Written Commentary

The FOMC rate decision and press conference will likely render much of the remaining data and events moot, though UK monthly GDP and Swedish CPI will have an impact on their respective domestic markets. There are German and Indian WPI to digest, with US PPI and Brazilian Retail Sales ahead, along with the last of this month’s Oil Market reports from the IEA. A light day for govt bond issuance sees Germany sell 10-yr, while homebuilder Lennar is the highlight on the corporate earnings calendar. Yesterday’s sharp about turn in US Treasury yields which initially feel in reaction to CPI, but quickly reversed, underlines poor underlying liquidity conditions, as well as the risk of some spiky volatility after the FOMC decision.

** U.K. – April GDP and activity indicators **

There were very few surprises in today’s data, with both monthly GDP and Index of Services exactly as expected, though the detail reveals that strength in retail and the TV/Film sector offsetting a small drag (-0.07 ppt) from health, the latter due to strikes; manufacturing and Construction were also a drag. But given the much stronger than expected rise in basic wages seen in yesterday’s labour report, today’s activity data will be a minor consideration in next week’s MPC rate decision, at which markets now see a risk of a 50 bps hike, with next week’s CPI data now the key factor.

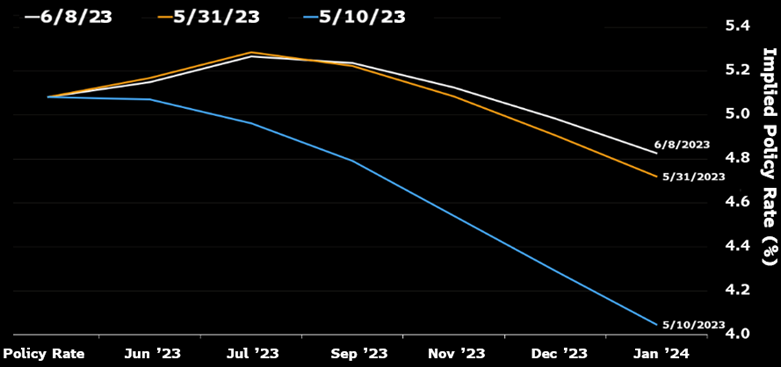

** U.S.A. – FOMC meeting / PPI **

Yesterday’s CPI was mixed with headline a tad below forecasts at 4.0% y/y, while core CPI slipped slightly less than expected to 5.3% y/y, though the core Services ex-Housing sub-index encouragingly dropped to 4.6% y/y, with higher than expected OER (housing) and a sharp jump in Used Auto Prices accounting for much of the headline core CPI pressure. That outcome should be sufficient for the Fed to justify a widely discounted decision to keep rates unchanged (at 5.00/5.25%) for the first time since the Fed started hiking rates in March 2022. Nevertheless, the latest ‘dot plot’ and Powell’s press conference are expected to hint at a July rate hike. The committee’s forecasts are also likely to see marginal upward revisions to growth and inflation forecasts, and a downward revision to Unemployment. Watch out for potential for some dissent on the rate vote, with both Bowman and Kashkari recently suggesting that the case for a pause had as yet not been made. While markets have back reversed much of the rate pivot that had been anticipated in April, and continue to anticipate the risk of rate hike in July (see chart), but still look for a rate cut by year end. What Powell and the FOMC will wish to avoid is markets ‘misinterpreting a pause’ as a pivot signal, and this will be their biggest challenge. It could if it chooses lean on the second policy target, namely Employment, emphasizing that labour demand remains very robust, and the economy relatively resilient, and that this continues to pose an upside risk on inflation going forward, and rules out a pivot well into next year, though this would leave it hostage to fortune, in a which ‘data dependent’ does not. PPI is likely to underscore the already evident diminishing pipeline pressures, with headline expected to fall to 1.5% y/y from 2.3%, and ex-Food, Energy & Trade to 3.0% y/y from 3.4%.