Written Commentary

{kind=link}

The Week Ahead – Preview:

The new week may be the peak of the summer holiday season in Europe, but has a deluge of statistics from the US and China, which will include Retail Sales, Industrial Production and housing data, and another busy week for the UK with CPI, labour data and Retail Sales, and indeed Canada (CPI, Retail and Manufacturing Sales, and Teranet House Prices), with Japan Q2 prov. GDP and Private Machinery Orders also on tap. It will be seasonally quite light in terms of central bank speakers, though there will be July FOMC and August RBA meeting minutes, while US corporate earnings are dominated by retailers: Walmart, Home Depot, Kohl’s, Lowe’s, Tapestry, Target and TJX inter alia, with Agilent Technologies, Analog Devices, Cisco and Deere & Co also reporting. The week will get off to a rather slow start, with Assumption in many Catholic/Orthodox countries and other bank holidays around the world.

The summer market mood is very much risk on, emboldened by the lower than expected, but still very high US inflation statistics, while swotting away the persistent push back on current market rate trajectories by all Fed speakers, a mixed earnings season, geopolitical tensions and protectionist narratives, the energy crisis in the EU and the UK, and ignoring the implications of a tentative bounce in energy and commodity prices on inflation, or indeed that central bank balance sheet reductions (i.e. liquidity withdrawals) are only just starting to crank up to full speed. Complacency is probably a better description than euphoria, and there appears to be an element of credit spread tightening feeding the equity market rally, above all the 150 bps tightening in US HY Credit spreads from their recent peak (see chart). The latter is however primarily a function of the spectacular swing in free cashflow in the once heavily US Shale oil sector being used to pay down debt, and only modestly to increase upstream oil and gas investment from rock bottom levels. This all attests to the point that not only have developed world central banks been ‘behind the curve’ on raising rates, but also in reducing excess QE liquidity.

Be that as it may, the week kicks off with a raft of statistics in Asia. Japan’s provisional Q2 GDP is seen bouncing back 0.7% q/q (2.6% SAAR), led by a 1.3% q/q rise in Private Consumption and 0.9% q/q in Business CapEx, with a light 0.3 ppt drag from inventories, and flat contribution from Exports. But the focus will be on China’s raft of activity and property data, which are expected to pick up, but hardly to attest to a rebound gathering momentum. Retail Sales are seen up 4.9% y/y from 3.1% y/y in June, but flattered by base effects, with y.t.d. growth expected at 0.1% from -0.7%. Industrial Production is forecast to pick up modestly to 4.3% y/y from 3.9%, while regional govt spending on infrastructure projects, which central govt has demanded should be set in motion by August, should boost Fixed Asset Investment marginally to 6.2% y.t.d. from 6.1%. However the property sector remains a major drag on activity, with New Home Prices expected to be down 0.1% m/m, and Property Investment seen dropping even faster at -5.7% (vs. -5.4%), while Unemployment remains elevated at an unchanged 5.5%. China also conducts its month 1-yr MTLF operation on Monday, with no change expected in the rate at 2.85%, but some speculation that there may not be a full rollover of the CNY 600 Bln that is maturing as the consensus expects, and perhaps a reduction to CNY 400 Bln as the PBOC tries to tamp down on unwanted speculative flows.

In the US, Retail Sales are forecast to edge up by 0.1% m/m, with the fall in gasoline prices (-7.7% m/m) weighing heavily on the headline, with the ex-Autos & Gas measure seen at 0.3% m/m and the core ‘Control Group’ measure up 0.6% m/m, boosted by online sales thanks to the mid-month Amazon Prime Day promotion, and given that discounting in furniture and electronics may boost volumes but not values, this may be a rather better report in ‘real’ terms than for some months. After a weak June print (-0.2% m/m), Industrial Production is expected to recover modestly by 0.3% m/m, though the risks look to be firmly skewed to the upside, given a combination of higher utilities output due to hot weather, a beneficial seasonal adjustment for auto output due to retooling being less of a pronounced drag, and a strong contribution from mining (above all oil output). The first of regional Fed manufacturing surveys are expected to see a downtick in NY to +5.0 after a sharp bounce in July, and a modest recovery in Philadelphia to -5.0, but as ever details will matter more than headline levels, above all Orders (new & backlogs), Outlooks, Prices, inventories and supplier deliveries. Housing data will be the other focal point, with little respite expected after a number of months of sharp deteriorations: NAHB seen unchanged at 55.0, but Housing Starts(-1.9% m/m), Permits (-2.7% m/m) and Existing Home Sales (-4.5% m/m after June -5.4%) all falling further, as the fall in mortgage rates does little to offset affordability and cost of living pressures. Within Existing Home Sales a close eye will need to be kept on volume of supply, still quite low at 3.0 months in June, but trending higher, though not as acutely as New Home supply, which is at levels not seen since 2006/2007 sub-prime crisis.

