Written Commentary

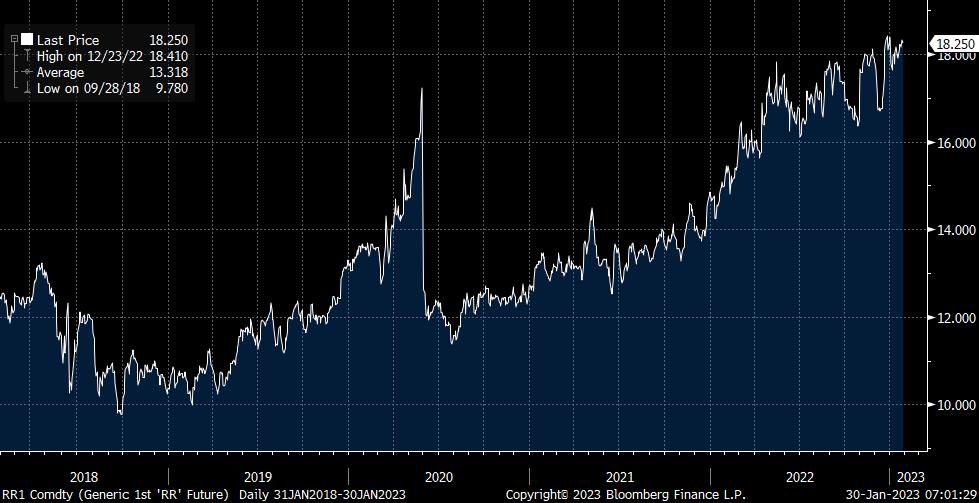

The week gets off to a relatively quiet start in data and events terms, with the improving UK Lloyds Business Barometer, fuelled by a welcome rise in optimism rather than activity, along with very weak Swedish GDP and the unexpected rebound in Spanish CPI (above all core at 7.5% y/y from 7.0%) to digest, which if echoed elsewhere will jangle market nerves ahead of the ECB meeting, with only German Q4 GDP and the US Dallas Fed Manufacturing ahead in terms of statistics. BPs annual World Energy Outlook tops a modest schedule of events, and while there are a good number of corporate earnings reports and the EU will sell 5 & 9-yr debt, the focus will be largely on month end, as markets await the large array of risk events later in the week. German GDP is seen flat q/q, which is an extrapolation from the already published 2022 estimate, and per se, any miss would be due to revisions to prior quarters; again this falls into the category ‘better than expected, but still weak’. With the UN FAO Food Price Index due at the end of the week, and most people focussed on wheat, corn, soybeans and livestock prices in terms of forward signals on food price pressures, it should be remembered that Rice is in fact the core staple food item globally, and it is now trading above the pandemic spike level in what is an ominous signal which requires monitoring – see attached chart.

RECAP: The Week Ahead – Preview:

This will be a bumper week for data and events on pretty much all fronts, with the Fed, ECB and BoE likely to be front and centre, as markets have continued to push hard against the Fed and ECB rates rhetoric. Statistically Euro area and national Q4 GDP and CPI readings, China’s NBS PMIs and the US Employment Cost Index and Consumer Confidence dominate the start of the week, along with month end. The back end of the week has Manufacturing and Services PMIs, South Korea Trade ahead of the US January labour data. In event terms the week kicks off with the IMF’s World Economic Forecast update on Tuesday, with interest in how it contrasts with the downbeat World Bank assessment, India presents its 2023 Budget in a year packed with 9 state elections ahead of the 2024 General Election, there are also rate decisions in Brazil & Czechia (both no change), along with embattled Ghana (200 bps rate hike) and Kenya (25 bps hike), and a close eye will continue to be kept on the war in Ukraine as Russia threatens a new offensive. In the commodities arena, OPEC+ holds Joint Technical Committee and Ministerial meetings, BP publishes its annual Energy Outlook, Exxon Mobil and Shell top a long list of oil sector companies reporting Q4 earnings, there are Q4 Production reports from Anglo American, Glencore and Vale, and earnings from Caterpillar and US Steel will also attract plenty of attention. The UN FAO publishes its Food Price Index as well as its Cereal Supply and Demand Briefing, and the USDA semi-annual report on Cattle Inventories will be very closely watched, with a relatively sharp fall expected on the back of high feed prices and drought hit pastures. US tech behemoths Alphabet, Amazon, Apple and Meta Platforms top the busy run of earnings in the US and elsewhere. There are no coupon sales in the US this week, but a busy week in Europe has govt bond auctions from the UK, EU, Germany, France, Italy and Spain, while Japan sells 2 and 10-yr, and there will also be a deluge of local govt bond issuance in China, as it returns from the Lunar New Year holidays. Politically the meeting between Biden and House speaker McCarthy on Wednesday about the US debt ceiling will be closely watched, while the sacking of Zahawi as UK Conservative party chairman and the poor reception for last Friday’s empty handed speech by Chancellor Hunt on kick starting the UK economy serve as a reminder of the fragility of the UK government, and there will be a fresh set of strikes in France on Tuesday against Macron’s renewed efforts to reform the French pension system.

