Written Commentary

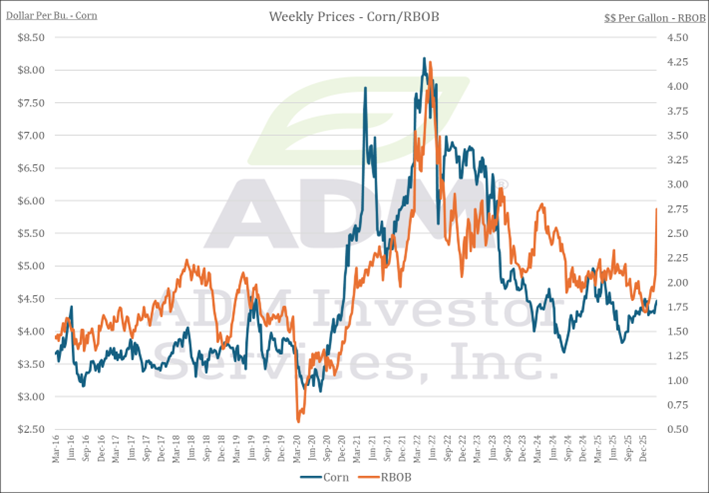

Prices were $.06-$.08 higher closing near session highs. Spreads were mixed as the nearby May/July made new lows however deferred spreads rebounded. May-26 jumped to a 4 month high with next resistance at $4.64 ¾. New crop Dec-26 traded to its highest level in nearly 2 years. Export sales remain strong, up 31% YTD vs. the USDA forecast of up 15.5%. The BAGE estimates Argentine harvest has reached 7% with early yields averaging 8.1 tons/HA, vs. the USDA yield est. of 7.1. The BAGE kept their production forecast unchanged at 57 mmt, vs. USDA at 53. Despite the strength in corn prices this week they didn’t keep pace with surging RBOB prices.

Higher prices across the complex today with beans up $.10-$.22, meal was $4-$8 higher while oil was up 60-90 points. Spreads were also firm across the complex. May-26 beans closed above $12 for the first time in 22 months. Despite the higher trade today, May-26 meal was lower on the week. May-26 oil established a new contract high as it extended a higher close to a 10th consecutive session. Fresh 18 month high on the weekly chart. As energy prices soar, so do agricultural prices. The inflationary implications from higher energy costs continue to fuel speculative buying across a host of commodities. With the war in Iran nearly a week old and the Straits of Hormuz still closed combined Pres. Trump stating he would accept “no deal with Iran accept unconditional surrender” energy prices spiked to close out the week. Spot board crush margins (May-26) were steady at $2.29 ½, matching the high from last summer, while bean oil PV closed at 51.2%. Seems unlikely we’ll see additional Chinese buying of US beans with Gulf FOB offers running $.90-$1.30 over Brazilian offers into the summer months.

Prices surged late closing $.24 to $.33 higher with CGO the leader to the upside. CGO May-26 surged to an 9 month high as the market adds “War Premium” and speculative traders scrabble to unwind short positions. Next resistance is the June-25 high near $6.45. Also a 9 month high for KC May-26 with resistance at $6.42. The UN’s Food and Agriculture Organization estimates global wheat production will fall to 810 mmt in 2026 as lower prices curb plantings. The FAO food index rose .9% in Feb-26 after 5 consecutive months of declines. At this point it would appear we’ll see a much bigger jump in March. Expect to see an easing of US drought conditions over the next few weeks. SovEcon left their 2026 Ukraine wheat production forecast unchanged at 24.6 mmt, up from 23.3 in 2025. They have planted acres increasing .2 mil. HA to 5.4 mil. The USDA is forecasting Ukraine’s production at 23 mmt.

Charts provided by CQG

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 02547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2026 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.