Written Commentary

Last Friday’s labour data was rather more mixed than the higher than expected Payrolls implied, above all a weak Household survey showing 226K drop in Employment and a 134K rise in Unemployment, but a steadier labour market relative to Q4 will keep the FOMC focussed on inflation risks, regardless of who is Fed Chair. Markets were not particularly unsettled by the gasoline and airfare paced 0.9% m/m surge in headline CPI, due to the modest 0.2% m/m rise in core CPI, but may be more sensitive to another expected jump of 0.6% m/m on headline to take the y/y rate up to 3.7%, with core CPI forecast at 0.3% m/m to edge the y/y rate up to 2.7%. Gasoline prices will again be a key driver, but within the travel/leisure category a fall in Hotel and other leisure activity prices may help to offset another jump in airfares. Some upward pressure from Shelter (housing) prices will primarily be a case of unwinding the artificial downward pull in this category during October’s government shutdown. Upside inflation risks from the Middle East and the transition from Powell to Warsh are set to keep the FOMC on hold well into H2 2026, but expect the generally hawkish bias from many regional Fed governors to re-emerge if there is another upside miss.

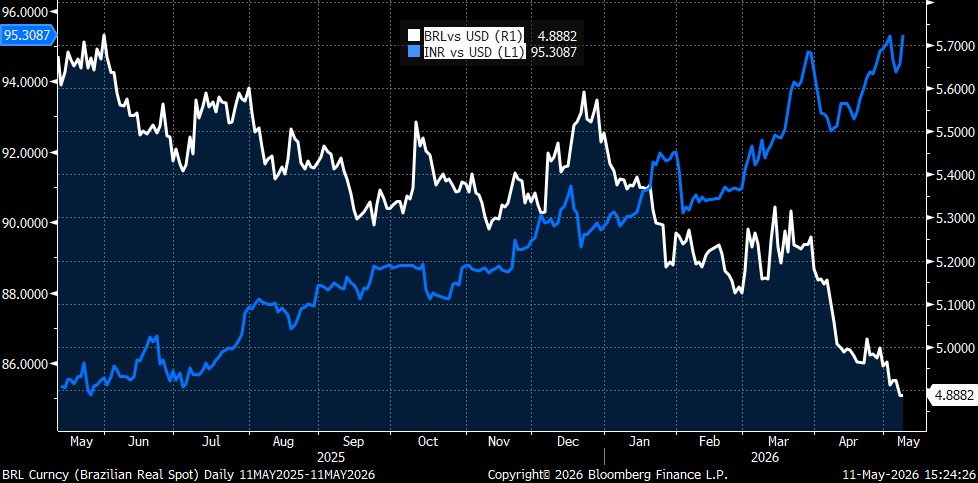

One of the starkest contrasts in the major EM economies on energy price pressures is between energy rich Brazil and large-scale energy importer India, most visible in the huge divergence between a very strong Brazilian Real and a very weak Indian Rupee (see chart). Indian CPI has climbed sharply from a cyclical low of 0.04% in October to 3.4% y/y in March, and is expected to climb to 3.78% y/y, while adverse base effects accounted for some of the initial rebound, a weak INR and latterly energy prices may push inflation well above the RBI’s 4.0% (+/-2.0%) target in coming months. For the time being, the RBI is happy to argue that inflation remains under control (as per RBI deputy governor Gupta last week), as fuel tax cuts have mitigated the upward pressure on energy prices, with food prices expected to have been the primary upward pressure point in April. But the fiscal scope to maintain or increase fuel tax cuts is limited, and if no deal is reached between the US and Iran soon, then some pass through of higher energy prices to consumers would be inevitable. For all that Brazil is energy resource rich, it is not immune to the fall-out from the Middle East conflict, as was evident in the 0.88% m/m gasoline price related jump in March pushing the y/y rate up to 4.14%, with April data seen up a further 0.67% m/m as a sharp drop in airfares offsets food price pressures and annual increases for medicines. But this would leave y/y inflation at 4.4%, only just below the top of the BCB’s target range of 3.0% (+/-1.5%), and limiting its scope to cut rates further, with the Selic rate target seen at 13.0% by year-end (vs. current 14.50%).