Written Commentary

The overaching political themes remain a constant source of leftfield disruptors (as per the abrupt termination of US Canada trade talks on the back of the White House taking umbrage of a Canadian video that showed footage of former US President Reagan criticising tariffs, which markets have chose to largely ignore in favour of putting an optimistic spin on Trump and Xi likely meeting at the APEC meeting). But economic data has its first real moment in the sunshine since Monday’s run of China activity indicators, with the focus on the delayed US CPI, run of ‘flash’ PMIs, UK Retail Sales and Japan’s overnight National CPI. The events schedule is sparse with some ECB speak from Nagel and Villeroy, and an expected further 100 bps rate cut in Russia. A busier day for corporate earnings in both Asia and Europe relative to the US has China Shenhua, Gotion Hiugh-Tech, Shandong Iron & Steel, Tongwei, NatWest, Norsk Hydro, HCA Healthcare, Procter & Gamble and Brazil’s Usminas among the likely highlights. As we go into the weekend, markets will also be watching oil prices, after yesterday’s very sharp short covering driven rally on the back of the new US sanctions on Russia’s Lukoil and Rosneft. The question now is whether this will be sufficient to quell long-standing concerns about an overall supply surplus, above all in the context of record volumes of floating storage, and indeed a roll-off period until 21 November before the sanctions take effect. Finally this Sunday beings the mid-term elections in Argentina, with opinion polls suggesting a knife edge outcome between President Milei’s La Libertad Avanza and Peronists, and the US administration adding fuel to the fire by stating that it would cease support for the country if Milei is defeated, with the slump in Argentina’s USD denominated this year not only a function of its debt and currency woes, but also discounting a swing back to the Peronists, leaving the country mired in all too familiar and destabilising political cycle.

** U.K. – Sep Retail Sales / PMIs **

In what has been a much better week for economic news, the run of upside surprises on today’s Retail Sales, Consumer Confidence and PMIs underlines a point that the domestic narrative on the UK economy has been too negative, even if none of today’s data does anything to resolve the UK’s fiscal problems. But then again, the media narrative all to frequently implies that the UK’s fiscal problems are unique, when in fact they should largely be ranked pari passu with the US, Europe or Japan. Be that as it may a jump in the climate for major purchases paced the rebound in Consumer Confidence (17 vs. 20), best in 14 months. Retail Sales at 0.5% m/m followed gains of 0.6% and 0.5% in July, and was paced by strength in Household Goods, Online Sales (helped by promotions) and jewellery, which suggests a very solid contribution to Q3 GDP from Household Consumption, and a greater propensity to spend household savings that have accumulated amid all the political uncertainty (and benefited from higher interest rates – sic, Ed.). In contrast to the Eurozone, a sharp rebound in the Manufacturing PMI to 49.6 from 46.2 (though at odds with the sector CBI survey) accounted for the rise in the overall PMI, with Services holding at a modestly expansionary 51.1. BoE MPC hawks will likely dig in their resistance to further rate cuts on the back of this run of data, arguing that with inflation still elevated, and the economy expanding moderately, the BoE should wait for more tangible proof that CPI is heading back to target,.

** October ‘flash’ PMIs **

Both Japan and India’s PMIs were disappointing. Japan’s Manufacturing eased to a 19-month low, while the Services PMI dropped to 52.4 from 53.3, with the former seeing an uptick in output, but Orders fell to an 18-month low. By contrast India saw a slight improvement in Manufacturing, but Services falling a 5-month low of 58.8 from 60.9, still within the range for 2025, but towards the lower end, and doubtless suffering from trade tensions with the US. Eurozone readings were again about the stark contrast between Germany, where the Services PMI surged to a 30-month high of 54.5, and a down at heel 47.1 from 48.5 for Services in France, in both cases Manufacturing PMIs remain contractionary, and were little changed for the month. But one has to observe that survey readings in France are riddled with inconsistencies, given that the PMIs completely contradict local surveys that saw Manufacturing and Consumer Confidence jump – per se it would be wise not to over-interpret what were a very noisy collection of surveys.

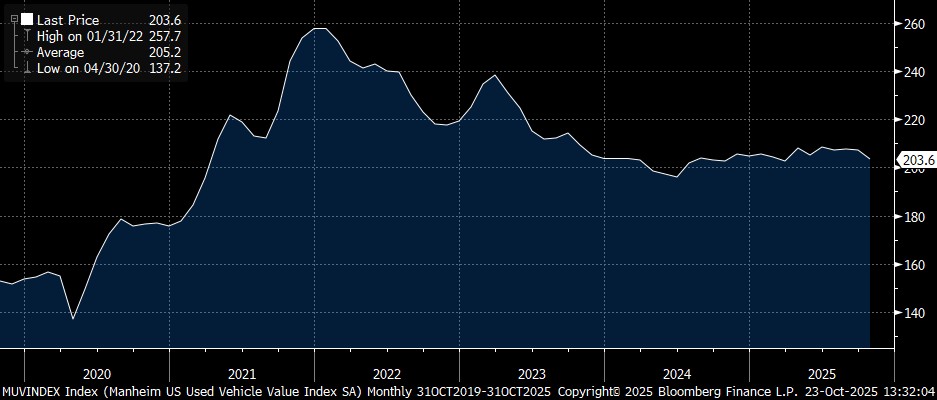

** U.S.A. – Sep CPI **

The delayed September CPI data is primarily being published as it also provides the benchmark for 2026 increases in social security payments. There will also be considerable scepticism about its accuracy given the protracted government shutdown will have hampered data collection. Be that as it may, it is forecast to show headline CPI unchanged at 0.4% m/m but rising to 3.1% y/y (from 2.9%), and core CPI at 0.3% for an unchanged 3.1% y/y, though 3-mth annualised rates would rise to 4.0% and 3.6% respectively (contrast that with the UK headline 3-mth annualised rate of just 1.6% y/y). If forecasts are correct, then it would question why the Fed seems determined to cut rates by a further 25 bps at its next two meetings, when inflation is accelerating, equity markets are close to all-time highs, credit spreads are tight, even if labour demand is weak. That said, the risks look to be to the downside of consensus on headline and core, with used auto prices slowing sharply (as per the Manheim index – see chart), and prior pressures from Airfares and Hotels/Restaurants also reversing, as well as evidence of prior tariff related increases in some goods prices having to be reversed, as consumers tighten their purse strings. Flash PMIs are forecast to ease m/m: Manufacturing 51.8 vs. Sep 52.0, Services 53.5 vs. 54.2.

Source: Bloomberg Finance L.P.