Written Commentary

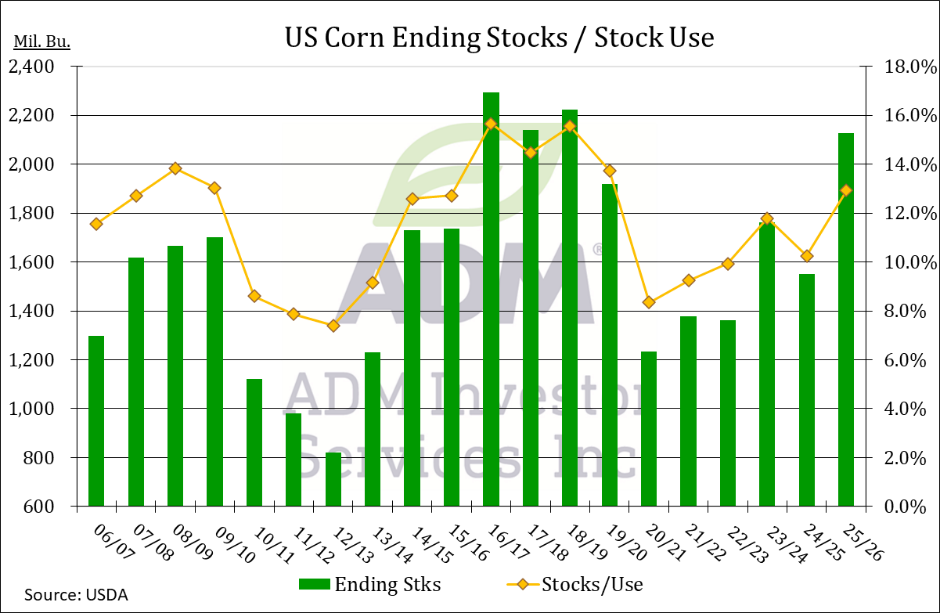

As expected there were minimal changes to the US balance sheets in today’s USDA WASDE update. Global inventories offered some surprises which were bearish for corn and wheat, while neutral to supportive for soybeans. Back to monitoring developments in the Middle East and US planting weather. Corn prices turned lower ahead of today’s USDA data and fell to new lows shortly after their release. Price closed $.01-$.03 lower while holding just above yesterday’s lows. Early strength tied to higher energy prices didn’t hold as RBOB futures finished near unchanged. The BAGE kept their Argentine production forecast unchanged at 57 mmt, well above the USDA forecast of 52 mmt. Harvest has reached 22%. US corn acres in drought plunged 15% to 29%.