Over in the UK, labour data get the week under way, with HMRC Payrolls seen up a modest 25K in July, while Q2 LFS Employment is expected to have posted a very robust 273K gain, only marginally less than the March-May 296K, and the Unemployment Rate seen steady at 3.8%, just above its all-time low of 3.7%. But it will be Average Weekly Earnings that attract most attention, with base effects accounting for the forecast drop in headline to 4.6% y/y from 6.2%, and more importantly some upward creep expected in the ex-Bonus measure to 4.5% y/y from 4.3%. But the latter will still be heavily negative in real terms, as the CPI data on Wednesday are expected to confirm with a 0.4% m/m rise pushing the y/y rate up to 8.6% from 8.2%, and core to 6.0% y/y from 5.8%, and as is well documented expected to keep on climbing to a peak of 13.3% y/y in October, according to BoE forecasts. Pipeline pressures are expected to remain high with PPI Input seen up 0.7% m/m 23.8% y/y and Output 0.9% m/m 16.5% y/y. The week ends with Retail Sales expected to drop -0.2% m/m, the seventh fall in 9 months, which have only seen one gain of just 0.1%, with the ex-Auto Fuel seen at -0.3% m/m, while July PSNB data are expected to see a deficit of £-2.8 Bln, in a month which normally sees a surplus due to hefty corporation tax receipts.

Elsewhere, Australian Unemployment is seen steady at all-time low of 3.5%, with Employment growing a more modest 26.5K, while Q2 Wages are forecast to rise a little faster in q/q terms (0.8% vs. 0.7%) and pick up to a still very subdued 2.7% y/y from 2.4%. Canada’s headline CPI is expected to echo the US and fall to 7.6% from 8.1% thanks to falling gasoline prices, core measures are however seen little changed at an average 5.0% y/y, per se implying that while the BoC may not opt for quite such an aggressive hike in September, it will remain hawkish, though this week’s Teranet House Prices will likely underline the very negative impact those aggressive rates are having. Germany’s ZEW Expectations survey should see a more marked improvement than the expected marginal gain from -53.8 to -52.7, given that the Dax has had a strong rally since early July, while the Current Situation is seen dropping further to a new low of -48.0 from -45.8, hardly surprising given the array of energy crisis inputs and chaos in Rhine transport due to low water levels. Last but not least, various CEE countries publish Q2 GDP data, which will show the extent of the impact of the war in Ukraine, energy crisis and very sharp interest rate increases in recent months, with forecasts looking for a -0.7% q/q for Poland and -0.2% q/q for Romania, and by contrast a +0.5% q/q for Hungary; Bulgaria and Slovakia also report.

