Written Commentary

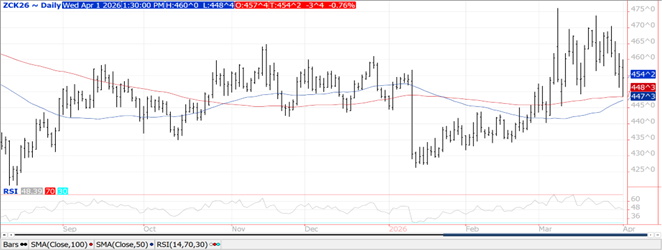

Prices were $.03-$.04 lower, finishing near the midpoint of today’s range. Spreads were steady to slightly weaker. May-26 held support right at its 100-day MA at $4.48 ½. July-26 corn at $4.65 is historically undervalued considering Mch 1st stocks / Q1&Q2 usage at 94% is well below the 10-year Ave. of 101%. Ethanol production slipped to 1,075 tbd, or 316 mil. gallons LW, down from 328 mil. the previous week, however was up 1% YOY. There was 106 mil. bu. used in the production process, or 15.15 mil. bu. per day, below the 15.44 pace needed to reach the USDA forecast of 5.6 bil. Implied gasoline usage fell 2.7% LW to 8.686 tbd, however was 2.2% above YA. Ethanol stocks slipped to 26 mil. barrels, below the 26.6 mb YA. Tomorrow’s export sales are expected to range from 40-60 mil. bu. Corn grind for ethanol production in Feb-26 at 425 mil. bu. was slightly above expectations of 422 mil.

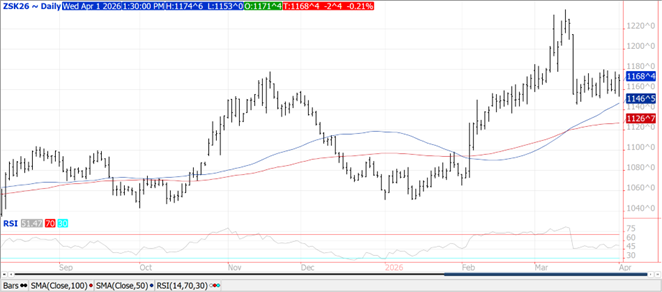

Prices were mostly lower across the complex with beans down $.02-$.03 closing well off session lows, meal was $2-$3 higher while oil is down 130-180 points. Bean and meal spreads were mixed while oil spreads weakened. May-26 beans have been stuck between $11.45-$11.80 for the past 2 weeks. Inside trade for Nov-26 beans. May-26 meal held support above this week’s low of $312.30. Initial support for May-26 oil is at 66.30. Lower energy prices weighed on commodity valuations. This AM President Trump stated that Iran’s Pres. asked for a ceasefire. He responded by saying he’d take it under consideration once the Straits of Hormuz was “open, free, and clear” while adding “until then, we are blasting Iran into oblivion or, as they say back to the Stone Ages!!” Pres. Trump will address the nation tonight, hopefully shedding light on US military objectives that remain and a timeline for their withdrawal from the Middle East. Crush margins slipped $.13 to $2.69 ½ while bean oil PV slumped to 51.3%. July-26 beans near $11.80 would historically appear overvalued given Mch 1st stocks / Q1&Q2 usage at 84.5%, however IMO justified given expectations for higher crush and possibly additional (but not likely) Chinese buying.

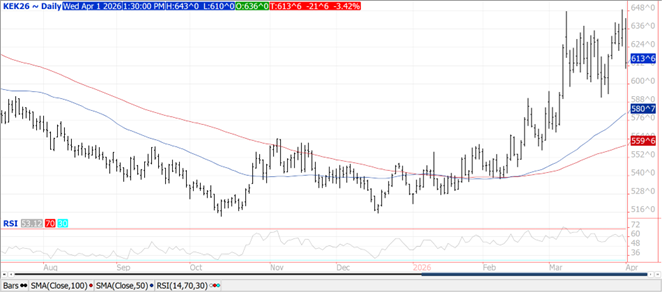

Prices plunged $.16-$.22 with KC futures the leader to the downside. Spreads also weakened. Prices quickly shrugged off support from yesterday’s lower than expected acreage forecasts focusing on rain distribution across the US plains. Next support for CGO May-26 is at LW’s low at $5.77 ¾. Support for KC May-26 is at $5.91 ¼. July-26 CGO near $6.10 would appear fairly valued historically given the Mch. 1st stocks / July thru Feb. usage. All wheat acres at 43.775 mil. were 1 mil. below expectations and the lowest in over a century. Winter wheat acres at 32.41 mil. were down 580k from Jan-26 report and down 743k from YA while at a 6-year low. Spring wheat acres at 9.415 were the lowest in 56 years and down 575k from YA. Yesterday Tunisia reportedly bought 100k mt of soft wheat near $275/mt CF. Rusagrotrans expects Russia’s wheat shipments in March could approach the record from 2024 at 4.89 mmt. If realized would place July-Mch shipments at 37.7 mmt, overtaking YA pace of 36.3 mmt. Export sales tomorrow are expected to range from 10-25 mil. bu.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.