Written Commentary

Prices were $.01 lower while spreads were also slightly easier. Mch-26 futures closed just below its 50 day MA. Prices continue to hold in a $4.35-$4.55 range. Friday’s CFTC report showed MM’s were net buyers of over 71k contracts in the week ended Oct. 28th, reducing their short position to 89.5k contracts. Export sales the week ended Nov. 6th at 39 mil. bu. bring YTD commitments to 1.509 bil. bu. up 28% from YA, vs. the USDA export forecast of up 9%. Export inspections as of Dec. 4th at 57 mil. bu. brought YTD inspections to 812 mil., up 69% from YA. Noted buyers were Mexico – 20 mil. and Japan with 12 mil. AgRural is forecasting Brazil’s 25/26 corn production forecast at 135.3 mmt, above the USDA est. of 131 mmt.

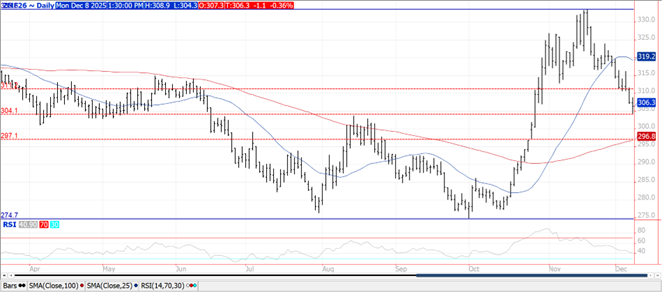

Prices were lower across the complex with beans down $.06-$.12, meal was off $1 while oil was 50 points lower. Bean and oil spreads weakened while meal spreads were slightly higher. Jan-26 beans fell to a fresh 5 week low while dipping back below $11.00. Next support is at $10.70. The low in Jan-26 meal just above $304 is a 50% retracement from the October low up to the November high. Jan-26 bean oil held support near its 50 day MA at 51.06. Spot board crush margins increased $.03 to $1.43 bu. with bean oil PV slipping to 45.5%. In the week ended Oct. 28th MM’s were net buyers of just over 83k contracts of soybeans, 49k meal while selling nearly 2k oil. The speculative buying in meal was the most in 1 week since March-2020 while the soybean buying was the most since May-2024. Soybean exports in the week ended Nov. 6th at only 19 mil. bu. brought YTD commitments to 651 mil. bu. down 40% from YA, vs. the USDA export forecast of down 13%. Export inspections as of Dec. 4th at 37 mil. bu. place YTD inspections at 474 mil., down 45% from YA. China finally showed up taking 4.4 mil. bu. Commitments to China as of Nov. 6th stood at 464k mt with additional announced sales since just over 2.6 mmt bring estimated commitments to nearly 3.1 mmt. Chinese soybean imports from all sources in Nov-25 at 8.1 mmt were down 14.5% from Oct. however up 13% from Nov-24. Imports over the first 11 months of 2025 at nearly 104 mmt are up 7% YOY. AgRural is reporting Brazilian plantings at 94%, just below the YA pace at 95%. They forecast production at 178.5 mmt, just above the USDA record production est. of 175 mmt.

Prices ranged from $.01 lower in CGO and MIAX to $.05 lower in KC. In the week ended Oct. 28th MM’s were net buyers of nearly 34k contracts of CGO, 16k contracts of KC while selling just over 200 contracts of MIAX. That was the most bought in 1 week for CGO futures since May-2019. Wheat sales the week ended Nov. 6th at 17 mil. bu. brought YTD commitments to 634 mil. bu. up 22% from YA, vs. the USDA forecast of up 9%. Export inspections at 14.5 mil. bu. were in line with expectations and brought YTD inspections to 501 mil. bu. up 21% from YA. APK-Inform forecasts Ukraine’s 2025 wheat production at 23.2 mmt, just above the USDA est. of 23 mmt.

Charts provided by QST.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.