Written Commentary

A busy day awaits on all fronts, with a heavily front loaded data featuring the overnight China Q4 GDP and monthly activity and property indicators, UK labour data, Australian Consumer Confidence and Singapore Exports ahead of Germany’s ZEW survey, US NY Fed Manufacturing survey and Canadian CPI. There are ECB and Fed speakers, OPEC’s monthly Oil Market Report, while Goldman Sachs, Morgan Stanley and United Airlines top the run of US corporate earnings. Govt bond supply takes the form of UK 2-yr, German 5-yr and Finland 4 & 9-yr. Germany’s ZEW Expectations is forecast to rise for a fourth month from Dec -23.3 to -15.0, with the risks to the upside given the strength of the Dax in recent weeks, with which the index is closely correlated; Current Conditions are also seen higher at -57.0 vs. December’s -61.4, and with activity data proving much better than feared, and inflation pressures easing, it may post a stronger rise, even if it remains at depressed levels from a longer term perspective.

** China – Q4 GDP **

Both GDP and the December activity data were considerably better than expected, and yet there is no mistaking that they were still poor. At flat q/q 3.9% y/y and at just 3.0% y/y for 2022, GDP was much weaker than the initial govt target of 5.5% and below the reduction to an estimate of ca. 4.0% later in the year. There will be many who view the data with a good deal of scepticism given the anecdotal evidence, above all the fall in the (often quite volatile) Unemployment Rate to 5.5% vs. an expected 0.1 ppt rise to 5.8% and the still very weak, but better Retail Sales at -1.8% y/y. Unsurprisingly Property Investment (-10.0% y/y) and Residential Property Sales (-28.3% y/y) were little changed, and underlining that restoring confidence in the sector will take time and considerable effort. The data will inevitably prompt upward revisions to 2023 GDP estimates, though the re-opening recovery will likely remain somewhat bumpy, and resolution of the property sector woes in balance sheet terms, and fading external demand will continue to present considerable headwinds. It also suggests that the expected fiscal boost and indeed PBOC policy easing measures may not be as significant as some had hoped.

** U.K. Nov/Dec Unemployment & Wages **

A somewhat mixed report with HMRC Payrolls rising just 28K against expectations of 63, with November’s increase revised to 70K from 107K, but hardly indicative of a significant easing in labour demand, as was confirmed by a still sky high Vacancies at 1.161 Mln (down a meagre 27K), while Nov LFS Employment measure was a tad better than the expected flat, but soft at 27K. Both headline and ex-Bonus Average Weekly Earnings rose a little more than expected at 6.4% y/y. However as noted in the Week Ahead, any analysis has to take very adverse base effects from 2021 into account, i.e. from a peak of 7.3% y/y in June 2021, the core ‘ex-Bonus’ measure fell to a trough of 3.6% in December, with the fall from October to November being 4.3% to 3.8%. Per se, most of the increase is down to base effects, and while wages are clearly rising at a much faster pace than pre-pandemic, they remain deeply negative in real terms, whatever the outcome of tomorrow’s CPI data.

** Canada – Dec CPI **

Yesterday’s Bank of Canada Q4 Business Outlook survey saw the headline index fall again to 0.1 from 1.7, and more importantly, the Future Sales reverse the tentative rebound in Q3 (-24.0 vs -18.0), while Consumer Wage Growth expectations slowed somewhat and 2 & 5-yr Inflation Expectations also dropped, per se suggesting that the BoC’s aggressive 2022 rate hikes are having an impact. Falling energy prices are likely to be the primary factor in an expected -0.5% m/m headline CPI drop that would see the y/y rate fall to 6.4% y/y from 6.8%, but core CPI is only seen easing a modest -0.1 ppt on both measures to a still very lofty 4.9% y/y and 5.2% y/y respectively. Anything lower than expected will likely prompt markets to reduce the current 70% probability of a further and final 25 bps hike at next week’s meeting.

** Japan – BoJ policy meeting **

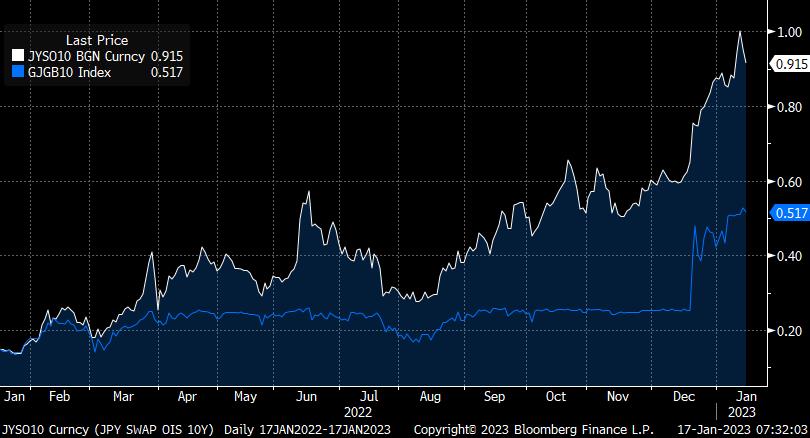

The consensus expects no change in either the Call Rate or 10-yr JGB yield targets, nor any further adjustments to the bandwidth on the latter. That said, markets would appear to be discounting the risk of a further move if the pressure on 10-yr JGB yields, and a colossal widening in the 10-yr JPY OIS swap spread (see chart) are anything to go by.

However the latter is far more technical than some would have us believe, and consequent on the December band widening, and testament to the fact that Japan’s money markets have been ‘cryogenically frozen’ for many years, thanks to BoJ policy. Restoring JPY money market functionality was always going to be painful, as well as sending shock waves elsewhere, and was always going to be a sine qua non before the BoJ could start to wind back its ultra-easy monetary policy. The BoJ will update its forecasts, with current FY core CPI likely to be revised up slightly from 3.9%, but the issue is whether it tweaks its forecasts up for the following 2 years from prior estimates for both of 1.6%, i.e. falling short of the 2.0% target; GDP forecasts for FY 2022 & 2023 may be tweaked modestly lower. If FY 2023 CPI forecast is revised higher (?1.8%), the BoJ may well emphasize that this is primarily due to continued supply problems, and reiterate that a shift in policy would have to see both stronger (domestic) demand and an acceleration in wage growth. Given the dislocation of JPY Swap rates relative to JGB yields, it will underline that it is monitoring and assessing related financial stability issues, but is unlikely to adopt or announce any specific measures to deal with this.