Written Commentary

Today will be all about the US CPI data, even though there are other statistical items on the agenda, including the overnight UK labour data, Japan BSI survey and PPI, Australia NAB Business & Westpac Consumer Confidence, with Germany’s ZEW and US NFIB surveys ahead. There are a good number of central bank speakers, but all are from the regulatory departments, with no monetary policymakers scheduled, though some more impromptu hawkish signalling from ECB officials is a distinct possibility. Govt bond supply is quite plentiful, with Italy selling 3, 7 & 24 yr, Germany 2-yr and the US 30-yr. On the political front, all eyes remain on the recent successes of Ukraine in re-taking parts of the Northeast and South, as the UN’s 77th General Assembly opens in New York.

** U.K. – Labour data review / CPI & PPI preview **

Outside of the tepid 40K increase in May-Jul LFS Employment and a drop in the ILo Unemployment Rate to a new low of 3.6% due to a further rise in inactivity, the labour data were broadly in line with expectations, but underline that it is the rise in inactivity which is key, and that is something which fiscal rather than monetary policy needs to deal with. The 34K drop in Vacancies was the largest since the start of the pandemic, but still leaves total Vacancies at 1.266 Mln running 50% higher than pre-pandemic. August HMRC Payrolls’ solid 71K rise suggest that the soft LFS Employment measure should be dismissed, while Average Weekly Earnings at 5.5% y/y headline and 5.2% y/y ex-Bonus confirms that basic pay is now in the driving seat of pay gains, but still leaves real wage growth down 2.8% y/y, and given the level of vacancies and inactivity, as well as adverse base effects, also implies that while wage pressures are rising, they are hardly running away with themselves. Focus now turns to CPI, with headline anticipated to be up an unchanged 0.6% m/m to edge the y/y rate down 0.1 ppt to 8.7%, but conversely core CPI is expected to edge up 0.1 ppt to 6.3%. Pipeline pressures as measured by PPI are expected to ease in m/m terms, but not y/y.

** Germany – September ZEW survey **

Given that the energy crisis is only getting worse, despite the recent drop in gas and power prices, and the fact that the Dax has been on the back foot and volatile, it is not surprising that the ZEW survey is forecast to see a drop in Expectations to -60.0, close to its 2008 low of -63.9, and a further drop in the Current Situation to -52.1 from -47.6.

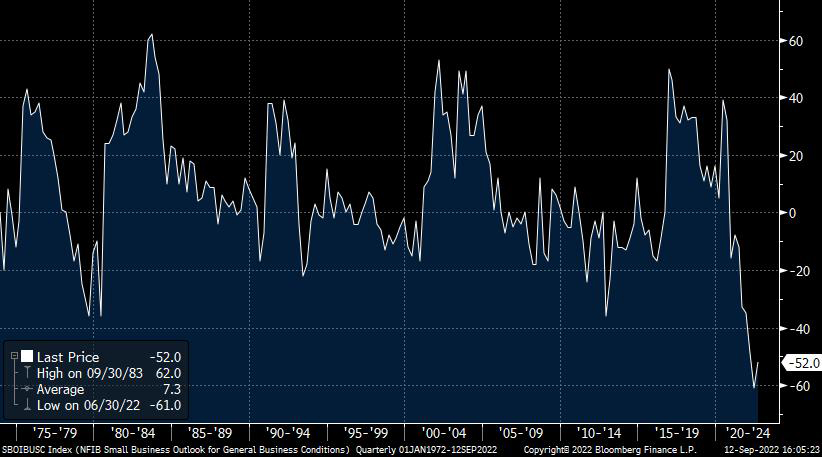

** U.S.A. – August CPI / NFIB Small Business Optimism **

US CPI gets top billing today, with the headline rate seen dipping 0.1% m/m on gasoline prices, while core is seen up 0.3% m/m, which would see headline dip to 8.0% y/y from 8.5%, but core rising to 6.1% y/y from 5.9%, as housing and services pressures, override lower auto and other goods prices. Even a downside miss on CPI seems unlikely to deter the Fed from a 75 bps next week, above all due to the strength of core CPI, which remains a long distance from its 2.0% target, and with headline hardly falling at a significant pace for the time being. The NFIB survey is expected to see a marginal pick up to 90.8 from 89.9 and June’s low of 89.9, primarily due to lower gasoline prices, with the already published Employment indices showing some modest improvements, but critical will be the Small Business Outlook which did rebound from its all-time low of -61.0 in June to -52.0, but as the chart attests, it remains far below any previous low.