Written Commentary

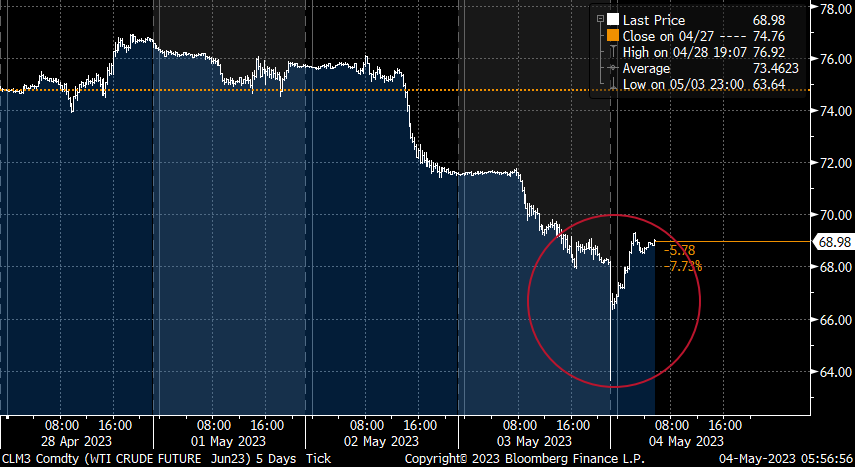

Yesterday was all about the Fed policy meeting, today is all about the ECB, with China’s Manufacturing PMI (dropping more than expected to 49.5) and German Trade (exports and imports falling more than expected, and suggesting February’s bounce was nothing more than an outlier) to digest ahead of Eurozone & UK Services PMIs, UK Consumer Credit and Mortgage Lending, US Q1 Non-farm Productivity, weekly Jobless Claims and Trade, the latter also due in Canada. Outside of the ECB, Norges Bank is expected to hike rates a further 25 bps to 3.25%, while there are local elections across England, but not London, in the UK, with the ruling Conservatives seen potentially losing up to 1,000 of their 3,663 seats that are being contested, with the elections taking place largely in rural areas, and a few Northern urban areas. Apple will be the focal point of today’s US Q1 corporate earnings, with the likes of AIG, Coinbase Global, Expedia and Sempra Energy also reporting. France and Spain hold multi-maturity govt bond auctions. Oil prices remain enormous pressure from a gloomy global economic outlook, the slide below $70 on WTI (with a very chaotic opening in Asia this morning – see chart) and $75 on Brent begs the question about how much more damage this will do to already subdued upstream investment intentions (outside of NOCs in the Middle East and Asia).

In terms of the Fed ‘pause’ signal, it was about as tentative as the FOMC and Powell could make it, with the phrase ‘some additional policy firming may be appropriate’ replaced by ‘In determining the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments’. Nevertheless, markets are pricing no rate moves in June or July, but already discounting a cut in September, which was clearly not the message that Powell & Co were conveying.

** UK/EU – April Services PMIs **

Flash readings for the UK and Eurozone were a lot stronger than expected, and it will be interesting to see if there are any upward revisions, given that much of the improvement appears to be centred around tourism, and lower energy prices. The fact that winter appears to be very unwilling to leave the stage this year across much of Northern and central Europe could perhaps act as a dampening factor. As with yesterday’s US Services ISM, a close eye needs to be kept on Prices Paid indices, which have fallen quite sharply, but remain elevated on any ‘normal’ historical comparison.