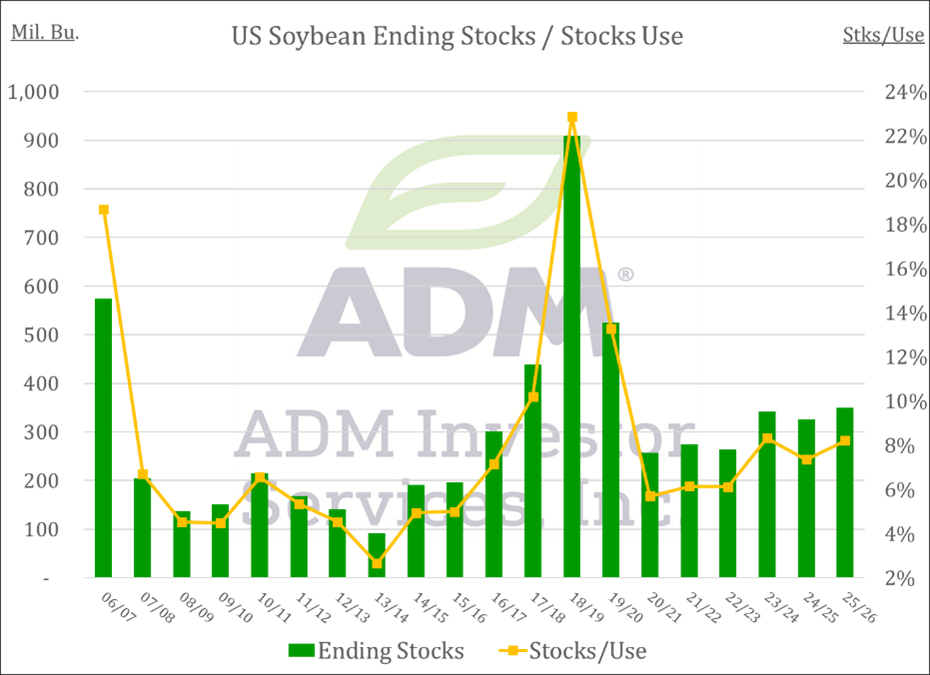

Prices closed slightly higher across the complex with soybeans $.01-$.03 higher, meal was up $2-$4 while oil was up 30-35 points. Spreads firmed across the complex. May-26 beans remain stuck between $11.40-$11.80. Spot crush margins rebounded $.07 ½ to $2.78 bu. while bean oil PV slipped to 51.6%. While energy/war headlines will continue to drive price volatility, the markets focus will likely begin to shift to the US planting season and Pres. Trump’s trip to China in mid-May. Chinese weapons supplied to Iran could complicate negotiations. The BAGE kept Argentine production at 48.5 mmt, just above USDA’s 48 mmt forecast. US soybean acres in drought plunged 13% to 31%.

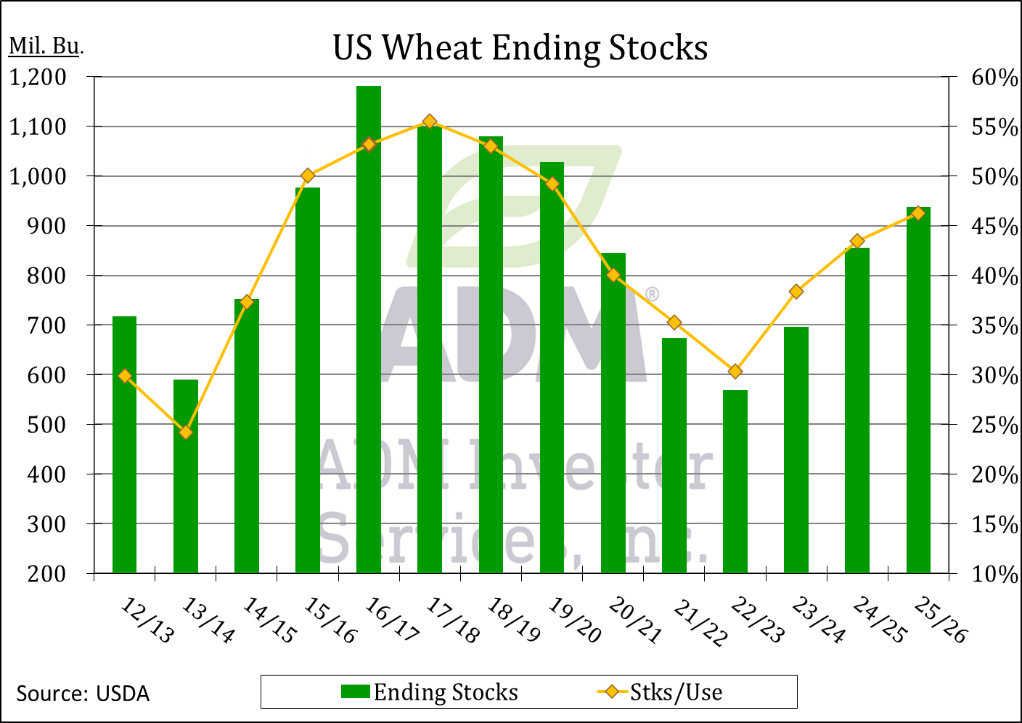

Prices were $.05-$.06 lower across the 3 classes. The July-26 contracts all carved out fresh 1-month lows. Next support for CGO July-26 is the March low at $5.74. KC July-26 held support at its 50 day MA at $6.01. Speculative traders appear to be quickly unwinding their recently established long position.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.