Written Commentary

A busy week for data and events gets off to a rather subdued start, with little more than Saturday’s China inflation and Credit Aggregates to digest ahead of Indian CPI and NY Fed Inflation Expectations survey, and just a sprinkling of central bank speakers, though none from the Fed, while Petrobras head a modest run of corporate earnings. The BoJ cut to its 5-10 yr JGB purchase volume (Y425 Bln vs. prior Y475 Bln) is of greater importance in signal terms rather than real market impact, given its gargantuan balance sheet. But coming alongside comments from govt officials urging the BoJ not to delay normalization because of risks, it does say the direction of travel is towards more rate hikes (though still only closing the rate gap marginally with the rest of the G7) and a steady reduction in QE purchases.

RECAP: The Week Ahead – Preview:

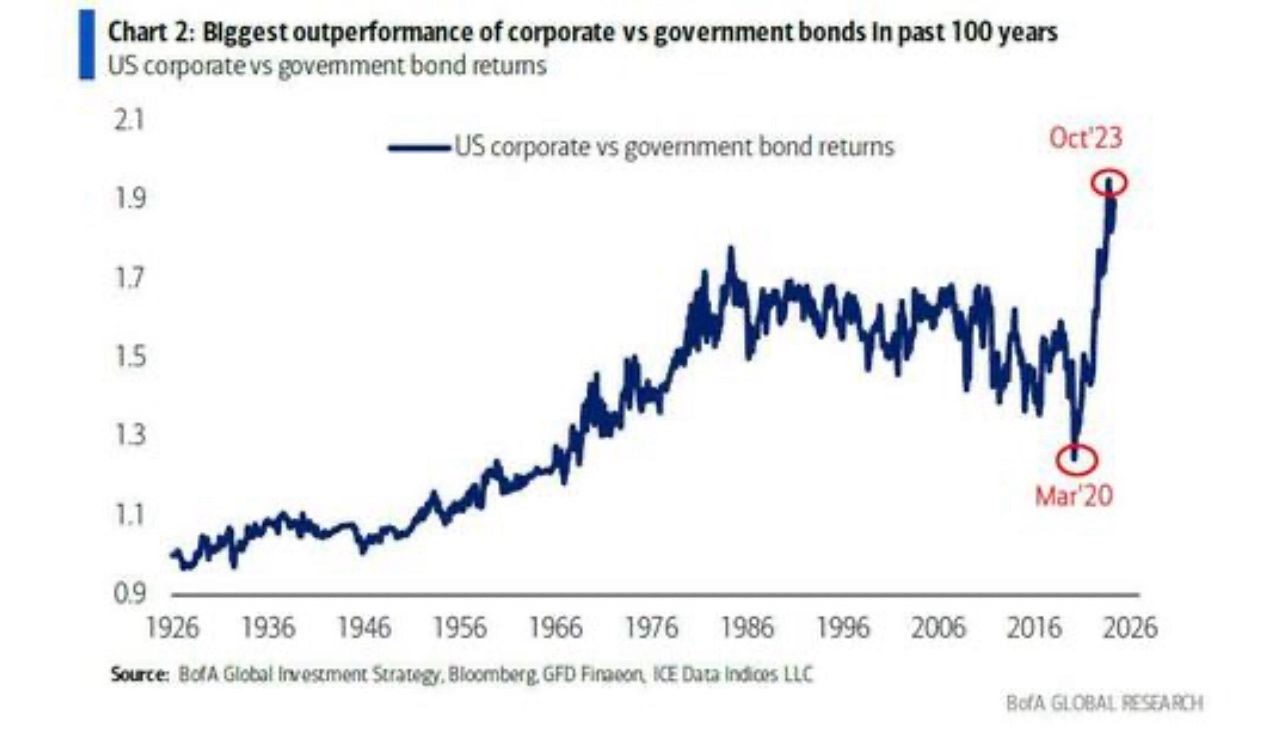

The new week has a deluge of major economic data from the US (CPI, PPI, Retail Sales, Industrial Production, NAHB, Housing Starts), and China (Retail Sales, Industrial Production, FAI, Property Investment, House Prices), with the UK looking to labour data, Japan to Q1 GDP, Australia to Unemployment, and Eurozone to final CPI, revised Q1 GDP and Germany’s ZEW survey, as India awaits CPI, WPI and Trade. China will have its monthly 1-yr MTLF operation and there are again a lot of central bank speakers, though no major central bank policy meetings. Geopolitics will remain very sensitive as Putin visits China, and the brutal conflicts in Gaza and Ukraine continue. A busy week in the commodity space, as both OPEC and IEA publish monthly Oil Market Reports, as Iraq sent conflicting signals on extending OPEC production cuts over the weekend, with a raft of conferences this week including the Qatar Economic Forum, BofA Metals & Mining Conference and Cobalt Congress in US, GrainCom in Switzerland, and the Antaike Copper conference in China, while there are grains S&D reports from France’s Agriculture Ministry and Brazil’s Conab. The European Commission publishes its Spring economic forecasts, and the ECB its Financial Stability Review. The US corporate earnings season is winding down but has Deere & Co, Home Depot and Walmart reporting, while elsewhere China’s tech behemoths Alibaba, JD.com and Tencent reporting, with Bayer, Sony and Japan’s major banks and Japan Post also reporting results. Market views on major central bank rate cut prospects and timing remain very fluid, but are currently supporting risk appetite and subduing volatility, though the very tight level of corporate credit spreads and their huge outperformance vs. Govts in the past four years are flashing warning signs (see chart). It will be a busier week for govt bond issuance in the Eurozone and Japan, but no coupon supply in the USA.