** U.K. – March Consumer Credit/ Mortgage Lending **

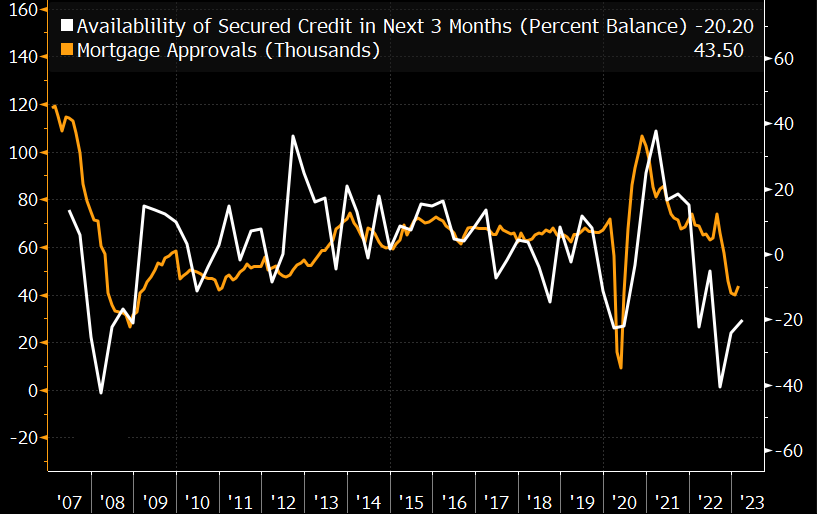

While Consumer Credit has returned to a broadly normal pace, and is expected to ease modestly to £1.2 Bln from February’s £1.4 Bln, which would leave the y/y pace running close to March’s 7.7%, even if the primary implication remains that households continue to borrow to pay bills boosted by inflation. But the focus will remain on Mortgage Lending and Approvals, which have improved since the Truss budget debacle, but remain way below ‘normal’ levels – see chart. Secured Lending is seen recovering to £1.6 Bln following a monthly cyclical low of £738 Mln in February, and a long term average £4.07 Bln.

** Eurozone – ECB council meeting **

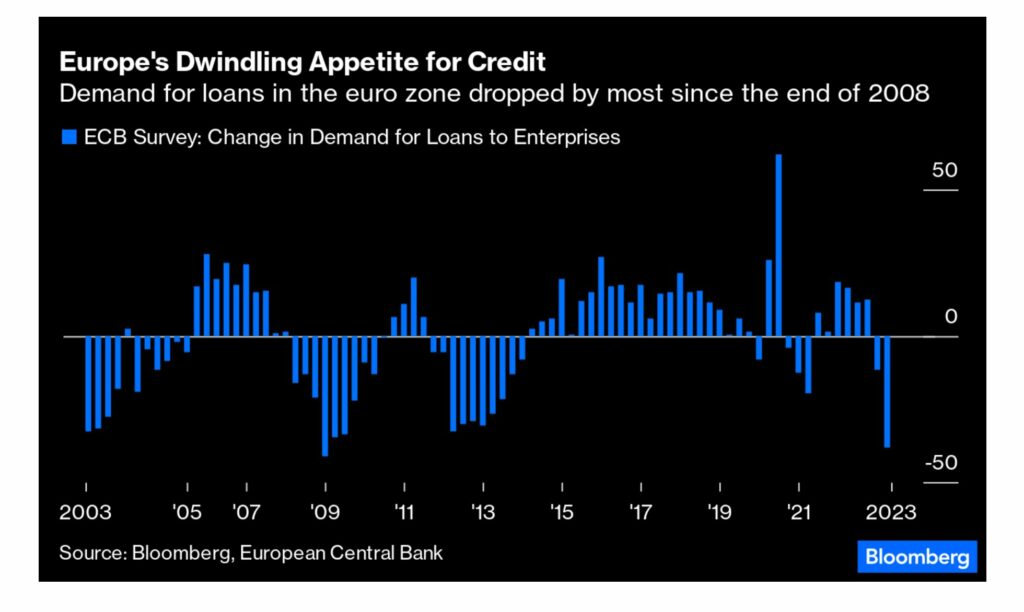

While inflation has definitely peaked in headline terms (April 7.0% y/y), and probably on core (April 5.6%), both remain very high, and the drop in core will likely be very slow and protracted, leaving the ECB with no choice other than to hike today by the expected 25 bps, and more likely again in June and July. While there had been some speculation about a further 50 bps hike today, Friday’s tepid 0.1% q/q Q1 GDP, and the steep fall in corporate credit demand seen in Tuesday’s quarterly ECB Lending survey (see chart) will be more than ammunition to temper the demands of the hardcore hawks on the ECB council. The ‘data dependency’ ‘meeting by meeting’ mantras (in principle a cloaking device for the rather deep divisions between hawks and doves) will likely be recycled. The question is whether there are stronger hints about a peak being closer at hand, and whether the hawks succeed in arguing for a faster pace of QT, as many have argued for. The press conference will likely also see some questions about the impact of a stronger EUR on the policy outlook, and it will be interesting to see if Lagarde’s recent Peterson Institute speech about the risks to Europe from global decoupling, and the attendant need to strengthen pooling of resources within the EU to strengthen supply chain security (above all energy and raw materials) gets any ‘air time’.