Written Commentary

Prices were $.10-$.12 lower, closing near session lows. Spreads also weakened. July held above MA support at $4.66. Support for Dec is at $4.83 ¼. EIA data showed ethanol production rebounded to 299 mil. gallons LW, up from 297 mil. the previous week while steady with YA. Production was below expectations for the 3rd consecutive week. There was 100 mil. bu. of corn used in the production process, or 14.3 mil. bu. per day, below the 15.7 needed to reach the USDA forecast of 5.60 bil. Ethanol stocks rose to 26 mil. barrels, above 25.2 mb from YA. Implied gasoline demand fell 3.2% to 8.813 tbd however, was up 1% YOY. If energy prices have indeed peaked, in likelihood, so has corn. With the US crop getting planted in a timely manner, US drought areas are low, higher production in SA combined with a large speculative long position make me think the path of least resistance points lower. Tomorrow’s export sales are expected to range between 32-70 mil. bu.

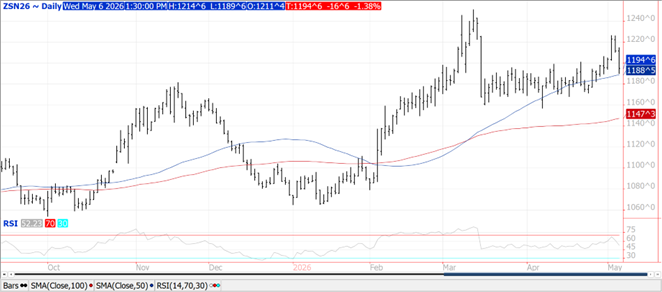

Prices were lower to sharply lower across the complex. Beans were $.14-$.17 lower, meal was down $1-$3 while oil was off nearly $.02 lb. Spreads weakened across the complex. July beans held MA support at $11.89. Longer-term support for Nov beans is $11.50. July-26 meal closed into new lows for the month with next support at its 100-day MA at $314.70. Major support for July oil is at $.70 lb. Sharply lower energy prices weighed heavily on the Ag. space today. The Trump Administration announced they were pausing “Project Freedom” as great progress has been made toward reaching a complete and final agreement with Iran’s acting government. Propping up odds that a permanent peace agreement may be near are reports China is urging Iran to accept the US peace proposal. Energy prices bounced off session lows when Pres. Trump stated the deal was not certain and that bombing would resume if they don’t agree. Spot crush margins backed off $.10 to $3.66 ½ bu. after reaching a modern day high yesterday at $3.76 ½ bu. On Friday the CFTC will likely print another record large position by MM’s in soybean oil and across the soybean complex. At yesterday’s close we estimate MM were net long 200k soybeans, 115k meal and 192k oil. Attention will now shift toward Pres. Trump’s meeting with Chinese leader Xi late next week in Beijing.

Prices ranged from $.03-$.11 lower across the 3 classes, closing well off session lows. CGO July-26 was down $.10 ½ at $6.17 ¼, KC July-26 was $.03 lower at $6.87 while MIAX July-26 was $.04 lower at $6.92. KC July-26 premium to CGO traded out to a new high to at $.70 bu. as HRW production is at much greater risk than SRW as there is still the potential for sub-freezing temperatures the next few mornings in the SW plains. A crop tour in OK forecasts the state’s wheat production will reach only 47.8 mil. bu. with an average yield of 23.1 bpa. The Ave. production in the last 10 years is 94.5 mil. bu. while last year’s crop reached 106.4 mil. bu. Tomorrow’s export sales are expected to range from 5-18 mil. bu.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.