Focus on weak China activity data and start of G7 Finance Ministers meeting, as US/Iran negotiations remain in deadlock; Japan supplementary Budget, Singapore Exports surge and Thai Q1 GDP to digest; US NAHB survey, various central bank speakers ahead.

China: sharp deceleration in Retail Sales, Industrial Production & FAI confirms need for innovative stimulus, and unhealthy dependency on external demand

Expectations for G7 Finance Ministers meeting low, but still needs to avoid highlighting underlying divisions and tensions

EVENTS PREVIEW

Markets start the week as they ended last, with a further rise in oil prices and the glaring impasse in US Iran negotiations to bring an end to the Persian Gulf conflict feeding a growing unease about inflation (and concomitant rise in govt bond yields) and the outlook for the global economy. The run of Chinese activity data will only serve to further undermine confidence. Both Retail Sales slowing to stall speed at 0.2% y/y and Industrial Production at 4.1% y/y, weakest since May 2023 were all the more worrying given favourable base effects, and the recent brief recovery in Fixed Asset Investment also came to an abrupt halt at -1.7% y/y. The need for additional stimulus is all too clear, as is the chronic dependency on external demand, but recycling prior measures will likely yield at most very transitory benefits, above all given the millstone of the long-standing property sector woes. While the headwinds from the Middle East conflict make this a bigger and more complex challenge, an end to the conflict would also probably deliver only marginal benefits, above all relative to other larger economies.

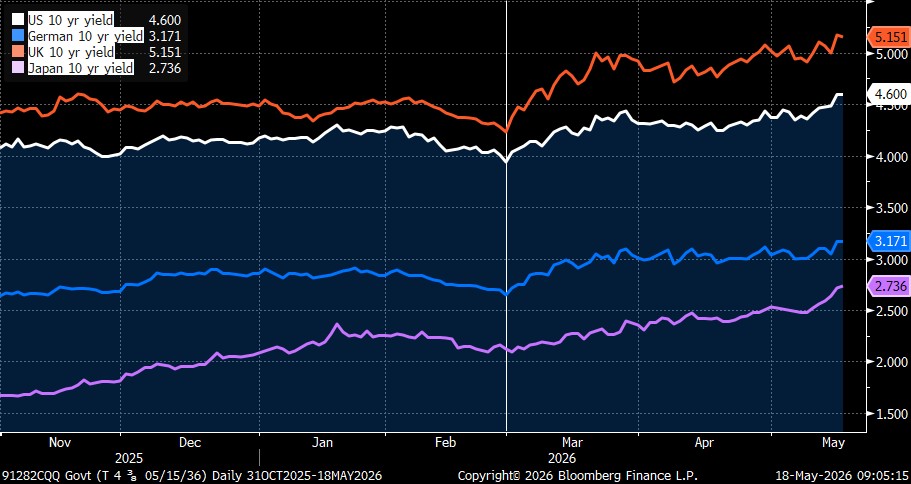

Meanwhile, Japan also moves back to centre stage, as confirmation that an imminent supplementary budget proposal will involve new debt, adding to upward pressure on bond yields (see chart) from oil prices, along with contagion from the rising political risk premium in the UK.

This hardly makes for an auspicious start to the two-day G7 Finance Ministers and Central Banks meeting in Paris today, from which little is expected in the way of concrete measures. But it will still need to convey some sense of unified purpose to tackle the myriad of current economic challenges, which may prove difficult given the numerous bilateral and multilateral tensions. Outside of that meeting, there are the very strong Singapore Exports to digest, with only the US NAHB Housing Market Index likely to attract any attention in terms of the remaining data points. It is expected to be unchanged at a sluggish 34, with risks skewed to the downside given rising mortgage rates, though the impact of the latest jump in Treasury yields may not be captured until next month’s survey. There are a number of central bank speakers, though outside of those at the Atlanta Fed’s annual Financial Markets Conference, most are not scheduled to talk about the economy and monetary policy.

RECAP: Highlights for the week:

Focus remains on national and geopolitical developments with US/Iran talks remaining in impasse, a long drawn-out Labour Party leadership contest in the UK, a formal meeting of G7 finance ministers and central bankers, and informal meeting of EU EcoFin ministers. While traffic through the Strait of Hormuz has picked up slightly, the weekend Iranian strike on a UAE nuclear power plant will keep everyone on edge, as the cumulative disruption to crude, gas and refined products continues to build.

NVIDIA (on Wednesday) and Walmart top the US earnings run, along with other retailer results.

China’s monthly activity, investment and property data, while UK has labour data, CPI and Retail Sales, Japan Q1 GDP and Trade, and Canada looks to CPI, which along with G7 flash PMIs, Germany’s Ifo Business Climate and a busy run of other national surveys, are the highlights statistically.

Numerous commodity conferences, including China Energy Week, Flame LNG in Netherlands, Australian Energy Producers Conference in Adelaide and the Argus Rio Crude Conference. IGC Grain Market Report and USDA livestock monthly report also on tap.

There are 19 S&P 500 companies reporting this week, with worldwide corporate earnings highlights as compiled by Bloomberg News likely to include: Analog Devices, Baidu, Bank Leumi Le-Israel BM, Bharat Electronics, Bilibili, BT Group, Cie Financiere Richemont, Deere, Experian, Generali, Hesai, Home Depot, Intuit, ITC, Keysight Technologies, Lenovo, MS&AD Insurance Group, Nvidia, NIO, Ryanair, Singapore Telecommunications, Sompo, Take-Two Interactive Software, Target, TJX, Tokio Marine, Walmart, Workday, Zoom Communications.

To view the full report and to sign up for daily market commentary please email admisi@admisi.com

Disclaimer: This material is provided for information purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. The views expressed reflect market conditions and publicly available information as of the date of writing and may change without notice. No representation or warranty is made as to the accuracy or completeness of the information. Past performance is not indicative of future results. Readers should consider their own circumstances and, where appropriate, seek independent financial advice.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.