Written Commentary

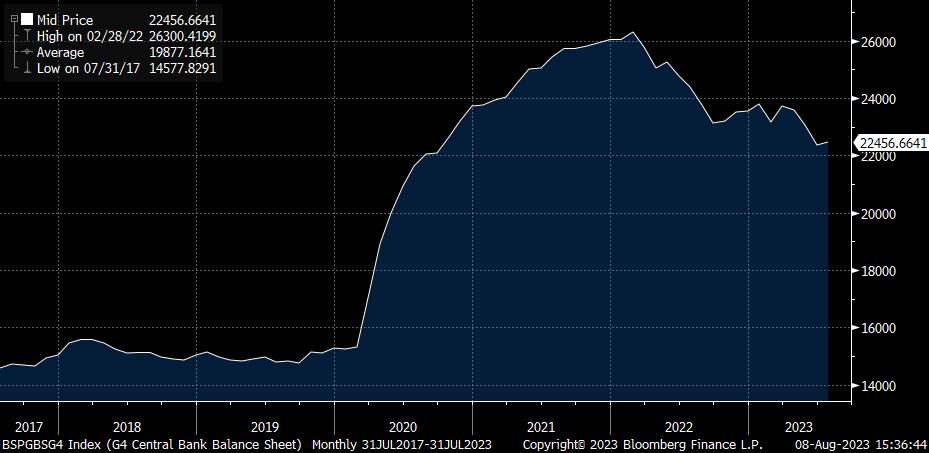

Markets are once again navel gazing, rather than really paying much attention to economic data. The run of events which started with the BoJ YCC policy tweak (how long before these ‘tweaks’ is recategorized as active policy tightening, rather than this myopic ‘nothing but blue skies’ euphemism), and was followed by the Fitch US sovereign downgrade, Moody’s US Bank downgrade and Italy’s bank levy, appears to finally be shaking confidence, along with the belated recognition that the G7 central ‘high for longer’ message is not a bluff. Ironically it comes at the same time as the aggregate size of G4 (Fed, ECB, BoJ & PBoC) central bank balance sheets has finally broken down through the September 2022 low point – see chart, though overall the pool of excess liquidity remains large at $22.6 Trln, but 15% lower than February 2022’s peak.

Be that as it may, the day’s schedule is modest, amounting to digesting China’s lurch into deflation, and awaiting Mexico’s CPI; with no central bank speakers scheduled. Another busy day for corporate earnings features amongst others: NTT, Sony, CBA and QBE in Asia, E.On and Generali in Europe, while Walt Disney will be the headliner in the US. There are 10-yr govt bond auctions in the UK, Germany and the USA.

** China – July CPI and PPI **

CPI fell marginally less than expected at -0.3% y/y, but was up 0.2% m/m, posting a gain for the first time in six months, and Core CPI rebounded to 0.8% y/y from 0.4%. The details highlight once again the hefty influence of food price base effects, which slid 1.7% y/y having been up 2.4% in June, which in turn underlines that the headline fall is deceptive, and will not last as base effects turn positive in coming months. The latter was evident in non-food prices which turned flat y/y after posting a drop of -0.6% y/y in June notably offsetting that food price fall was a sharp pick-up in holiday travel costs from 6.4% to 13.1% y/y, offering a glimmer of hope that consumer demand in this sector is proving to be robust. On the other hand, PPI remains mired in negative territory falling -0.2% m/m, with base effects in commodities and raw materials pushing up the y/y rate to -4.4% vs. expected -4.1% and June’s -5.4%, but still sending a weak signal on domestic demand and output, with the latest round of stimulus measures only likely to exercise modest upward pressure in H2 2023, assisted by the weakness in the CNY exchange rate.