Written Commentary

While the focus will be on US CPI, there are plenty more major data points, with China’s inflation readings, Japan’s Economy Watchers survey and Norwegian monthly GDP to digest, ahead of Brazil Services Output, US weekly jobless claims, Indian CPI and Industrial Production. Fed speakers will be quite plentiful, the ECB publishes its Economic Bulletin, while Agricultural commodities will be focussed on the USDA’s monthly WASDE report, which follows on from the equivalent S&D report from China’s Agriculture Ministry. Govt bond supply remains plentiful, with Italy selling 3 & 7-yr, Spain 3, 7 & 23-yr, Canada 2-yr and the US 30-yr, with the usual start of year rush of corporate issuance in USD and EUR continuing at a rapid pace, and serving as reminder of the very high level of refinancing which needs to be transacted this year.

** China – December CPI & PPI **

CPI edged up a modest 0.1 ppt to 1.8%, but given Food Prices jumped to 4.8% y/y from 3.8% due to base effects, this continues to underline that domestic demand remains very week, as was emphasized by a much lower than expected -0.7% y/y for PPI, despite strong upward base effects. That said the initial disruption from re-opening was always likely to bear down on demand and by extension prices, and it may take a few months before any genuine trend in prices can be discerned.

** India – December CPI, November Industrial Production **

Headline CPI is seen little changed at 5.9% y/y, just below the top of the RBI’s 2.0%-6.0% target range with food prices seen falling on a combination of base effects, an extension of the free food programme and a larger than typical seasonal fall in vegetable prices. Core inflation is however likely to remain above target (last 6.5% y/y) and may tick higher on the back of a rise in gold & silver prices, and see some pressure arise in freight costs. Given that PMIs continue to signal that India’s economic growth is defying the loss of momentum being witnessed in East Asia, Europe and North America, the stickiness of core CPI is likely to prompt the RBI to hike rates by a further 25 bps in February. The anticipated sharp rebound in Industrial Production to 3.2% y/y after a steep 4.0% fall in October will be mostly down to calendar effects, with the Diwali holiday having been in October in 2022 as against November in 2021, though also echoing a further rise in the Manufacturing PMI.

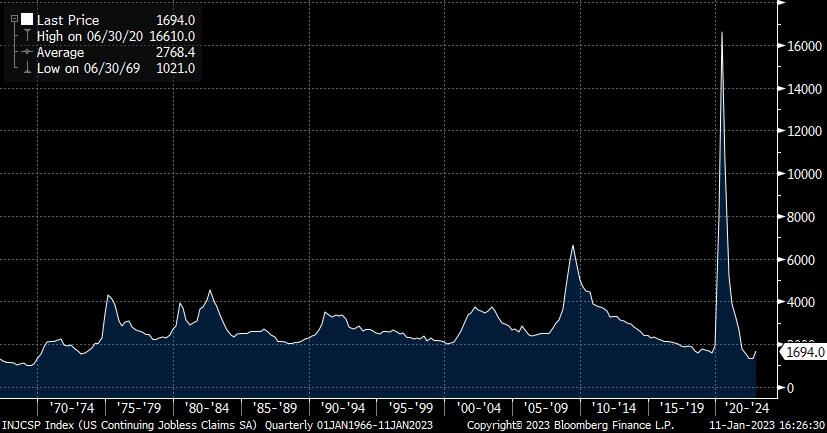

** U.S.A. – December CPI, Weekly Jobless Claims **

As is well documented, US CPI data has prompted very sharp market moves in the past 6 months, though it has to be added that going into this report, markets appear heavily skewed in expectation terms to a third consecutive downside surprise. The consensus looks for a heavily energy (gasoline) price driven dip of -0.1% m/m, which would take the y/y down to 6.5% y/y from 7.1%, with falling auto prices and retailer discounting to offload excessive inventories also in the mix; airfares should also drag. Housing (OER/Shelter) will continue to exercise some upward pressure, but probably at a somewhat slower m/m pace than the 0.6-0.8% seen in the past 6 months, and continue to see considerable offset from medical care, with core CPI seen posting a relatively modest rise of 0.3% m/m (vs. Nov 0.2%), though the focus will above all be on the ex-Food, Energy & Shelter measure that fell 0.1% m/m in both October & November, which if repeated would start to make a more compelling argument for the Fed to opt for a 25 bps (already discounted) hike in early February. The problem remains that this is already discounted, and as the Fed minutes observed: FOMC ‘participants noted that, because monetary policy worked importantly through financial markets, an unwarranted easing in financial conditions, especially if driven by a misperception by the public of the Committee’s reaction function, would complicate the Committee’s effort to restore price stability.’ As for weekly jobless claims, these are expected to see Initial claims rebound from 204K to a still super low 215K, with Continued Claims seen rising again to 1.709 Mln from 1.694 Mln. In terms of the latter, there are a number of analysts citing the percentage rise from September’s 1.364 Mln low as a sign of a significant loosening of the labour market. To which I would only respond, look at the attached chart going back to 1967 and tell me if this seems an appropriate way of assessing that number.