, Beijing-Shanghai High Speed Railway, BOC Hong Kong, Broadcom, BYD, Canadian Imperial Bank of Commerce, China Pacific Insurance Group, China Petroleum & Chemical, China Resources Land, China State Construction Engineering, China Yangtze Power, Citic, Citic Securities, Crowdstrike, Dell Technologies, Dollar General, Fortescue Metals, Foshan Haitian Flavouring & Food, Gree Electric Appliances of Zhuhai, Haier Smart Home, HP, Industrial & Commercial Bank of China, Industrial Bank China, Jiangsu Yanghe Brewery Joint-Stock, LONGi Green Energy Technology, Lululemon Athletica, Luxshare Precision Industry, Luzhou Laojiao, Midea Group, MongoDB, Nongfu Spring, PDD Holdings, People’s Insurance Group of China, Pernod Ricard, PetroChina, Ping An Insurance, Postal Savings Bank of China, Prudential, Salesforce, SF Holding, Shanghai Pudong Development Bank, Shenzhen Mindray Bio-Medical Electronics, UBS Group, Veeva Systems, VMware, Xiaomi.