For all that the data run is busy, it will be secondary to the run of central bank meetings. The Fed is expected to dial down its rate hike pace for a second meeting, with a 25 bps hike to 4.50%-4.75% expected, and markets pricing in just one further 25 bps hike at the March meeting. While there has been the usual rotation of regional Fed president voters, which at the margin can be seen as a potentially dovish shift, the fact is that Kashkari has swung from being arch dove to arch hawk, Boston Fed’s Logan has been vocal in opposing markets easing of financial conditions, as has Harker. While voting was unanimous for most of last year, there is a good chance that one or other member may dissent and vote for 50 bps, above all to signal discontent with market rate pricing, and Powell will probably be happy about this in signal terms. In terms of narrative on the economy and inflation, they will acknowledge the loss of growth momentum, and the slowdown in inflation indicators, but Tuesday’s Q4 Employment Cost Index (expectation 1.1% q/q vs. 1.2%) may be referenced along with Friday’s unchanged Core Services ex-Housing PCE deflator as part of an emphasis on needing to keep rates restrictive for a protracted period. Particular attention will be paid to any tweaks to the statement outlook on rates, which in December said: “The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” It will also be interesting to see if Powell echoes Brainard, Waller and Bullard in suggesting prospects for engineering a ‘soft landing’ for the economy have improved, as well as any comments on the impact of China’s re-opening on the inflation outlook. Powell will certainly be wary of not fuelling market hopes for a Fed pivot, though as rates get closer to a peak, the path in signalling terms becomes ever narrower, and more challenging.

By contrast to the Fed, the ECB has been emphatic about ‘staying the course’ on hiking rates, though markets while discounting a further 50 bps rate hike this week (Depo 2.50%, Refi 3.0%), are veering towards a 25 bps rate hike in March, despite all but a few doves signalling 50 bps at both meetings. The week’s CPI and GDP readings could well shift market expectations in either direction, with 0.2 ppt fall in headline CPI to 9.0% y/y and just 0.1 ppt in core to 5.1% expected (with ‘core core’ having climbed close to 7.0% y/y in December,) while Eurozone Q4 GDP is seen falling 0.1% q/q, though the risk is modestly to the upside on the latter, given that both German and French readings are seen flat q/q, and Spain marginally beat forecasts at 0.2% q/q, with Italy seen contracting 0.2%. A close eye will need to be kept on how much of a positive contribution is made by inventories, given that any build would be seen as involuntary due to weak demand, though Lagarde may well suggest that the growth outlook has improved, and what is said on wages which are clearly becoming more of a concern (even the very dovish Panetta has conceded that a wage price spiral must be prevented, as well as the view on energy price falls. Should the statement see little change to this section “In particular, the Governing Council judges that interest rates will still have to rise significantly at a steady pace to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target”, this would underline their hawkish narrative, especially if they were to add ‘at the next several meetings’. The other focal point will be on the impending start of balance sheet reduction (QT), and on any further details on timing and implementation, and above all on any discussion about how this might interact in policy implementation terms with rate policy, i.e. the extent to which QT might mitigate some of the upside pressure on rates. The risks are very much skewed to markets being unpleasantly surprised by ECB hawkishness.

The BoE is seen as having little choice in having to hike rates by 50 bps to 4.0% following the only gradual drop in headline CPI and stubborn core inflation, as well as the uptick in Average Weekly Earnings (even if, as previously noted, adverse base effects are clearly playing a role). But the key questions are on a) the voting after Dhingra and Tenreyro voted for no change in December, while Mann voted for +75 bps, and b) the extent to which GDP forecasts are revised higher, as well as longer term CPI forecasts, given that market rate expectations have been wound back quite sharply since November’s Monetary Policy report. It will also be interesting to see if Hunt’s tight fiscal policy stance is seen as mitigating the need for an aggressive rate policy. It is possible that the already quite ambiguous signal on future rate moves becomes even more vague, though an outright pause signal would probably have to be couched in terms which emphasize that the risk would still be for higher rates if needed, and not opening the door to ‘pivot’ chatter.

In terms of the week’s US data, Consumer Confidence is expected to tick marginally higher, Challenger Layoffs are likely to escalate sharply higher, JOLTS Job Openings are seen falling modestly to a still very high 10.3 Mln, and Auto Sales are expected to jump very sharply to 15.5 Mln though largely due to seasonal adjustment. Friday’s labour data are forecast to show a drop in Non-farm Payrolls growth to 185K, though markets have generally under-clubbed forecasts for many months in what looks to be a case of ‘wishful seeing’, and a failure to understand that while tech sector layoffs are large, other parts of the economy are still struggling to fill positions. The Unemployment Rate is seen ticking up 0.1 ppt to 3.6%, though the more pertinent question will be whether the Underemployment Rate holds at an all-time low of 6.5%, with the Participation Rate seen unchanged at 62.3%. Elsewhere Japan’s Industrial Production is forecast to fall 1.2% m/m, but Retail Sales are expected to rebound 0.8% m/m, with South Korea’s Trade data perhaps more significant, with the fall in Exports seen accelerating to -11.5% y/y.

As noted it will be a very busy week for earnings in the US (107 S&P 500 companies reporting) and around the world, with Bloomberg News noting the following as being among the highlights: AMD, Aflac, Allstate, Alphabet, Amazon, Amgen, Aon, Apple, Banco Santander, Bristol-Myers Squibb, Canadian Pacific Railway, Cigna, ConocoPhillips, Deutsche Bank, Electronic Arts, Eli Lilly, Estee Lauder, Exxon Mobil, Ferrari, Ford Motor, General Motors, Gilead Sciences, GSK, Hershey, Hitachi, Honeywell International, Humana, ING Groep, LyondellBasell, Marathon Petroleum, McDonald’s, McKesson, Merck, Meta Platforms, MetLife, Mitsubishi, Mitsui, Mizuho Financial Group, Mondelez International, Moody’s, Novartis, Novo Nordisk, NXP Semiconductors, Pfizer, Phillips 66, Qualcomm, Samsung SDI, Sanofi, Shell, SoftBank, Sony, Starbucks, Sumitomo Mitsui Financial, Sysco, T-Mobile US, Takeda Pharmaceutical, Thermo Fisher Scientific, UBS Group, UniCredit, UPS & Zimmer Biomet.