Written Commentary

A bumper day for economic statistics awaits, while the events schedule is rather thin, though there is another deluge of corporate earnings in China. There are Australia’s CPI (falling faster than expected) and Q2 Construction output and Spanish CPI to digest, while ahead lie German CPI, an array of confidence surveys for the Eurozone, Italy and Sweden, UK Consumer Credit and Mortgage Lending, US ADP Employment, revised Q2 GDP, Goods Trade Balance, Wholesale Inventories and Pending Home Sales. BoJ’s Tamura is the sole scheduled central bank speaker and his comments offered some clear hints that further policy tweaks may be ahead, though he may prove to be a minority dissenter against the ‘status quo’, while Banco de Mexico publishes its latest inflation report. Amongst those reporting earnings in China are Bank of China, Baoshan Iron & Steel, Country Garden Holdings, Great Wall Motors, ICBC, PetroChina, Postal Savings Bank, Shaanxi Coal, Tianqi Lithium and Zoomlion, while Crowdstrike and Salesforce headline in the USA. Govt bond supply takes the form of 5 & 10-yr and 7-yr FRN in Italy, and 4-yr in Germany.

** Germany / Spain – August prov. HICP **

Eurozone national CPI readings will again be rather disparate, with energy price base effects keeping Spanish HICP at a very low level relative to other countries, but ticking higher on the month to 2.6% y/y from 2.1%, and core HICP likely to be little changed at 4.5% y/y. By contrast, German HICP is seen up 0.3% m/m, but dipping to 6.4% y/y from 6.5%, with a boost from higher travel/tourism costs (set to fade in September), offset by base effects in both housing and food, however the initial reading from Germany’s most populous state NRW (0.5% m/m) implies higher than expected outturn, with a 0.9% m/m rise in transport, and a 1.5% rise in Alcohol & Tobacco among the pressure points. Today’s reading and the French, Italian and Eurozone readings tomorrow will probably offer fuel to both hawks and doves on the ECB council, with hawks arguing that inflation remains way too high, and it would be premature to suggest that rates are sufficiently restrictive, above all to bring core inflation down to target. Doves will argue that the array of growth indicators are already flashing amber, if not red, and that time needs to be taken to judge the cumulative and lagged impact of what has already been implemented, or severely heighten the risk of over-tightening.

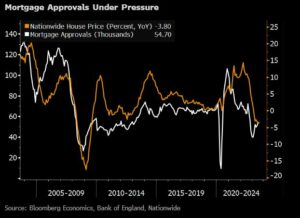

** U.K. – Consumer Credit & Mortgage Approvals **

As noted, this week’s UK housing indicators are expected to remain very weak, with Mortgage Approvals forecast to drop to 51K from 54.7K, Mortgage Lending to remain very weak at £300 Mln and Nationwide’s House Price index to fall -0.4% m/m, to push the y/y rate down to -4.9% from -3.8% (see chart). Consumer Credit is expected to post a very average rise of £1.4 Bln.

** U.S.A. – July ADP Employment / Q2 GDP **

Yesterday’s much sharper-than-expected fall in JOLTS Job Openings (8.827 Mln vs. prior revised 9.165 Mln) and a sharp deceleration in the Consumer Confidence Labour Differential (Jobs Plentiful minus Hard To Get) suggest that the loosening in the US labour market is starting to accelerate in a significant way, even if the ever sharper revisions to both JOLTS and Consumer Confidence do raise questions about data reliability. As has often been the case in the past year, the ADP Employment measure has a habit of delivering a surprise, and often a misleading one, with today’s August report seen decelerating to 192K after posting sharp gains of 324K and 455K in prior months, which stood in contrast to modestly soft gains in the official Payrolls data. 2 GDP is expected to be unrevised at 2.4%, though the focus has already turned to Q3, which is seen ticking up towards 3.0% SAAR, even if this is seen as a temporary bump higher, both due to the so-called ‘Barbenheimer’ effect and a pick-up in inventories (which may well be involuntary).