Written Commentary

There is little on the data schedule that will trouble summer markets, with Japan’s PPI and Australia’s Q2 Wage Price Index to digest and nothing of significance ahead. The IEA rounds off this week’s round of monthly oil market reports, and will also publish its annual energy market statistical supplement. The Bank of Canada’s July policy meeting minutes are accompanied by some further Fed speakers.

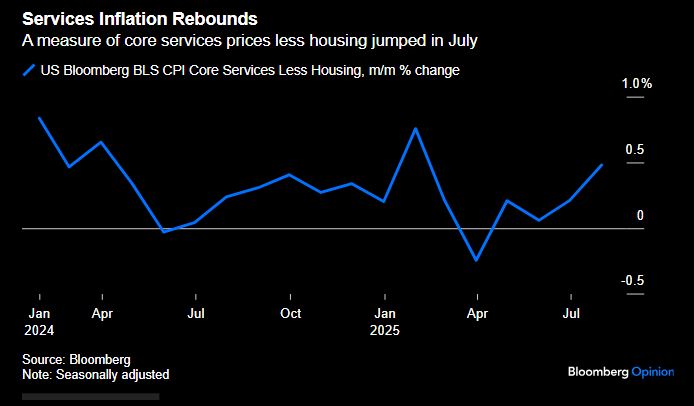

Yesterday’s US CPI has been construed as confirming the likelihood of a Fed rate cut in September, and yet core CPI was slightly above expectations 0.3% m/m and a very lofty 3.1% y/y (relative to target). While good price inflation remained relatively subdued, which some will interpret as signalling a modest impact from tariffs, it remains the case that the impact of tariffs, which has been persistently delayed, will only start to meaningfully show up in coming months. Rather more worryingly, especially for the likes of the dissenting Waller (Bowman’s case appears to rest far more on the labour data – i.e. the data for which the head of the BLS was ‘fired’) is the upturn in Services CPI (0.3% m/m 3.8% y/y), above all ex-Housing at 0.5% m/m. To be sure Airfares (4.0% m/m) had a sharp impact, but as the attached chart highlights, the seasonal trend is running a good deal higher than in 2024, and it would be disingenuous to suggest that it is consistent with core CPI converging to the Fed’s 2.0% target. Be that as it may, risk assets, above all equities, celebrated this with a move to new highs in many cases. The latter is being given extra rocket fuel by speculation about a potential 50 bps rate cut in September, presumably partially rationalised by Miran’s temporary appointment to the FOMC. The case against 50 bps primarily boils down to last year’s 50 bps cut having been a mistake, above all due to FOMC members over-interpreting the transient weakness in labour demand last summer (sic! Ed.), which one might add probably contributed to the extended pause in rate cuts this year. Be that as it may, the other key drivers of the current rally, aside from Q2 earnings (above all Mag 7) is very subdued interest rate volatility. As can be seen both in the chart of the narrow range in which the Dec 2025 SOFR future has traded over recent months, and over the year to date as a whole compared to the 2024 rate expectations roller coaster, and the very low level of the MOVE Treasury volatility index, which is in turn helping to keep the VIX subdued. Of course what is missing from this rationale is any discussion of tariffs, geopolitical tensions, uncertainty, policy ambiguity, or political interference in monetary policy, which fits with markets whose reaction function has been severely impaired (above all by QE liquidity, which has not risen this year despite QT programmes), and is largely reliant on momentum trades, with the derivatives tail very much ‘wagging the dog’. This is a classic example of a perception vs. reality divide that has a tendency to unravel in a disorderly fashion, though the degree generally varies according to happenstance, the worst example being the GFC.