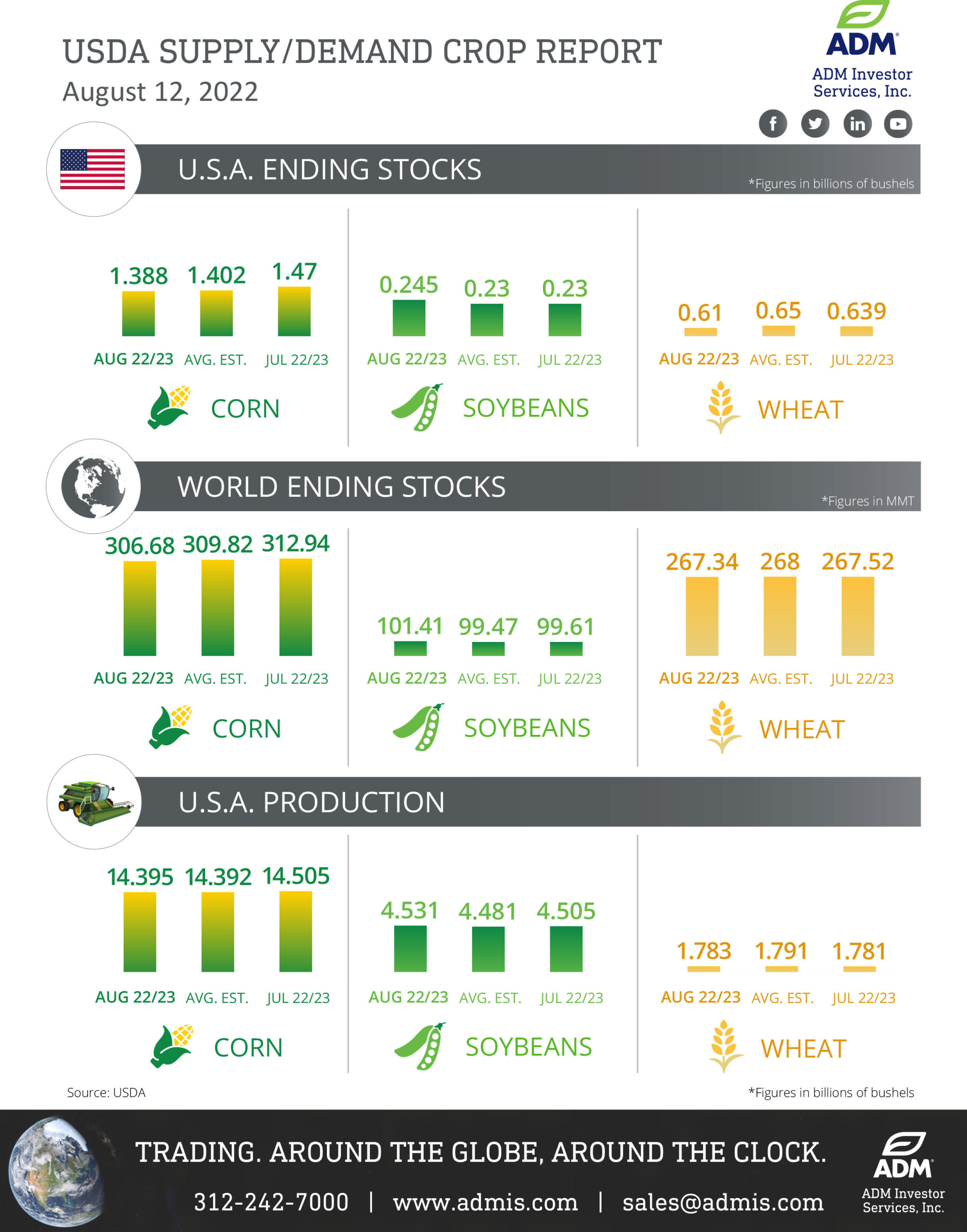

In the commodities space, it will still be a case of numerous supply concerns contending with rapid swings in sentiment about the economic outlook, and by extension demand. Last Friday’s WADSE was mixed, see summary infographic and watch ADMIS’s Steve Freed’s assessment here . As noted above, Rhine Water levels are now so low that barge transport is reduced to a minimum and may have to stop completely, with barge rates up in the sky, and thus creating huge problems for diesel and coal transport, which is in part being switched to rail. There are Saudi Aramco’s record Q2 profits to digest, with the company pledging to raise output to maximum levels, while Monday sees the focus switch to miners with behemoth BHP results, and above all its outlook for demand, given concerns about demand in China and the EU. Results and outlook expectations from Deere & Co will also be watched closely as a proxy for the global economic outlook.

As noted Retailers dominate the US earnings run, with the focus on how Walmart are dealing with rising input costs (goods and wages) and reducing an involuntary build-up of inventories. The earnings schedule also has a busy run of Chinese corporates reporting, and is likely to see the following among the highlights according to Bloomberg news: Adyen, Agilent Technologies, Analog Devices, Applied Materials, Bath and Body Works, BHP Group, China Merchants Bank, China Telecom, Cisco Systems, CSL, Deere, Estee Lauder, Galaxy Entertainment Group, Goodman Group, Henkel, Hong Kong Exchanges & Clearing, Jiangsu Hengrui Medicine, Keysight Technologies, Kohl’s, Li Auto, Macy’s, NetEase, Ping An Bank, Ross Stores, Saudi Arabian Oil, Sea, Shenzhen Mindray Bio-Medical Electronics, Synopsys, Tencent, TJX, Tongwei, Transurban Group, Wuxi Biologics Cayman, Xiaomi, Yunnan Energy New Material, Zhangzhou Pientzehuang Pharmaceutical.

The information within this publication has been compiled for general purposes only. Although every attempt has been made to ensure the accuracy of the information, ADM Investor Services International Limited (ADMISI) assumes no responsibility for any errors or omissions and will not update it. The views in this publication reflect solely those of the authors and not necessarily those of ADMISI or its affiliated institutions. This publication and information herein should not be considered investment advice nor an offer to sell or an invitation to invest in any products mentioned by ADMISI.

© 2022 ADM Investor Services International Limited.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.