U.S.A. – While the focus will be on Tuesday’s PPI and Wednesday’s CPI, Monday’s NY Fed 1-yr Inflation Expectations (steady at 3.0% since December) will require attention after the jump in the Michigan measure to 3.5% y/y from 3.2%. Unusually PPI precedes CPI, with headline seen up a relatively well contained 0.2% m/m to edge the y/y up 0.1 ppt to 2.2%, while core is seen up 0.3% m/m, and the y/y rate slipping to 2.3$ from 2.4%; headline will be boosted primarily by energy (gasoline) prices, with some upside risks to core given rises in Manufacturing survey price indices, and a close eye needs to be kept on Financial Services which has been pressuring the core PCE deflator. CPI will again be uncomfortably high for the Fed, with food (above all eating out) and energy pushing up headline a further 0.4% m/m taking the 3-mth annualized rate to 4.8%, though base effects will edge the y/y rate down to 3.4%, while core is seen up 0.3% m/m, with the y/y expected to drop to 3.6% from 3.8%. The latter will be subject to conflicting forces as Housing costs and Used Car Prices ease somewhat, but Insurance and Medical Services will exercise upward pressure. Per se, it looks as though growth and labour data will have to do the heavy lifting if Fed rate cut caution is going to ease. Retail Sales are expected to cool to 0.4% m/m headline and 0.1%/0.2% m/m after surging 0.7% and 1.0%/1.1% respectively in March, a close eye needs to be kept on the balance of consumer spending between essentials and discretionary & big-ticket items. Industrial Production and Manufacturing are forecast to rise just 0.1% m/m, after relatively robust prints of 0.5% and 0.4% in March, headline may be boosted by utilities due to warmer weather, while surveys hint at downside risks to Manufacturing Output. The highly erratic NY Fed Manufacturing is best ignored, while the Philly Fed Manufacturing is seen giving back much of April’s jump to 15.5 from 3.2 with a slip to 7.5. Tuesday’s NFIB Small Business Optimism is expected to remain very subdued at 88.2 (March 88.5), echoing the already published Employment components, which saw Hiring Intentions little changed at 12, after falling to a 4-yr low of 11 in March, while the NAHB Housing Market Index is again expected to be unchanged at 51. Initial Claims will be closely watched after last week’s jump to 231K, though forecasts assume the latter was largely aberrant with a slip to 220K anticipated. Overall, if forecasts are correct, this would hint at a further loss of growth momentum, but not of the variety that will have the Fed easing up much on its recently more hawkish rhetoric.

China: The weekend inflation and credit aggregates offered little in the way of encouraging news, with Food prices (-2.7% y/y) continuing to weigh on headline inflation (0.3% y/y), and both core and services CPI holding at 0.9% y/y. Meanwhile, even the boost from very benign base effects still saw PPI miss forecasts at -2.5% y/y. Credit aggregates do have to be taken in the context of the outsized rises in March and typical seasonal trends, but New Yuan Loans at CNY 720 Bln (vs. expected CNY 800 Bln) were weak even if unchanged in y/y terms at 9.6% y/y, while the CNY 200 Bln fall in Aggregate Social Financing against expectations of a rise of CNY 1.0 Trln (and posting record low growth of 8.3% y/y), along with a sharp and unexpected drop in M2 to 7.2% y/y from 8.3% continue to suggest that credit demand is very weak, and a further cut in rate will do little or nothing to boost confidence. Friday’s activity data are expected to see April readings improve on March, as LNY timing effects unwind, but year to date readings across the gamut of Retail Sales (4.7% y/y), Industrial Production (6.0%), Fixed Asset investment (4.5%) and Property Investment (-9.6%) are seen barely changed from March, with the surveyed Unemployment Rate also expected to hold at 5.2%. A more sustained and meaningful recovery still looks rather elusive, as property sector woes continue to offset very notable strength in High Tech and energy transition related output. Property developer balance sheet resolution remains a sine qua non if the much hoped for recovery, particularly given headwinds to external demand from geopolitical tensions.

UK: After a relatively dovish message from last week’s BoE policy meeting and forecasts, the focus turns to the latest set of labour data, with Average Weekly Earnings seen easing only very modestly (-0.1 ppt) to a still high 5.5% y/y headline and 5.9% ex-Bonus. HMRC Payrolls (last -67K) and an expected accelerated decline to -215K from -156K in the much maligned LFS Employment measure are however expected to suggest a meaningful loosening in labour demand, with a further modest rise in the Unemployment Rate to 4.3% from 4.2% anticipated. Barring weaker than expected readings (and bearing in mind often hefty revisions), it would put rather more onus on next week’s CPI data in terms of enhancing the chances of an initial June rate cut. Bernanke will testify to Parliament’s Treasury Select Committee on his recent report, and the BoE’s hawks (Greene and Mann) will be speaking.

Japan: This week’s Q1 provisional GDP may prove to be somewhat of a red herring as far as BoJ rate expectations go, given that the anticipated -0.4% q/q (or -1.4% SAAR) will owe much to the shutdown at one automaker due to a safety scandal, which will contribute heavily to a sharp reversal in Business Spending (-0.5% q/q vs. Q4) along with a mean reversion in exports (forecast to drag GDP 0.3 ppt lower), which were artificially boosted by industrial ‘royalties’ in Q4. That said the continued expected weakness of Private Consumption (forecast -0.2% q/q vs. Q4 -0.3%) will continue to worry the BoJ, even if the slowdown in Nominal GDP growth to 0.2% from 0.5% may offer some comfort.

Elsewhere neither Eurozone April CPI or Q1 GDP are expected to be revised from preliminary readings, while Germany’s ZEW survey is seen edging up again to 44.9 from April’s 42.9 on the Expectations measure, and also on Current Situation, though still very depressed at -76.3 from -79.2. Australian Q1 Wages are forecast to be unchanged at a fairly lofty 0.9% q/q 4.2% y/y, which will continue to act as a restraint on the RBA shifting to a more dovish stance, though the contrast between strong public sector wages and an easing in the private sector needs to be monitored. Monthly Employment is seen recovering to a rather average 23.7K after unexpected falling 6.6K (watch for revisions) in March, with the Unemployment Rate expected to be unchanged at 4.2%. Tuesday’s Indian CPI is expected to ease modestly to 4.8% y/y from 4.9%, on the back of lower Food and core goods prices, and this should also see a further small slip in the RBI’s core CPI measure from March’s 3.3%. Trade data are likely to see a very typical seasonal fall in both Exports and Imports, the former stronger than the latter, thus contributing to a widening in the Trade deficit to $-17.2 Bln from March’s $-15.6 Bln.- There are just 13 S&P 500 companies reporting this week, with worldwide highlights for the week as compiled by Bloomberg News likely to include: Airports of Thailand, Alcon, Alibaba, Allianz, Applied Materials, Baidu, Banco BTG Pactual, Bayer, Bharti Airtel, Bridgestone, Cisco Systems, Compass Group, Deere, Deutsche Telekom, E.ON, Engie, Experian, Ferrovial, Hannover Re, Hapag-Lloyd, Hindustan Aeronautics, Home Depot, Hon Hai Precision Industry, Hoya, Japan Post, Japan Post Bank, JD.com, JSW Steel, KBC Group, Merck, Mitsubishi UFJ Financial, Mizuho Financial, PetroBras, PTT, Recruit, Richemont, RWE, Sea, Siemens, SMC, SoftBank, Sony, Sumitomo Mitsui Financial, Swiss Re, Tencent, Terumo, Walmart.